by Mish

There is an additional possibility of 0.4% the Fed hikes by half a point.

Then what?

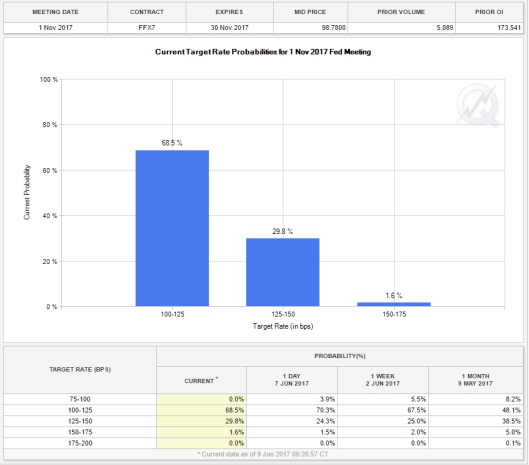

December Odds

December is interesting because the odds of no additional hike this year topped 50% mid-day Friday. The odds settled at 45.5%. The market now expects a December hike.

The Fed managed to get in two hikes so far this year. I expected at most one. The third hike is now supposedly odds on.

Fed Hike Cycle Over?

I doubt the Fed hikes three times this year. In fact, I now think the Fed hike cycle ends in June. The next move, after June, will be a cut or a long delay.

However, if the Fed wants to hike, and can convince the market it will hike, then another hike is coming. Both requirements have to be met.

Economic data has been miserable. Judging from data alone, there is no reason for the Fed to hike (putting myself in their traditional talk-point shoes).

Yet, clearly, the Fed has blown economic bubbles. The Fed could have and should have hiked much more, much sooner.

Of course, that assumes there is a Fed, but there shouldn’t be.

I don’t know where rates should be, and neither do they. At least I know what I don’t know.

The Fed has now blown three massive bubbles in succession. This one will bust too. And instead of working with interest rates at 4.0% when the recession hits, the Fed will start with interest rates at or near 1.0%.

Second Quarter Reality

- Wholesale Trade Report Worse Than Expected: 2nd Quarter Recovery Thesis Nearly Dead

- Factory Orders a 2nd Quarter Disappointment: “High-Flying” Regional Nonsense

- Payrolls “Unexpectedly” Weak, Negative Revisions, Earning Poor: What Happened?

- Trade Deficit Widens: Cascade of Bad News Accelerates, Trump Will Howl

- Construction Spedding: Construction Spending Falls Sharply, March Revised Higher: Construction Spending Mysteries

- Motor Vehicle Sales: Motor Vehicle Sales Flat, Hope Turns to Second Half: What About Fleet Sales? Incentives?

- April Durable Goods shipments down 0.3%, new orders down 0.7%: April Durable Goods: Yet Another Weak Second-Quarter Report

- Wholesale Inventories: Down 0.3% in April. March revised lower from 0.2% to 0.1%.Retail Inventories: Down 0.3% in April. March revised lower from 0.5% to 0.3%. For details, please see Fed Eyes Second Quarter Recovery, Expects Trump Fiscal Policy Will Expand Economy

- Trade deficit in April widens by 3.8% with exports down and imports up: Trade Deficit Widens, Exports Weak: Economists Miss the Mark

- Tax Receipts: Federal Tax Receipts Running Below Expectations

- April New Home Sales: New Home Sales Contract 11.4%: Sales Barely Up Year-Over-Year

- April Existing Home Sales: New Home Sales Contract 11.4%: Sales Barely Up Year-Over-Year

- April Existing Home Sales: Spring Housing Flop: Existing Home Sales Decline 2.3 Percent, Inventory Issues Persist

- April Housing Starts: About that Strong April Recovery: Housing Starts and Permits Flop, March Revised Lower

- April Empire State Manufacturing Survey: Empire State Manufacturing Survey Turns Negative: Welcome News?

- April Retail Sales: Sales were at least positive (+0.4%), but they were well under economists projections: Retail Sales Disappoint Again: Department Stores Clobbered in 2017

Based on data so far, we are looking at 2nd-quarter GDP near 1.0%. If things worsen, expect negative GDP. https://t.co/0FmoTdb4C0

— Mike “Mish” Shedlock (@MishGEA) June 11, 2017

Mike “Mish” Shedlock