In recent months, GDP estimates from the Atlanta Fed GDPNow Model were typically way higher than those by the New York Fed Nowcast Model.

The situation is now reverse.

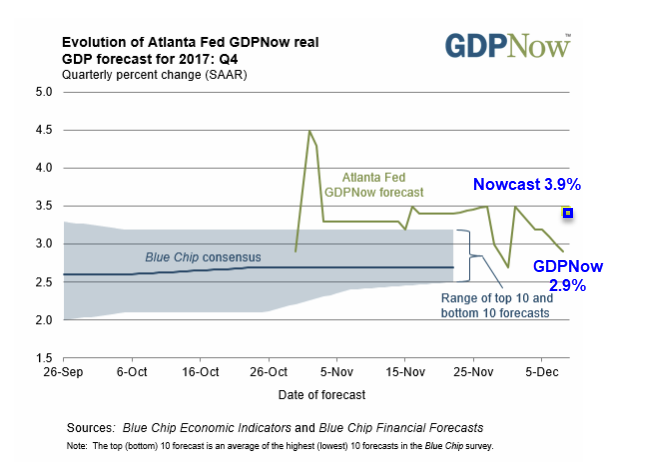

4th Quarter GDPNow Forecast December 8

“The GDPNow model forecast for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2017 is 2.9 percent on December 8, down from 3.2 percent on December 5. The forecasts of real consumer spending growth and real private fixed-investment growth declined from 2.8 percent and 8.1 percent, respectively, to 2.5 percent and 7.0 percent, respectively, after this morning’s employment report from the U.S. Bureau of Labor Statistics. The model’s estimate of the dynamic factor for November—normalized to have mean 0 and standard deviation 1 and used to forecast the yet-to-be released monthly GDP source data—declined from 1.13 to 0.47 after the report,” according to Pat Higgins, creator of GDPNow.

4th Quarter Nowcast Forecast December 8

The Nowcast model did not react to the jobs report, but the GDPNow model reacted with a 0.3 percentage point decline.

An even bigger dive happened following the jobs report in November when the GDPNow model plunged from 4.5% to 3.3%

Dynamic Factor Volatility

In November, I pinged Pat Higgins at GDPNow asking if it the decline was wage related.

Higgins explained the model uses “something like 22 payroll employment series from different industries at various levels of aggregation and two from the household survey to estimate the dynamic factor but It doesn’t use any wage data.”

For more details please see Email From Pat Higgins On the Dynamic Factor Volatility of GDPNow.

Dynamic factor volatility hit GDPNow again this month.

Anemic Wage Growth

Year-over-year wage growth in the jobs report was anemic once again. For details, please see November Jobs +228,000: Employment Only +57,000.

Mike “Mish” Shedlock

As long as official policy, at both the Fed and governments at all levels, is to maximize the share of total output that is distributed via asset appreciation mechanisms to the idle classes; which necessarily reduces the share distributed to those who do the work to create the output; it will take some really magnanimous bubble blowing, before you see price increases for goods the latter group are the predominant buyers for. Which so happens to be what the clowns providing macabre entertainment at our contemporary “economic” circus, refers to as “inflation.”

We’ll get there eventually, once the systemic transfers from the productive to the connected has gotten so rapacious, that none of the former can any longer afford to, nor are allowed to, do anything but serve as simple manservants to the latter. Hence supply of everything dries up, while demand printed out of thin air keeps exploding. Venezuela is, if only slightly in the big scheme of things, still a hair’s breadth ahead of us down that shared road. At least for now.

Nope el-Tedo and the long bond agrees

Mish, are you ready to blink on your low-interest rates/deflation outlook? Trump’s policies are all inflationary, except for his trade talk, which seems to be mostly just talk.