Since there is no longer any reasonable debate about a trade war having started, let’s investigate how it ends.

Two days ago I wrote Trade End Game Scenarios: Boycott Treasuries vs Yuan Devaluation.

I posted the topic following this Tweet by David Rosenberg, Chief Economist & Strategist at Gluskin Sheff.

The end-game retaliation comes via a global boycott of the Treasury auctions. Foreign entities fund half the US fiscal deficit, which is set to double. Imagine the locals funding their own budget gap! This forces the savings rate up at the expense of spending. Recession follows.

— David Rosenberg (@EconguyRosie) June 19, 2018

I strongly disagreed with Rosenberg.

Treasury Boycott Thesis

I am surprised that Rosenberg brings this up because, in my mind, this hash has been settled long ago.

What exactly would China, Japan, and Germany do with their reserves and ongoing trade surplus? Mathematically they have to do something.

Historically, that something has been to buy treasuries. But I suppose China could buy could be gold or US equities. The latter would be smack in the middle of an obvious bubble.

And if China were to dump US treasuries, the alleged nuclear option, it would serve to strengthen the Yuan. Recall that China sold US treasuries to support the Yuan and stop capital flight. In a trade war, China would not want an appreciating currency!

I think Rosenberg proposes nonsense, but given the nonsensical actions of Trump, I cannot rule out nonsensical or illogical responses.

This leads us to the most logical real threat.

Yuan Devaluation Thesis

China cannot retaliate with enough tariffs on its own to combat tariffs imposed by the US. However, the yuan does not float. China could devalue the yuan enough to counteract the value of US tariffs.

But hold on. It is not without risk. Recall that China sold US treasuries to stop capital flight. If China devalues, there is a strong likelihood that capital flight would intensify.

What If?

Economist Brad Setser asks What Would Happen if China Started Selling Off Its Treasury Portfolio?

As the Trump administration has emphasized, China cannot match the U.S. by putting tariffs on $250 billion, let alone $450 billion in U.S. exports. The U.S. just doesn’t export that much to China

China also could respond asymmetrically, and look toward other levers that it may have over the U.S.

Three stand out:

- Imposing new limits on U.S. firms operating in China, and taking actions that limit their sales in China. Apple and GM sell a lot of made-in-China phones and cars that wouldn’t be impacted by tariffs.

- Weakening China’s currency to offset the drag on China’s economy from far reaching tariffs. A standard, empirically well-grounded, rule of thumb is that a 10% depreciation (against a basket) raises net exports by about 1.5 percentage points of GDP—which could effectively offset realistic estimates of the economic drag of a trade war on China. This option isn’t without risks—it could reignite now contained capital outflows from China, and China might ultimately end up with a bigger-than-initially desired depreciation.

- And the perennial threat that China would sell its Treasuries. That could happen as a byproduct of a decision by China to push its currency down—if China signals that it wants a weaker currency, the market would sell yuan for dollars, and controlling the pace of depreciation would require that China sell reserves. Or could happen even if China maintained its current basket peg and shifted its portfolio around—selling Treasury notes for bills, or selling Treasuries and buying (gulp) Bunds (if it can find them—it might end up buying French bonds instead) or JGBs.

[Mish Comment: I do not fully understand point number 3 given conventional wisdom is that China sold US dollar assets to shore up the yuan and stop capital flight.]

A quick reminder. Treasury rates are usually understood to be a function of the expected path of Federal Reserve short-term policy rates.

Purists (Michael Woodford, for example) argue that “flows” have almost no impact on the Treasury market, and the only thing that really matters is the expected path of the Federal Reserve.

I do, though, think “flows” matter. A standard, empirically well-grounded [PDF] rule of thumb is that 1% of GDP in Federal Reserve “QE” or asset purchases reduces long-term Treasury rates by about 5 basis points, so 10 percent of GDP in “QE” would be expected to reduce the ten year yield by something like -50 basis points (here are the latest projections from Fed staff).

[Mish Comment: Setser believes US Treasury yields would rise by about 30 basis points if China dumped its entire $1.3 trillion portfolio. Yep, that’s it. I am more inclined to side with Woodford at least in regards to the flow impact. I do not agree that the “only” thing that matters is the expected path.]

A 30 basis point rise in the ten year, even 60 basis point rise in the ten year, would be painful, but also ultimately bearable. And, critically, these estimates assume that the Fed doesn’t react to a rising term premium and a steepening of the yield curve by easing.

