Please consider Italy May Face ‘Perma-Recession’ as ECB Warns of Hazards Ahead.

Italy may be teetering on the brink of a “perma-recession” that will see its public debt spiral out of control and bring the future of the single currency into question.

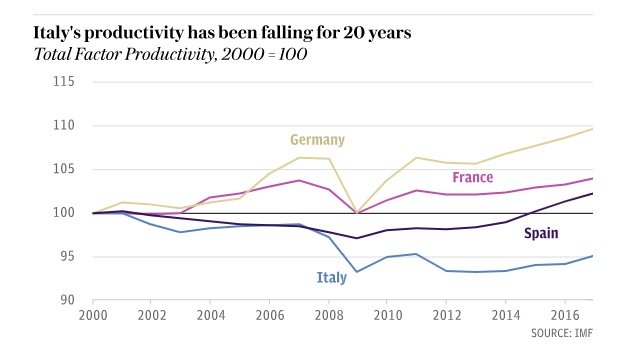

The eurozone’s third-largest economy will see its GDP “flat-line at best” over the next decade, according to Jack Allen, senior Europe economist at Capital Economics. He added: “In effect, we think Italy will be in a state of ‘perma-recession’ from which there is no obvious escape. Among advanced economies, this would be unprecedented.

Deflation Takes Hold

Ambrose Evans-Pritchard warns The European Central Bank has let deflation take hold and is now an impotent spectator.

The European Central Bank has reached the end of the road. It no longer has the monetary levers or the political authority to launch another ‘shock and awe’ rescue if the eurozone tips into recession.

Mario Draghi tried valiantly to bluff his way through the ECB Watchers conference on Wednesday, laying out his surgical toolkit should the worst happen. “We are not short on instruments to deliver our mandate,” he said.

“What instruments?,” asked Ashoka Mody, the former deputy-director of the International Monetary Fund in Europe. “Aside from its jumble of words, the ECB has nothing else to offer.”

“They pulled QE too soon,” said James Ferguson, a monetarist at MacroStrategy. “The underlying economy is not fixed and the banks are not fixed. The chances of a deflationary bust have increased massively.”

Mr Draghi knows – but cannot admit – that the ECB was forced to shut down QE prematurely under pressure from Germany and the northern bloc. The real motives were political, rooted in the dysfunctional character of Europe’s half-built monetary union and German fears of debt union by stealth.

It would take ‘helicopter money’ or people’s QE injected into the veins of the real economy to pull Europe out of a deflationary vortex in today’s circumstances. That would breach the Lisbon Treaty and precipitate a storm in the German constitutional court.

In a sense Europe is paying the price for policy errors made almost a decade ago. The ECB should never have raised rates in 2011 and triggered EMU’s double-dip recession. It should not have delayed QE for five years after the Fed had already shown the way. This inertia – or hubris – allowed ‘Japanese’ pathologies to take root. Now the task is becoming impossible.

Totally Silly Stuff

One hike too many does not cause a recession. Nor does one hike less prevent one.

The EU’s problems are structural.

One size fits all does not work with interest rates. There are enormous productivity differences between peripheral Europe and Germany.

The Euro is a failure and contributes to the mess. Italy, Greece, and even France need huge work rule changes. France does not need tax hikes.

All this talk of “austerity” is a joke. France and Spain have missed budget targets for a decade. Yet here we are, Europe is headed for recession if indeed not in one already.

Inflation Expectations

Misplaced Blame

Monetarists like Pritchard blame the ECB.

The ECB’s negative interest rates were counterproductive, but that’s what the monetarists want.

One does not cure structural problems with central bank policies even if by some miracle central banks could divine the best interest rate. In the Eurozone, that’s not even possible because one size doesn’t fit all.

Finally, the inflation expectation meme is absurd. Those who don’t understand why should take a look at Hello Jerome Powell, We Have Questions.

Mike “Mish” Shedlock

True deflation will make Italy a wonderful place to live! Folks from all over will want to be a part of the gentle recovery from the decades of inflationary depression imposed by the elitist monetary cartels.

Other than death, nothing is permanent.

In what could be considered an appalling move the Italian Prime Minister signed a historic memorandum of understanding with Chinese President Xi Jinping Saturday morning in Rome. The agreement made Italy the first founding EU member, and the first G-7 nation, to officially sign on to Beijing’s “One Belt, One Road” (OBOR) economic development initiative.

For Italy, this appears an “any port in a storm” situation. Italy struggling with a high level of debt and a stagnate economy has found the EU less than supportive and lacking answers as to how they might kick-start growth

The ramifications flowing from Italy’s deal with China may, in the end, prove to be a deal with the devil that opens the floodgates that washes away much of the EU and breaks the euro. The article below delves into the current deal.

“They pulled QE too soon,” said James Ferguson

That is just too funny. If anyone is claiming it was pulled too soon, QE didn’t work.

In Biblical days, every 50 years there was a year of debt jubilee. The long term debt cycle lasted 50 years. It hasn’t changed since then, as the Kondratieff cycle is 50 years and Martin Armstrong’s Economic Confidence Cycle is 50 years.

So now it’s Italy’s turn to be going under. I remember to good old days when it was Greece, then Portugal, then Spain. Good thing for Italy, the ECB has a lot of practice papering over these issues.

You’re right, to suggest the Fed has gotten it right while the EU and Japan blew it is totally silly stuff. They’ve all blown it, though perhaps in slightly different ways and for different reasons.

If only Draghi was able to keep QE going for just a bit longer, everything would turn out alright – banks would have been fixed and there would be no risk of a deflationary spiral. They were oh sooooo close. Darn it.

You know, you read supposedly smart people make statements as such and realize that there are a lot of idiots out there, and quite a few in key decision making positions. Really scary s*#t, don’t you think?

The whole purpose of progressivism, is to ensure that key decision making, and wealth controlling, positions are handed out according to caste membership, rather than free and open competition. As in, according to possession of arbitrarily awarded “degrees” in various forms of pseudo science. The latter to give the pretense that there is some form of meritocracy involved, rather than just a transfer of power and wealth to the children of those who already have the wealth and connections to purchase said degrees. So, you get increasing, and acceleratingly so, decay into institutionalized idiocy. Which inevitably leads to decay of all else as well.

Bringing down all protective tariff barriers might help. Deflationary, major economic adjustments needed but might spur animal spirits.

As for the bond buying it has helped zombies, zombies that will one day need clearing up with major implications there too.

Demographics don’t help. The lifeblood of demand is a growing population with youth setting up house and home. Not healthy in Europe.

With domestic demand less than healthy, and global exports likely to slow, it’s a potential car crash with global implications.

The only places will healthy demographics don’t have the necessary disposable income to keep the global engine running and buying high end cars.

People’s QE? Where will the old spend it?

New pair of slippers perhaps.

Hooking up to China (EU may well do) is no panacea. Japan the same. All the countries with demand able to help are competitors for high end product sales. The others have been kept impoverished by the EU tariff wall in agriculture etc.