This is a guest blog courtesy of Wirepoints and authors Ted Dabrowski and John Klingner.

It’s the Pension Promises, Stupid!

You can trust public pension apologists to deflect any critique that calls out the failure of defined benefit plans. Unsurprisingly, their response to a recent Wall Street Journal editorial highlighting Wirepoints’ research was just that – deflection via misdirection and victim playing.

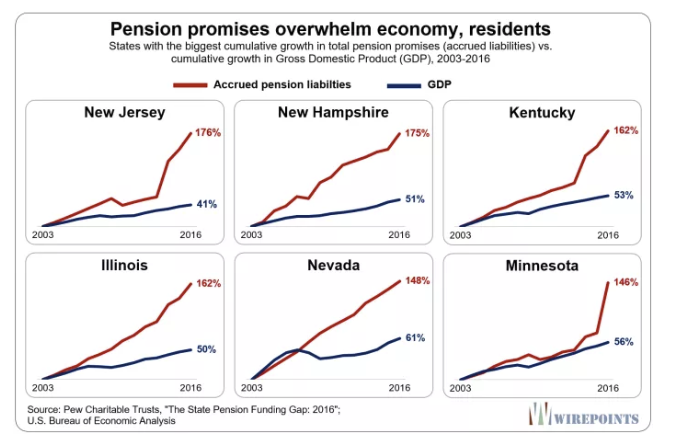

Wirepoints found that a skyrocketing growth in pension benefits, what are known as accrued liabilities, is behind most of the state pension crises playing out across the country. Uncontrolled pension benefit growth is swamping many state economies and the residents who pay for those benefits.

Apologists Deflect Facts

The apologists find the facts inconvenient, so they deflect. They revert to their standard narrative that state governments, and by extension taxpayers, are to blame for “failing to fully fund their public pension commitments.” Or that public employees are the only “victims.” Or they criticize unessential details to distract from the undeniable growth in benefits.

But the apologists don’t disprove the core findings of our research: that unrestrained benefit growth is behind many state fiscal crises.

That was the subject of our two most recent reports: Illinois state pensions: Overpromised, not underfunded and Overpromising has crippled public pensions: A 50-state survey.

The numbers are undeniable. And it’s not just the growth rate of accrued liabilities that’s daunting. It’s how they’re crowding out everything in their path.

Some public pension apologists took issue with the above graphic. They complained that comparing the growth of total pension benefits (accrued liabilities) to the growth in other economic indicators like GDP is “illogical and has no theoretical basis.”

The fact is accrued liabilities are a debt – they are the sum of every pension obligation made to all workers and retirees. The growth in that debt over time matters since taxpayers are liable for a large chunk of those promises. If the sum of those promises grows too fast year after year – far faster than an economy (GDP) and its taxpayers (household incomes) can keep up with – a shortfall will invariably occur.

Any person who’s managed a business knows you can’t let a significant debt grow uncontrollably – regardless of why it grows or the math behind it. Left unchallenged, it will bring insolvency. Same goes for a family and its credit card debt.

Yet that’s precisely what’s happening to some states like Illinois, New Jersey and Kentucky.

For example, look at the below chart of Illinois, where Wirepoints has gathered 30 years of pension and state budget data.

Illinois Pension Promises vs State Revenue

Promises are swallowing the budget and crowding out spending for everything else.

In 1987, total promises made to active workers and retirees were 1.6 times, or 162%, the size of the state’s yearly operating budget.

By 2016, those total promises had jumped to 6.8 times that of state general fund revenues. That’s outrageous any way you measure it.

How did that happen? The answer lies in the massive growth in the state’s total pension promises – some due to a growth in perks and some due to a more honest reporting of what those promises are really worth.

In 1987, total pension benefits promised to the state’s active workers and retirees was just $18 billion. That’s the total amount of benefits the state’s actuaries calculated were owed by the state.

By 2016, total pension benefits owed had ballooned to $208 billion, according to the Commission on Government Finances and Accounting, the state’s official number crunchers. That’s an increase of 8.8 percent, compounded annually.

In contrast, the state’s tax revenues grew to $30.5 billion in 2016 from $11 billion in 1987. That growth rate was about 3.6 percent a year, or about 36 percent faster than the inflation rate of 2.6 percent annually.

The bottom line: Total pension benefits owed by the state grew 2.5 times faster than state revenues, year after year, for nearly 30 years.

Illinois’ pension growth has dwarfed the growth of everything else in the economy – the state’s GDP (using state personal income as a proxy), the state’s tax revenues and its residents’ ability to pay for them.

It’s little wonder that Illinois pensions are dramatically underfunded. Taxpayer contributions could never keep up with that kind of growth. It’s left Illinois with an officially-reported pension shortfall of $129 billion. And a credit rating that’s just one notch above junk.

While Illinois may be the extreme, other states aren’t far behind.

It’s time to stop blaming taxpayers for the pension mess across the country.

In too many cases, it’s overpromising, and not underfunding, that’s the real cause.

