by Mish

Hi Mish

A few years ago while going through Khan Academy I stumbled on his series of videos about cause of financial collapse. It was a revelation to me. Ever since I have been looking for for an alternative sources of financial information. That is how I found your blog. I have been reading it almost every day. Thank you for your opinions and knowledge.

I work as an electrician for Ford Motor Co. I have been with the company for 15 years. Two contracts ago Ford and UAW agreed to a 2 tier wage system. Which means that Ford can hire new production workers at $15-$17 per hour rate rather than $23-$25 rate (approximate rates).

I notice that whenever we have a large group of new hires few months later I see number of new vehicles on company’s parking lot. I assume that most of the new cars belong to the new hires. It also seems to me that most of them did not have the best credit and had to finance the loans for the long terms. If the car sales take a down turn contractually this new hires would be the firs to be laid off. Seems to me like a big risk.

Questions

1.Do auto-backed loan securities exist?

2.If so, do they look similar to the mortgage CDOs?

3.Is there a way to short them for somebody with limited financial abilities?

Sincerely

FW

Answers

- Yes

- Yes

- Not easy, perhaps impossible to do so directly as a small investor. In any case, not recommended.

Recall that it was hedge funds who took the opposite side of mortgage CDOs in leveraged ways. Indirectly, one might look for companies that engage in subprime auto loans and short them. That is possible but certainly not a recommendation.

In fact, for someone with limited financial means, I would not recommend shorting at all. It is very difficult to short successfully.

Instead, I would recommend buying gold or gold miners or simply sitting on cash waiting for far better opportunities.

For small investors seeking a low-cost broker, for those who buys small numbers of shares, and for those who trades frequently, I suggest looking into Interactive Brokers. IB is not a full service broker but they have an excellent trading platform and among the lowest fees in the industry. Don’t expect advice or lots of service.

Other than having accounts and some client accounts at IB, I have no other relationship with them, and I get nothing out of this recommendation. I do own gold and miners among other investments.

Auto Loan Securitization Probed by U.S., States

Returning to the initial question, here is a pertinent article from about a year ago: Auto Loan Securitization Probed by U.S., States.

The Justice Department and state authorities are looking into the securitization of auto loans for possible fraud as part of an effort to seek out emerging areas of abuse, Acting Deputy Attorney General Sally Quillian Yates said.

The department’s No. 2 official, in a speech to state attorneys general Tuesday in Washington, said prosecutors were taking a hard look at the auto lending industry to stem any abuses before they could harm the marketplace.

“We shouldn’t wait until there is a crisis to pay attention,” Yates said. “We can and should use our experience investigating mortgage-backed securities to be on the lookout for, and head off, any potential threat, rather than waiting until after losses have been suffered.”

While the auto-loan securities market is much smaller than the market in subprime mortgages that was at the heart of the 2008 financial crisis, there are parallels. Ratings companies are awarding top grades to the securities, while it isn’t easy for buyers to verify the accuracy of those assessments, according to attorneys, academics and other auto-loan securities experts.

Cheap Funding

Scrutiny of the market is intensifying at the same time more borrowers are falling behind on their payments and sales of securities backed by the loans increase. Auto-finance firms that lend to people with bad credit lowered their standards amid increased competition as new entrants flooded the business to capitalize on cheap funding, according to Moody’s Investors Service.

The Justice Department is looking broadly at potential auto loan abuses. General Motors Co.’s financing unit and Santander Consumer USA reported receiving Justice Department subpoenas last year. GM was asked to turn over documents on underwriting criteria, origination, warranties and securitization of subprime loans since 2007.

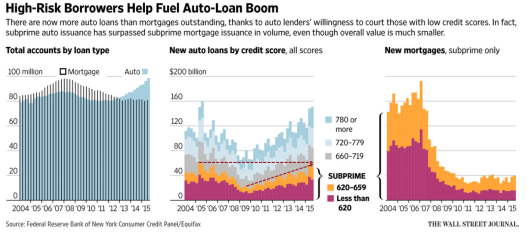

Surge in Subprime Auto Lending Draws Attention

On November 19, 2015, the Wall Street Journal reported Surge in Subprime Auto Lending Draws Attention.

Subprime auto lending is shifting into higher gear, raising some concerns in Washington where top financial regulators have sounded alarms about this category of loans.

Over the six months through September, more than $110 billion of auto loans have been originated to borrowers with credit scores below 660, the bottom cutoff for having a credit score generally considered “good,” according to a report Thursday from the Federal Reserve Bank of New York. Of that sum, about $70 billion went to borrowers with credit scores below 620, scored that are considered “bad.”

But when it comes to auto loans, in particular, a rising volume of loans is going to borrowers with poor credit. The sum in that category has nearly reached the same level as in 2006, raising questions about the health of the nation’s auto-lending portfolio and drawing uncomfortable comparisons to the rise in subprime mortgages that helped fuel the housing collapse, financial crisis and recession.

The comptroller of the currency, Thomas Curry, said in a speech last month that some of the activity in auto loans “reminds me of what happened in mortgage-backed securities in the run-up to the crisis.”

And Richard Cordray, director of the Consumer Financial Protection Bureau, warned in September 2014 that subprime auto-loan borrowers “may be more vulnerable to predatory practices” and that “direct oversight of their lending practices is essential.”

The subprime auto sector is due for a big hit. Is this the year?

Assuming so, many of the subprime auto lenders were gobbled up by larger companies with other more diversified businesses. For example, subprime lenders Safeco was bought by Liberty Mutual.

Even if one can find some direct plays, shorting is not a good idea for inexperienced traders, especially those with limited funds. Shorting CDOs or buying credit default swaps is out of the question.

Mike “Mish” Shedlock