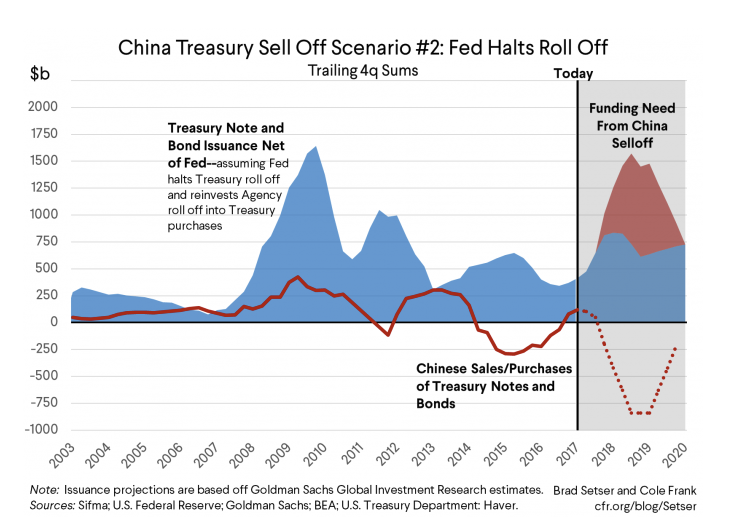

It is fairly easy for the Fed to signal that it expects fewer rate hikes going forward than it expects now. Plus the Fed has a second, fairly direct, way to respond to Chinese sales: change its pace of balance sheet roll off. Roll off is scheduled, counting Agencies, to rise to $150 billion a quarter/$600 billion a year by the fourth quarter. Stopping that, and perhaps signalling that over time the Fed would raise the size of its balance sheet in the long-run would provide a powerful counter to Chinese sales. The combination of a bigger “terminal” Fed balance sheet and a change in rate expectations would, in my view, be more powerful than anything that China could threaten.

I am not in the business of giving China advice on how to upset U.S. markets.

But if the National Security Council ever was convened to discuss China’s options for asymmetric retaliation, I would encourage it to spend most of its time worrying about the consequences of a Chinese exchange rate move. The impact on any such Chinese depreciation on the United States would be limited if the U.S. could convince its allies in Asia to take action to avoid following China’s currency down (even though it is against their short-run economic interest; their export driven economies compete directly with China). They have plenty of reserves—and could sell those reserves to absorb market pressure for their currencies to depreciate along with the Chinese yuan. But they aren’t likely to do that if they think the U.S. brought on the Chinese devaluation through reckless trade action.

And I would encourage the U.S. government to spend a bit of its time thinking about the impact of Chinese sales of assets other than Treasuries, a scenario that I discussed back in April with Joe Weisenthal and Tracy Alloway.

Treasuries sales in a sense are easy to counter, as the Fed is very comfortable buying and selling Treasuries for its own account. I have often said that the U.S. ultimately holds the high cards here: the Fed is the one actor in the world that can buy more than China can ever sell.

Nuclear Threats Real and Imaginary

The nuclear dumping threat is a topic that just will not go away. Every few months it comes up in one way or another. I was surprised when Rosenberg brought it up.

A reader asked me about dumping the other day. I said what would China buy? Gold? US equities? Copper? What?

Setser asked Bunds? French Bonds? Japanese Bonds?

Not only is dumping a sword the US could easily counteract, it is a sword in which China, without US currency reserves, might chop off its own head.

The real “nuclear” threat is a devaluation. And it would be much harder to counteract. But once again, such an action also poses a huge risk to China. If Chinese investors thought more devaluation were on the horizon, capital flight would intensify.

To stop capital flight, China would have to sell US-denominated assets to buy the yuan, thereby strengthening the yuan.

We have come full circle, haven’t we?

Mike “Mish” Shedlock

Totally agree this is a silly topic, but one point that rarely is mentioned is that the US has records of all treasuries owned by China (and everyone). If this trade war escalates we could declare all 1.3T null and void based on “national security”

capital flight? there is no free capital movement in china

It is certainly possible for China to sell their treasuries without caused appreciation of their currency. All they have to do is use the proceeds to buy some other dollar-denominated assets.

