James Bullard explains: When Quantitative Tightening Is Not Quantitative Tightening.

The actual effects of QE appear to be far from neutral. There are many ideas about why this may be so. One leading candidate theory is that QE did not have direct effects but did send a credible signal about how long the FOMC intended to keep the policy rate near zero.

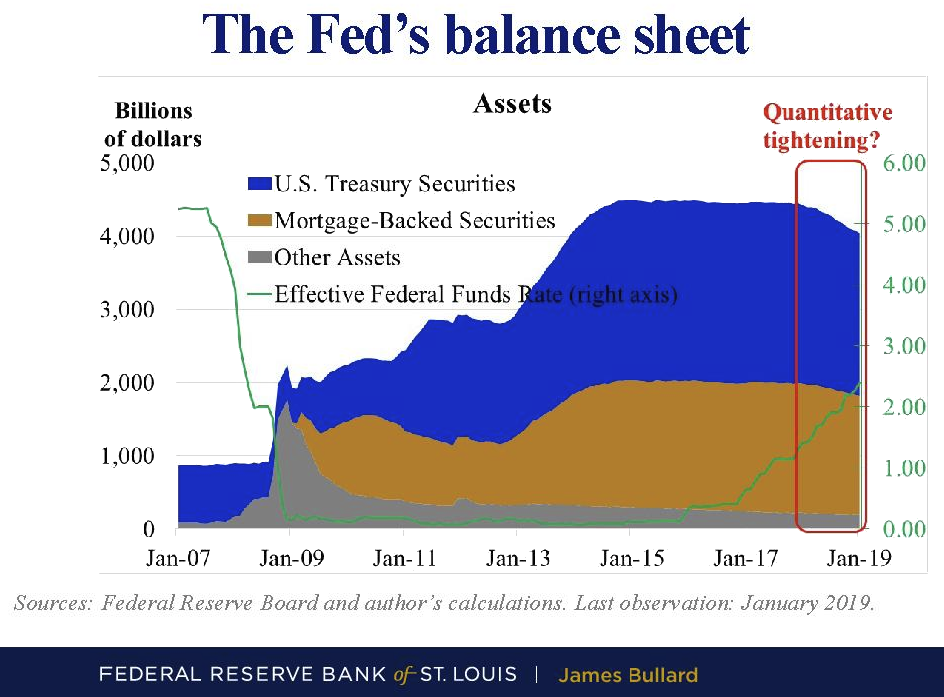

The signaling argument seems to work reasonably well if the policy rate is near zero. In that situation, the FOMC may wish to signal convincingly that it will keep the policy rate near zero “for longer”—i.e., beyond the time that an ordinary approach to monetary policy would call for rising rates. QE may have been a good approach to accomplish this objective.

The figure illustrates the effect of QE announcements on forward rates. A sizable part of the effect is due to expectations for future policy. Imposing no-arbitrage restrictions (right panel) delivers more precise estimates.

Asymmetric Effects

With the policy rate near zero, the effects of QE may have been substantial due to signaling effects.

Now, with the policy rate well above zero, any signaling effects from balance sheet changes have dissipated.

This means balance sheet shrinkage—“QT”—does not have equal and opposite effects from QE. Indeed, one may view the effects of unwinding the balance sheet as relatively minor.

Making Stuff Up As We Go Along

Supposedly QE had no direct effect. Rather it had an indirect one. This is the hindsight given today.

The next time, when something different happens, the Fed will give different hindsight, always with the implied message it did the right thing.

Questions for Bullard

- Why didn’t QE work very well for the EU? Japan?

- Was the goal of QE to raise inflation as the BLS measures it, or raise asset prices and create bubbles?

- If QT doesn’t matter, then why the hell did the Fed abandon it, a week or so after announcing QT was on auto-pilot?

- If it doesn’t matter, why not just undo all of it right now?

Of Ivory Towers and Wizards

In regards to question number two, the Fed surely succeeded at blowing bubbles.

These wizards sit in their ivory tower group-think boxes and spout complete nonsense about the Phillips Curve, inflation expectations and the meaning of inflation itself while ignoring the massive bubbles they blow while doing so.

Stupidity Well-Anchored

Two days ago NY Fed President John Williams reiterated complete nonsense on the Phillips Curve and inflation expectations.

Bullard offered further evidence that Economic Stupidity and Fed Groupthink Remain “Well-Anchored”

Mike “Mish” Shedlock

“The next time, when something different happens, the Fed will give different hindsight, always with the implied message it did the right thing.”

Zero Hedge headline: Bernanke Killed The World Economy, New Academic Study Confirms

“St. Louis Fed president James Bullard discusses Quantitative Tightening (QT). As usual, he makes little sense.”

Bullard manipulated the stock market in 2014, saying that QE shouldn’t end, to goose the market to a new all time high during a serious decline. When QE ended and Japan took over, Bullard then said QE should end and that his previous remarks were misunderstood.

There is no reason to take Bullard’s comments seriously.

Let the good times roll.

Fed Stratagy: Say it over and over again, “TINA is normal”. Eventually, it will sink in.

One will never find real evidence of “direct” effects QE, or QT, or any other central bank action, when one refuses to look at details beyond the most degenerate of macro levels.

Printing money doesn’t create anything real. Nor destroy it. All it does is redistribute that which is already there. So, yes, if one insists on putting on blinders and look at everything from nothing but a sufficiently degenerate macro point of view, both QE and QT can be construed to have “no effect.”

