Today’s housing report was a disaster vs expectations.

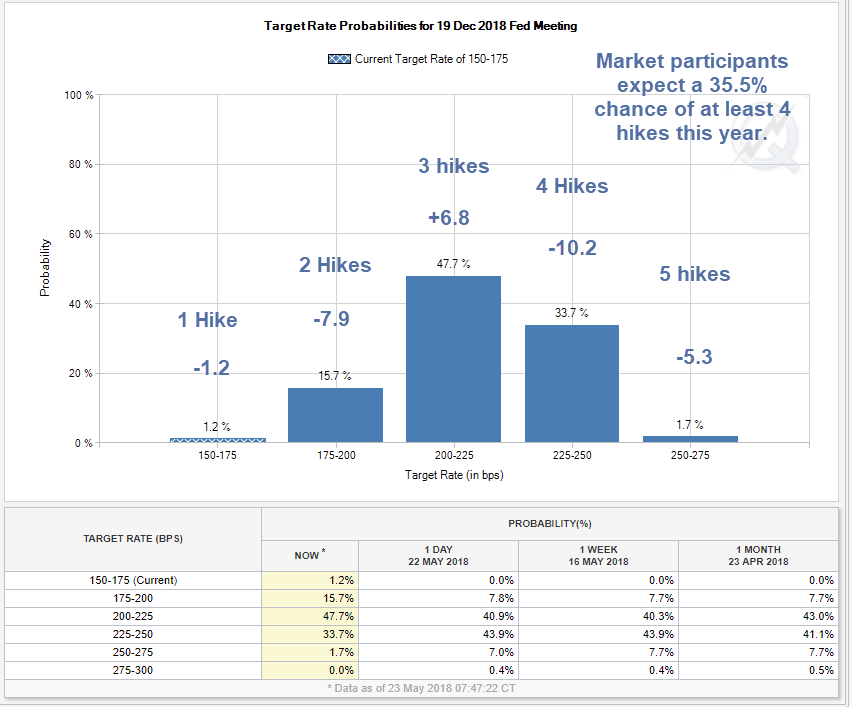

Numbers +- reflect the rate hike odds movement today alone.

Let’s compare to a snapshot I took eleven days ago.

Rate Hike Expectations May 12

Eleven days ago, traders were pricing in chances of five or even six hikes. The consensus estimate was a 47.4% chance of at least 4 hikes this year.

Compare the preceding chart to today’s chart. There is now a small chance of no more hikes this year.

What Happened?

Reality: April New Home Sales Slide 1.5%, March Revised Sharply Lower.

I rather doubt Trump’s trade shenanigans helped any.

One can also ponder this.

Question for the Fed: How does the Citigroup economic surprise index rolling over to 7-month lows jive with the view that “economic fundamentals were currently supporting continued above-trend economic growth”? pic.twitter.com/Rpnd5TeFw7

— David Rosenberg (@EconguyRosie) May 23, 2018

By the way, Rosie might need to rethink inflation as well.

Inflation watchers please note: the yield on the 10-year note is back below 3.0%.

Let’s not confuse late stage inflation with a massive breakout of stagflation. For discussion, please see Reflections on Late-Stage Inflation.

Mike “Mish” Shedlock

Agreed. It’s the internally set discount rates that are screwing the pensions. They dreamed dreams for far too long, then went risky so they didn’t think they’d have to wake up. Falling out of bed onto the floor from a great height, hurts real bad….. Lots of hurt coming.

Part of confidence is, of course, central bank staying a pre-annonced course. No obfuscation with low inflation blabberish.

A good part of the pension crisis is; pension funds putting money into increasingly risky assets to fulfill their obligations. It may not blow up spectacularly, but by gradual attrition. As retirees confront reality, they will cut back spending to the bone.

*Blacklisted said: “It is because of the pension crisis that the Fed is raising.”*

I have difficulty understanding how disrupting an asset bubble with higher rates today is going to help pension funds pay their future liabilities.

Distilling down the Fed’s motivations as best I can, I still see the US Dollar as the foundation of their power. Until they have a viable replacement, they need the dollar to continue being widely accepted as a currency and, since the value of the dollar springs from the cash flows of dollar based economies, the Fed needs those economies grow as debts grow. The reason they cannot give credit away indefinitely is that extremely easy credit is prone to being wasted and, when that waste grows large enough, it guarantees a credit collapse in the future (people and institutions overpay for stuff, consume beyond their means, etc). I think the Fed wants to walk the line between growth and malinvestment and they see that malinvestment has been gaining steam. The billion dollar question is, are they already too late? I suspect they are too late.

I was following you right up until the end. It is because of the pension crisis that the Fed is raising. As stocks rise with the influx of fear capital from around the world, they will continue to raise rates to try and save their image as a serial bubble blower, which of course will only exacerbate the biggest problem – a rising dollar.

Money supply is less important than confidence. As we have seen, you can’t force banks to lend or businesses to borrow if they are not confident in the future. Look at money velocity. It’s at multi-decade lows. If businesses can make a profit borrowing at 10%, they will do it. If they are not profitable at 1%, they won’t borrow. As govt’s get more desperate to hang on to their perks and power, the deeper they will reach into people’s pockets and safety deposit boxes, which of course will destroy confidence.

I think the TINA story is about to die. Stocks are horrendously overvalued by any metric one can think of. This is by the way completely independent of interest rates (the effect of rates on the stock market does of course exist, but I believe it is vastly overstated in modern-day models. Money supply growth is a far more important driver).

Volatility is certainly giving mortgage lenders and home borrowers fits. Lock or not to lock? Looks like new home sales are already feeling the pinch of higher rates. The big question is whether the Fed really believes their own bullshit or not. If they do keep raising rates, it just speeds up the timeline in terms of bringing the economy to a screeching halt, and thus the deflation that comes with it.