The S&P 500 fell into negative territory for the year as Retail Warnings added to the misery of a tech bust in progress.

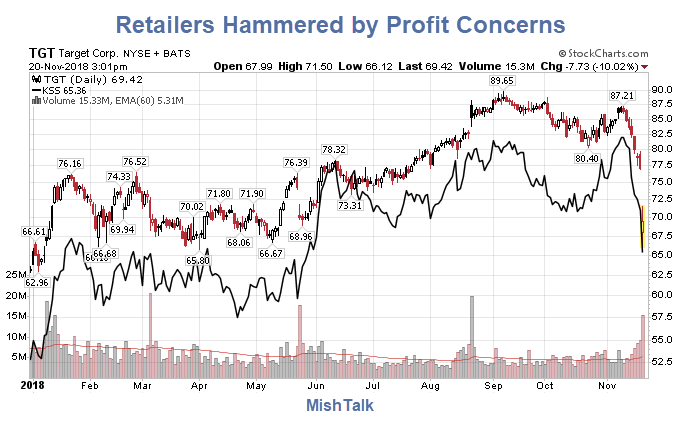

- Target Corp shares (TGT.N) slumped 10.28 percent after the retailer’s third-quarter profit missed analysts’ estimates as investments in its online business, higher wages and price cuts hurt margins.

- Department store operator Kohl’s Corp (KSS.N) shed 9.42 percent after its full-year profit forecast fell below expectations.

- Home improvement chain Lowe’s Cos Inc (LOW.N) fell 4.76 percent after it unveiled further plans of restructuring in the face of worse-than-expected comparable sales numbers.

- TJX Cos Inc (TJX.N) slipped 3.4 percent after the off-price retailer’s holiday-quarter earnings forecast fell largely below estimates.

- Ross Stores (ROST.O) fell 6.94 percent as its fourth-quarter forecast for same-store sales came below analysts’ expectations.

Tech Rout

These 5 Tech Stocks Combined Have Lost More Than $800 Billion in Market Value: https://t.co/VjjFPMdWre by @stephengrocer $FB $AAPL pic.twitter.com/0XQTYJExZ5

— Jesse Colombo (@TheBubbleBubble) November 20, 2018

Stocks Negative for the Year

Dow Jones, S&P 500, NASDAQ all now negative on the year (NYSE FANG+; still positive, but substantially off the year’s high) pic.twitter.com/Dso6rpIy3N

— Michael McDonough (@M_McDonough) November 20, 2018

This is not even a down payment on what’s coming.

Mike “Mish” Shedlock

I wonder what the retirement fund management groups are doing now to contend with their TINA decisions? 50%+ portfolios invested in equities. How’s that workin’ out fer-ya?

Credit cards are maxing up, not mine, but my discretionary has suffered as well, I’m not even so sure about this $69/month internet bill anymore.

This year we have the October slide it doesn’t happen every year unless you are in Pork Belly’s.

We still haven’t seen one important demographic effect. Normally as a demographic group ages, they get into their fifties, and stop spending, which leads to an economic down period (i.e. recession/depression). Baby boomers continue to spend, even though they are in their 60s, so the economy has never collapsed. Meanwhile, the Millennials peaked about 1991, and are now in their late 20s and approaching the years when they get married and become subject to enforced spending.

Can the baby boomers support the economy for the next few years, until the Millennials take over? I have my doubts. The stock market has priced in continued rapid growth and low interest rates, and I don’t see that happening. Any of the following can take us into a long bear market (and bear markets don’t end until people stop “buying the dip”):

Will one of these happen? Will all of them happen a little? I don’t know, but I’m with Mish in thinking that the overall market returns over the next 5 years or so will be negative.

If spending made people wealthier, a ship full of drunken sailors would be the richest country in history.

Spending doesn’t make “people” richer, but it does lead to corporate growth and profits, which in turn makes the markets rise. And, when spending slows, so does corporate growth, and markets reverse. That’s why bull markets don’t last forever.

You can look at the other side of the coin, too. Baby boomers working does create wealth, and when they retire, and live off savings, and social security, they decrease the overall wealth.

A third perspective is that when they retire, they stop adding to their investment accounts, and start withdrawing from it. That can’t make the markets continue to rise.

There is no default risk in US government bonds. However dollar is quite strong compared to Euro so there might be some rise in Euro compared to the dollar for a while until Europe blows up and then Dollar will rally again.

True, it’s a devaluation risk.

It’s correct, there is really no risk of “default” at the present, because the US can always simply print USD and pay off the bonds. The problem is that, as the debt to GDP ratio rises, those lending money to the US will become skeptical of that exact risk, which would lead to a decrease in value of the USD. Thus, the real risk is that those lending to the US will increasingly insist on bonds not denominated in USD, such as TIPS bonds, which are inflation adjusted.

Once the bonds are no longer denominated in nominal USD, the ability of the US to print it’s way out of debt ceases, and they become exposed to the same risks as smaller countries.

People that are paying 110% of their take home pay on housing and “health insurance” have no discretionary purchasing power. I am shocked. Shocked, I tells ya!

Good comment by Schaap60 – Under my scenario a gap down would be over a week or so at the end. That could of course happen several times. By that I mean a sudden drop of 15% followed by a 10% rally that eventually gives it all back then plunges another 15% …. etc for years. Every rally sold until the final plunge. Just a guess

One more point. If this is the beginning of a deflationary trend than expect this economy to last a few generations.

People who are retired will have to learn to make it on reasonably priced stocks or on safe bonds, no matter how low the yield is.

You made the point on Coast to Coast that the market may trend down for years rather than crash in the traditional sense. I can’t help but think people dependent on money in the market for retirement will lose their nerve and it will gap down at some point. It will be interesting to see how this plays out.

Agreed. 2008 is already on everyones mind. Kinda like my ex millionaire great aunt that had most of the money in GM and has spent the last 10 years telling everyone how shes now poor.

Never fall in love with an investment. Your aunt would be a good example.

Never have more than 10% of your stock market “wealth” in one stock.

Ideal is to have 20 dividend paying stocks at about 5% of your stock “wealth” in one stock.

Then re-invest the dividends in more risky investments (tech, internet) every other year and buy more dividend paying stocks every other year.

You here the stories of someone holding Coke since 1912, but investing nearly everything in a single stocks is a fool’s errand.

We keep hearing that the individual investor is less & less significant. Most of the people dependent on the market for retirement money have their funds invested indirectly, through mutual funds, index funds, etc. It is not clear how the professional managers of that money are going to meet withdrawals from their funds — sell the dogs, or sell the good stuff?

Nor is it clear what the people who lose their nerve are going to do with the money they get from liquidation. The only thing we know for sure is that almost every asset class is over-priced by historical comparison, and everything is likely to mean revert. Not a pretty situation.

Shaap60, I think you are right to expect a sharp decline to hit one of these days. First of all, market peaks characterized by extreme overvaluation have always been followed by a wave of panic selling in the past. In short, market history suggests that the market is actually quite vulnerable to a crash.

Secondly, the needed preconditions are in place: money supply growth has slowed dramatically and there is a lot of leverage in the market (margin debt). Moreover, a great many systematic trading strategies are acting on similar technical signals and tend to exacerbate moves in both directions.