In a Daily Reckoning article, Jim Rickards states This Bond Bull Market Still Has Legs.

Rickards’ article contains some interesting anecdotes regarding bond trading and his relationship with the Fed. And it contains none of the “act now” hype typical of DR articles. It’s well worth a read.

Here is the set of paragraphs that caught my attention.

Rates of 13% when inflation is 15% are actually stimulative. Rates of 3% when inflation is 1% are actually contractionary. In these examples, 2% is a “high” rate and 13% is a “low” rate once inflation is factored in. [No problem with this paragraph.]

The situation today is much closer to the latter example. [Really?]

The yield to maturity on 10-year Treasury notes is currently around 2.7%, the highest since the yield briefly touched 3% at the end of 2013. Inflation as measured by the PCE core deflator (the Fed’s preferred measure) is currently about 1.5% year over year. Using those metrics, real interest rates are about 1.2%, relatively high by historic standards. [Whoa!]

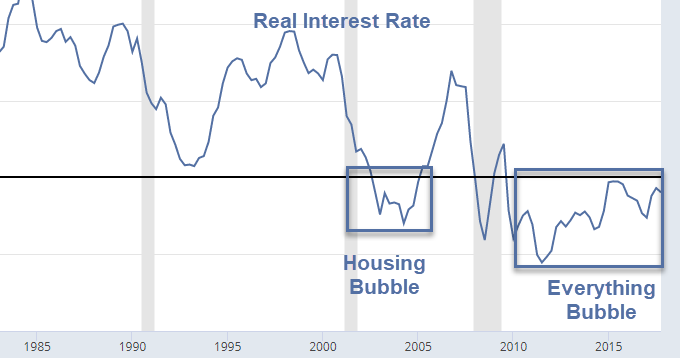

Let’s put that thesis to a chart test.

10-Year Treasury Yield Minus PCE (Excluding Food and Energy)

10-Year Treasury Yield Minus PCE

I have two problems with Rickards’ statements.

- Whether one uses core PCE (excluding food and energy) or full PCE the spread is not historically low.

- Neither chart represents “real” rates. The following charts do.

Fed Funds Rate Minus PCE (Excluding food and Energy)

Fed Funds Rate Minus PCE

The above two charts represent “real” interest rates as commonly understood. And both are negative.

Rates are even more negative if one factors in housing prices as I believe should be done.

Moreover, look at the unprecedented length of time the Fed held rates negative. When Fed Chair Janet Yellen repeatedly stated “real interest rates are accommodative” she wasn’t fooling.

When the bubbles blow up, the accolades for Yellen will vanish.

That said, I believe Rickards has things correct when he states “This Bond Bull Market Still Has Legs.”

Why?

Asset Deflation Coming Up

When recession hits, asset deflation will return with a vengeance. Bank loans based on asset prices rising will force losses. Consumer defaults will rise. Consumer spending will tank.

Add those up and we are likely to see outright price deflation once again. Regardless, the Fed will come in and do what they always do, cut rates. The lemmings in Europe will follow. Those events would be good for gold.

Looking ahead, here’s the crucial question: Will stocks respond to QE4 the same way as before or will the earnings recession deflate that boat too? I expect the latter and it will be extremely painful for the dip buyers.

Meanwhile, Hold the Champagne and Truffles: Yellen’s Story Not Yet Written. Also ignore the inflation hype. It’s another premature scare.

Mike “Mish” Shedlock

You continue to live in a US-centric bubble, while relying on beliefs, biases, and models that do NOT apply in this period of time. Rates will spike higher due to sovereign default risk and lack of demand from everyone except CB’s, which cannot instill confidence no matter how much they print.

Rising rates increases the cost to keep funding govt perks and power, causing govt’s to get increasingly aggressive in going after other people’s money, which further erodes trust and confidence, increases hoarding, decreases economic activity/taxes, and further raises sovereign default risk and interest rates. Rinse and repeat.

The collapse is always from the periphery to the core, which means global capital will continue to accelerate into dollar-based assets, particularly stocks, which is the only other market deep enough that is backed by something instead of nothing.

I regret I dismissed Jim Rickards’ words even before your cogent analysis for misuse of the word “historic” when he clearly means “historical”.

“The Fed will not let deflation anywhere near their grand moral hazard experiment.” The FED cannot prevent a bubble from deflating.

Banks get capital impaired, home prices plunge, stock prices dip enough, Core PCE declines – any of those

Ambrose: “… nations like Venezuela will more than happy to make up the loss in supply …” That is a pity! You were making such good sense up until then. Oh well!

The Fed is raising in part to avoid more damage to the dollar, and to keep foreign investment coming. I think the UST will have to defend the currency at some point, which means buying the dollar at a lower price XXX, and printing the money to do that. Rickards also thinks they will price gold at some rate higher, and back the currency, which is the same thing. The rate hikes were also to give Powell some rate hike room to work with. There are some views that the Fed is really behind the curve, and that inflation will return like the 70s genie in a bottle, but rising rates kill off the HY market and energy investment will turn off, which will not produce much more than $4 gasoline, (small inflation) but a big slam on GDP, and exports. Then prices will actually fall, as the recessionary pull is much greater than the inflationary or stagflationary drag on the economy, only because nations like Venezuela will more than happy to make up the loss in supply. Overall Mish has it right, deflationary vortex.

First of all the fed has no business setting interest rates. Does anyone believe that Ivy league Phd”s who have never worked in the private sector can manage the worlds largest economy? Good reference for this is James Grants latest book The forgotten Depression. Furthermore if the govt used the same criteria to measure inflation as they did in the 70,s and 80,s the official numbers would be a lot higher. In fact there are numerous sites that will give you a different read on the inflation figures. One is the billion prices project. Anyway deflation may be coming but according to my middle class shopping habits inflation is far higher than the fantasy numbers the idiots in DC want you to believe.

The whole world has gone insane. Bitcoin as an example. Any predictions based on people acting rationally in response to facts are null and void.

Agree 100% with Mish. It’s just that we may have to wait a while longer for the next recession with the FedGov pushing the pedal to the metal on deficit spending ($500 BILLION+ and growing). The bond market may have to “take away the keys” first, then the economy goes into recession as a result and finally yields collapse. Not an easy scenario to endure for bondholders.

Mish,

Since you assume the Fed can and is going to do QE4, under what circumstances (or when market has dropped how much?) do you think the Fed will do it?

Very interesting, as always, and something to ponder. The question I’m left wondering is, what will it take to trigger PCE inflation, rather than deflation, which leads to a whole different scenario and consequences and outcomes that are very different. Normally, you’d expect low real interest rates to lead to bubbles, yes, but also to a falling dollar and inflation. When real interest rates were low in the early 70s, that led to the inflation of the late 70s and the overproduction of housing/condos that we saw in the early 80s. With unemployment low, and real rates still low, will it be enough to finally trigger inflation?