Which is about as relevant as Krugman’s (and others’, both mindless groupies and ostensibly less mindless ones….) assertion that “debt doesn’t matter, since it’s money we owe to ourselves.” So, it makes absolutely no difference whether everyone in America is 100% debt free; or if absolutely everyone, along with all their kids and all their descendants, for all of posterity, will remain indentured debt slaves to Lloyd Blankfein. Hey, it doesn’t make any difference at all, since it’s just money “we” owe to “ourselves…”

Which, again, makes about as much as sense as insisting that nuking Manhattan doesn’t really make any difference either, energy in the universe being conserved and all……..

“As usual, he makes little sense.”

Yep! But market loves him after all he is as dovish as one can get!

Bullard – “Rate hikes, balance sheet reduction ‘coming to an end’”

“I think we’re in a good place today,” he said. “We had a lot of success. People said it couldn’t be done.”

Arsonist at the Fed taking credit (for a job not yet done — given the high debt and frothy markets and the scampering at the Fed if the markets sneezes). Moreover the Great Recession happened because of the Fed.

Strutting about! Why do we put up with him and his ilk?

“Moreover the Great Recession happened because of the Fed.”

There are many plausible arguments for the cause of it, but I’m not aware any that tie the Fed into it at all:

“The most plausible is that it was simply an inevitable cyclical event.”

Greenspan taking the lending standard to ZERO was not simply a cyclical event. It was a deliberate act to foster a housing bubble, along with the Ownership Society program during the Bush Administration.

Here is a central banker talking about the idiocy of keeping interest rates too low for too long…

Poloz ironically re-iterated the consequences of a prolonged negative interest rate environment:

“We have seen the natural results of leaving interest rates very low for a long time. For one thing, this has been hard for people, such as retirees, who rely on interest from their savings for their income.

“Further, people have taken on a lot of debt, mostly in the form of mortgages and home equity lines of credit. By 2017, the ratio of household debt to disposable income had hit a record – with the average household owing more than $1.70 for every dollar of disposable income.

“If we remove households that do not have mortgages, the ratio becomes much higher – close to $3 for every dollar of disposable income. And house prices were rising extremely quickly in some of Canada’s biggest cities.”

I wonder how these magicians are going to extricate the world from the mess they have created. But then, the central bankers are lunatics and one cannot put anything beyond their capabilities…

There is no question that maintaining low interest rates causes a variety of effects. It takes money from those with cash who rely on interest, and gives to those with assets (stocks, real estate). It also benefits those who want to buy homes, so in general it benefits the young as the expense of the elderly. That, however, isn’t what cause the “great recession”.

There were two causes. First, many loans were issued to non-creditworthy borrowers, which sooner or later was going to lead to default. These loans were issued because banks were required to show the same approval rate for all races and areas, meaning they had to aggressively target certain demographic groups, who later had higher default rates. These loans were also issued aggressively because the system in place caused the lender to not care if the loan was repaid, only whether it could be sold. The combined result was a debt crisis that would inevitably collapse. Note that both policies remain in effect, so we can expect a repeat of this problem in the future.

The second problem was the repeal of Glass Steagall, which allowed banks to get into riskier investments. Sure, it didn’t lead to collapse immediately, but it definitely was a significant contributor.

As for whether it was merely a foreseeable cyclical event, contemplate that before Harry Dent had his success go to his head, and starting making crazy forecasts, back in 1991 he wrote “The Great Boom ahead”. In it he forecast that the demographics of the baby boom would lead to the biggest real estate boom of all time (it did), with the Dow going to 15,000 (it did), and followed by a depression led by a real estate collapse in 2008.

Some people believe that the Fed can create a credit bubble, but yet, no matter how much they tried to push on a string post-2008, it didn’t work. They could push reserves into the banking system, but couldn’t get banks to lend to the non-credit worthy, nor get people to borrow. The credit boom prior to 2008 was caused, not because the Fed created it, but because baby boomers kept buying bigger and bigger homes as they moved through their peak earning years, just as every generation does.

The Fed certainly has power, but it is not nearly as great as many think.

Carl_R

What I meant was the Great Recession happened when the boom caused by keeping the interest rate too low for too long (2001-2003) led to a housing bubble (scoffed at by ‘Courage to act’ Bernanke) burst.

Basically the meddling with interest rates since 1987 by Greenspan, further improved upon by Bernanke with QE has been the norm for last 30 years. This is root cause for the boom and bust.

My simple point is low interest rates is the fuel for any bubble (leads to indiscriminate borrowing and mal-investment and monstrous asset price inflation) and this liquidity is provided by the Fed’s actions.

#5. The fake obama “recovery” displayed in a single chart. $5 trillion of “created from nothing” funds pumped into the economy + bailouts + zero interest rates.

And we wonder why we have the massive bubbles and distortions in the economy today.

I think that part of the answer is that the free market is remarkably resilient. I found myself wondering why the Fed actions did so little, and now I find myself wondering why the tariff idiocy has done so little, and in the end, what I come back to is that the economy is resilient, and adjusts for whatever silliness the Fed and/or Government are up to. That’s not to say that government action never has an impact, just that it tends to be smaller than expected, and tends to creep in over a longer period of time than you would expect.

I would conclude the free market is a stronger force than the Fed or government. I would use the word “resilient” to describe how the market returns to its natural trend once government interference through rule changes (shorting) ends. This was made very clear in 2008 when shorting bank and finance stock became prohibited overnight for a period of 4 to 6 weeks. After the ban expired, those stocks fell.