More Illinois Pension Woe Links

- Illinois state pensions: Overpromised, not underfunded

- Overpromising has crippled public pensions: A 50-state survey

- Where Illinois’ skyrocketing pension benefits came from

- Harvey, the first domino in Illinois: Data shows nearly 400 other pension funds could trigger garnishment by the state

- A booming market can’t save Illinois pensions

The above courtesy of Wirepoints and authors Ted Dabrowski and John Klingner with some minor emphasis edits, subtitles, and chart trend lines by me.

Mike “Mish” Shedlock

If the unions want pension, then it should be on them. Let the state contribute a set amount. Then they are done. Obligation is met. Like a shared 401k.

Then the union can manage the fund and pay out as they see fit.

I wonder if aging demographics explains a good portion of this?

The politicians, of course, give themselves the same benefits as the union employees. They know that by the time the pain starts, they’ll be long gone. A defined pension plan is an annuity. Some actuary crunched the numbers and knew it wasn’t viable to begin with, then changed the basic assumptions to make it look OK.

The reserve requirements for pension plans were relaxed during the Clinton administration. Gotta love them Dems.

At the end of the next downturn, pensions will not be underfunded; they will cease to exist.

I agree there are a lot of problems with the promises.

But like many others, I find the charts and comparisons of GDP to obligations an abuse of statistics.

I also believe the central banks skimmed about 20% off pension-safe investments by forcing interest rates over 2% lower than they should have been for the last decade. And that alone creates a large funding gap.

Illinois should be an example of corruption and bad management, but not be the example for the average state pension.

I wonder what these numbers will look like at the next recession when equity prices decline 40 – 60%?

Pensioners should have any benefit they are willing and capable of paying for.

Question for Mich: Have you ever seriously considered moving from Illinois to a more financially stable state? (I live in a high personal state income state, and I definitely could be an economic migrant when I retire).

The new Los Angeles Police Chief retired from his previous position, was given a lump sump pension payout of $1.27 million, then was rehired.

It can be lucrative to be the guy with the gun, in the midst of a disarmed sheep flock.

Cops and firemen are exactly where the pension problem lies. And, of course, California takes everything to an obscene level. The guy in this article is just a thief in my humble opinion. He gets a check for $1.3 million, a pension of $300k, and now a job for $400k. And honestly, it is not that hard of a job.

For the “Makers”, the crisis is perhaps 10% of their livelihood. For the “Takers” of all stripes, especially those who promised, it’s a life or death battle. How it ends? The parasite always kills the host.

“The parasite always kills the host.”

A properly co-evolved parasite never kills the host because that means the parasites death too. Instead the parasite feeds off the host, perhaps weakening him somewhat, but primarily uses the host for food and as a vessel of procreation. Then drops out the host through his poo to infect other hosts. Eventually the host evolves to carry the parasite without really noticing it’s there.

In any system governed by survival of the fittest evolution, that kind of permanence only occurs if the relationship is, on a deeper, possibly non-obvious, level, symbiotic. If the host is genuinely weakened, as is a requirement for the parasite to be a true parasite, evolution will favor the individuals with the most parasite resistance. Over time reducing occurrence of the parasitic relationship.

Fittest in evolutionary terms means able and willing to procreate at higher levels than your peers. So your response for any organism is dependent upon the characteristics of any species mechanism for procreation. So a parasite might evolve to be the least destructive during the years when its host is best able to procreate. There are actually viruses that produce proteins that cause bacterial organisms to into overdrive with their procreation, allowing the viruses to infect more bacteria than would be otherwise possible. Interesting stuff though. My post was meant to be more humorous than anything, but, as usual, I missed the mark.

🙂

I’m not quite aspie enough to not catch that your post wasn’t intended all that seriously…..

Fitness does go lots deeper than simply humping like rabbits, though. Instead, in it’s most popular, biological, venue; it comes down to the whole palette of opportunities genes have for influencing how successful they are at projecting themselves into the future.

Simple procreation is important. But so is ensuring viability of offspring; both immediate and 4000 generations down the line. Meaning, sticking around and remaining strong enough to provide for offspring’s sustenance. As well as teaching offspring to do the same. And contributing to building an environment less hostile to own’s offspring than predators’ and competitors… And also, even, having the sense to croak, hence stop consuming resources, once ones own marginal contribution per unit of resource to the future projection, is lower than that of future generations than could otherwise consume them.

In human terms, having 5 kids instead of 15, spending the thus freed up resources on teaching those 5 how to build weaponry, and other technology, that enable the 5 to lay claim to more resources than those who picked the 15 route, is one such way. It’s how technology arose in the first place. Thing is, it’s not sustainable statically, since copying what others are doing, is always cheaper and easier than inventing new stuff in the first place. So, unless those going the 5 route, keep innovating hence staying ahead, the equilibrium will shift back to the rabbits again; just now with the 15 using technology originally invented by the 5. Think cave dwellers focused on procreation, utilizing weapons designed, and often built, by people who had time to design them, due to having fewer kids….

