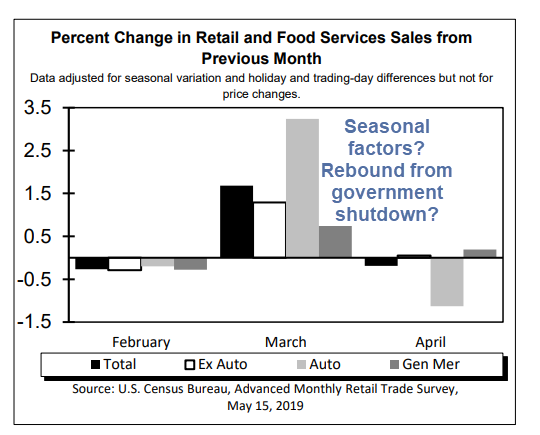

The Advance Retail Sales numbers report for April provides further evidence that the the government shutdown last year had a bigger impact that anticipated. Another possibility is seasonal adjustments gone haywire.

The shutdown started Saturday, December 22 and ended Friday, January 25, 2019 when Trump finally gave up on a wall deal, yet another negotiation error.

Retail Sales vs Expectations

Once again, economists missed the mark badly as Econoday notes.

The second quarter gets off to a stumbling start pulled down by a 0.2 percent headline decline in an April retail sales report where the core details show unexpected weakness. Excluding autos, in which sales were already expected to fall sharply, April sales managed only a 0.1 percent gain to fall underneath Econoday’s consensus range. Excluding autos and also gasoline sales, which were already expected to rise sharply, sales fell 0.2 percent in April to also fall below the consensus range. Just making the consensus range is a no change result for the control group, a component used in the calculation of GDP and pointing squarely to early second-quarter deceleration in consumer spending which had already decelerated sharply in the first quarter.

A 1.1 percent decline in auto sales (signaled by the prior release of unit sales at manufacturers) is no surprise and neither is a 1.8 percent jump at gasoline stations, signaled here by the price of gas. The big surprise is a 1.3 percent drop at electronics & appliance stores that follows a 4.3 percent tumble in March. Weakness here hints at lower prices for consumer electronics and also lower spending on home improvements. Furniture sales also hint at trouble for residential investment, coming in unchanged following March’s 3.1 percent decline, as do sales of building materials which fell 1.9 percent in April following, however, a 1.2 percent rise in March.

The best news in the report comes from its weakest sub-component, department stores where April sales jumped 0.7 percent. This was enough, however, to give only a small 0.2 percent lift to the overall general merchandise component. Another positive is restaurants where sales rose 0.2 percent on top of a great monthly surge of 5.7 percent in March.

Total retail sales in March were revised 1 tenth higher to a yet larger 1.7 percent jump, which is a positive for the first quarter but not the second quarter. The very choppy results from March to April are very likely the result of this year’s April shift from early April last year to late April this year, a shift of consequence that jumbles the calendar and seasonal adjustments. There are plenty of warning signs in this report but taking March and April together offers comfort, pointing perhaps to a steady and moderate rate of consumer spending which is a possibility that can’t be confirmed, however, until the May retail sales report this time next month.

Calendar Shift?

Econoday blames a calendar shift. Perhaps that’s part of it. What about a delayed government shutdown impact?

How about general overall slowness?

Advance Retail Sales – Spotlight Last 6 Months

The choppiness in these reports highlights the difficulty in predicting these numbers. Yet, sales, on average, have gone precisely nowhere for six months.

And it’s not just autos. Economists missed the mark on retail sales less autos by a whopping 0.6 percentage points this month.

The choppiness of the numbers masks the economic slowdown that is clearly in progress.

Mike “Mish” Shedlock

Fed finally stated inflation may preclude them from lowering rates.

This is because economists do not live in the real world. Between genuine price inflation and stagnant income, the majority of Americans just don’t have money to spend. This is reason # 1 for the retail apocalypse. Reason # 2 is the enormous debt run up by these companies, often by vulture capitalists, which cannot be paid back. Between all that–and Trump’s tariffs–I expect us to end up in a near depression.

Prices are definitely higher across the board forsall retail goods and this is BEFORE the current tariffs and the rest take affect. The price of iPhone is going up by 15% effective immediately due to the tariffs

The Easter shift would help April not hurt (v. March)

“What about a delayed government shutdown impact? How about general overall slowness?”

I think that about nails it. It looks like overall slowness, with the government shutdown deferring some spending from December-January to February-March.

Less than 1 million people were affected by the shutdown

So, about 1% of the workforce? If they postponed purchases, and people who worked at businesses that lost sales also postponed purchases, you might expect to see a 1-2 sales drop in January, and an offsetting increase after the shutdown ended.