It doesn’t really matter if China holds bonds or cash in reserve, reserves are an accounting device to help the BIS keep the books It doesn’t matter who runs a trade deficit, somebody has too. Trump could avoid this by signing a buy America subsidy to consumers instead he wants to TAX TAX TAX. China capital needs are for Belt and Road infrastructure, and hence its not recursive, or consumer based, or dead end spending. China could spend all its dollar based reserves in Central Asia and the foreign funds held in reserve at Treasury would not change and I am sure American/multinational corporations are going to get a big slice of that cash in contracts. The problem is not what China is doing its what the US reckless Federal spending policies are doing to the bonds they hold in good faith. (insert fingers in throat at this point) Trump promised to renegotiate those bonds in his campaign, America cannot put tariffs on everyone and run massive deficits. The man is fundamentally insane and he is not a businessman. The fact that the Fed has this deux la machina of interest rate hikes only serves to prop up the dollar while he pulls the rug out from under the people who hold those dollars. The dollar rises and China sees an advantage in changing bonds (adding more risk) into dollars. Argentina sold 100yr bonds at 7% (to US institutional buyers) because the perceived future risk is much less than their PAST or historical risk, while in the US mountains of zero interest Treasury bonds in circulation now are impaired by the prospect of FUTURE risk to our credit rating, which reflects on the leadership and no prospect in sight of balancing our budget even if we mug our allies for cash on these trade deals.

China could dump Treasuries if it became afraid that they are dropping in value or if they are treated like Iran and thereby stuck with them. Maybe Russia believes this is going to happen.

The Treasury can just “print” whatever it needs and/or have the Fed buy them up. Japan has been getting away with this for many years.

I can envision China swapping a portion of the procedes from any Treasury sales with EU member central banks and the balance into metals and other commodities.

The fed can purchase unlimited treasuries? Guess again, that won’t happen because that is no way to finance a government.

tariffs is smoke screen,trump wants the commies in china,NK gone period before they take over the world.

“[Mish Comment: I do not fully understand point number 3 given conventional wisdom is that China sold US dollar assets to shore up the yuan and stop capital flight.]”

Per Setser: “..if China signals that it wants a weaker currency, the market would sell yuan for dollars, and controlling the pace of depreciation would require that China sell reserves.”

You’re saying the same thing: Selling US assets shores up yuan. Setser just postulates that if China implicitly signalling it wants a weaker, less shored up, yuan; it will, in practice, end up having to shore it up. Due to “overreaction” by other market participants.

..a whole lot of speculative hobgoblinology if you ask me….. But that’s what life in a central bank centered world is all about, I suppose….

Why couldn’t the Chinese just buy physical gold and kill the paper shorts (US banks)? If the price of gold rose to $2000 an ounce or more wouldn’t this be a lethal blow to the dollar?

A large part of the trade deficit in goods is caused by American firms investing abroad (e.g., China) and using the local economy to produce goods that they export to the American market. If Trump wants this to stop, he should make sure these companies pull their investments out and reinvest their capital in American production! US policy has for decades encouraged the exact opposite. The idea that these foreign workers are robbing America is crazy — they are accumulating pieces of paper in exchange for giving away real stuff to Americans that they could better use themselves!

There is no nuclear option. Going nuclear can only mean mutual destruction. It reminds me of Trump’s question in the early days about what good is it to have nuclear weapons if you can’t use them?

Actually, they offered to buy B$70 of American goods and agricultural produce; that’s quite a bit, since there is only so much cotton and grits you can use.

By punishing firms that are doing just that?

Q: “then why would China be inclined to retaliate at all?”

A: Because Chinese leaders are as economically illiterate as Trump

Mish, if you are correct about free trade being the best medicine no matter what any other country does, then why would China be inclined to retaliate at all? It would be to their benefit not to retaliate while the US hobbles itself with higher tariffs.

Even Realist seems interested in teaching the US a lesson at this point. Why bother? If the US is hurting itself more than other countries by enacting additional tariffs, then we will suffer from these bad policies without anyone else’s help. I would think the more competitive countries would go about their business meanwhile.

(I am not in favor of the US suffering under bad policy. I want to better understand an inconsistency in what is being discussed here.)

The other option for China would be to sit down and negotiate with the US on moves to increase imports from the US. China would want to do this quietly, but it would be the most effective response — and maybe the most likely.

Great post Mish. Thanks for your work every day to create a great place for people to come daily to read interesting analysis of events and markets. Yours is one of the few economic blogs I try to read daily.

Ye the Fed could buy them. What Sester said. I do not think the Fed would even have to resort to that.

If there were a drop off in Treasury buying by foreigners couldn’t the fed just buy them like Japan has been doing. Seems to be working for them although I don’t understand why it has for so long as it has.