More “pension crises” related, “fittest” also involves building a society that maximizes the resources available to those best able to design and produce the technology and weaponry that allows them to out innovate those choosing more of a procreate-and-cheaply-copy strategy. Instead of arranging it such that potential innovators, current and future, are stuck spending their valuable time and resources clipping the toenails of those way past their technology creating prime.

No doubt that there are problems but these charts are a bit of a statistical abuse to support an agenda. A far better chart would be to show cash flows each year (or decaded). How much needs to be paid out vs how much the states are taking in. It would also be helpful to see on such a chart how much of any mismatch is due to under/over funding of the plans.

And at the end of the day – don’t blame the employees. They asked for something and your elected officials gave it to them.

If “elected officials gave it to them,” there wouldn’t be much of a problem, now would it? As they would then have “it.” Fair and square. Nothing to squabble over.

Me telling some random dude down the street that your firstborn will pay him a million ten years from now, doesn’t equate to me giving him anything at all. Neither does it somehow obligate your firstborn to pay anyone anything. Nor give me some right to stick a gun in his face to force him to do so.

Pensioners were scammed. Again, fair and square. The money is gone. As workers, the pensioners handed over lots of time and money, in exchange for cheap lies. Which is, duh, the only product governments have for sale. The scammers, in government and the FIRE rackets, got their money. The racketeers got to drive fancy cars and live in fancy condos, mansions and hotels in exotic locations. While the government hacks got to preen around the world, pretending to be important figures in some fashionably socialist ownership society. And the pensioners? They got a bag of sweet sounding lies. Those were the terms of the deal. The deal closed, the money was spent. Now there’s nothing more left. It’s history.

Of course, being we’re stuck in a financialized dystopia and all: Now a second set of produce-nothing leeches wants a cut at the through as well, just as the FIRE racketeers did: This time the ambulance chasers. Coming up with one cockamamie excuse after another, for why government now needs to, in addition to sell lies, also run around sticking guns in the faces of completely unrelated third parties, forcing them to “make good” on some scam they weren’t even born when took place. While cutting the ambulance chasers in to the tune of millions, for dragging Dystopia yet another level closer to Venezuela, of course.

“And at the end of the day – don’t blame the employees. They asked for something and your elected officials gave it to them.”

Asked for something? There is currently talk of a potential teachers strike in L.A.

I think there was also a Youtube video of an SEIU member making an electoral threat against some city council if they didn’t get what they wanted.

I have little doubt that the State of Illinois is both over-promising and under-funding their pensions. That’s what you get when you live in a fundamentally corrupt state. I’m not personally opposed to pensions, public or private, but I am opposed to fraudulent behavior, which over-promising or under-funding is.

What I find unwieldy about the argument in this article is a lack of real understanding of the over-promising argument. Did the State’s workforce grow faster than the private workforce? Did the average pay of a State employee grow faster than that of private sector employees? Did legislation pass increasing the total value of the benefit? Say from 50% of final pay to 75%? Any of these things (or combinations) would cause benefits to rise faster than GDP or aggregate State revenues.

Then if the total pension liability grew at a compounded rate of 8.8%, what was the compounded income from funding and interest on investments? How does that play into the issue? That’s not discussed here.

I’d like to see a deeper dive to get a better understanding. Here’s is my bet: the State’s workforce grew faster than the private sector workforce, and average wages paid to State worker’s grew faster than average wages in the private sector. General benefits didn’t change. And, again I’m betting this is true, that growth in State employment and wages was very much in line with historical norms. But what really changed was a massive reduction in growth in employment and wages in the private sector over the same period of time. Which has left private sector workers wondering what happened and left them pretty jealous of their public sector neighbors.

I’m betting that stuff is true because the article didn’t get into any details. And the information shouldn’t be that difficult to find.

The question is how is this going to end?

There will be blood…

Either with a much greater appreciation, both pubic and academic, for the necessity of a very robust, quick, efficient and final bankruptcy process for the long term functioning of any society.

Or, barring that; either Somalia or Venezuela. Depending on whether people grow up or not, respectively.

I think there will be a fudge. Firstly they will squeeze the retirees and soon-to-retire employees probably by limiting COLA increases. Secondly young employees will be offered an opt-out to allow them to invest in 401(k)-like vehicles that will be in the employee’s own name and thus can’t be defaulted on by the state. Lastly there will be an increase in inflation (which is how the COLA limits will mitigate the costs) to decrease the liability in real terms.

I can’t see any other solution that avoid’s Matson’s or Stuki’s predictions of chaos.

You’re betting on the Venezuela solution. That’s where I would lay my money as well.

Not to get into another healthcare debate, but I think some of the pension obligation is towards healthcare benefits, I could be wrong. If true, national healthcare would mitigate some of this disaster. I do know that there is a lot of gaming of the system in the last few years of an employees time by increasing overtime and pay to jack up the ultimate pension payout. A lot of this crap will have to stop and I will bet there will be some public bankruuptcys damaging bondholders as well as reduced benefits expecially for those that are being way overpaid via abuse of the system.