At the current rate of 2.35%, the Fed hands out about $33.58 billion in free money to the banks.

Interest Rate on Excess Reserves

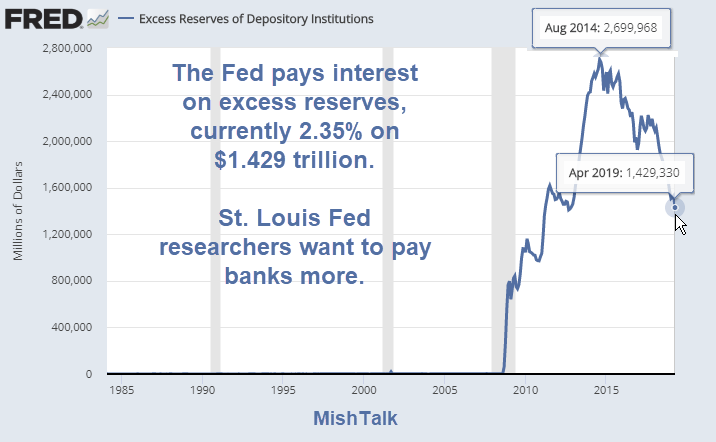

The two charts show the moving target.

Excess reserves peaked at $2.7 trillion in August of 2014 but the interest rate on excess reserves then was only 0.25%.

0.25% of $2.7 trillion is “only” $6.75 billion in free money at an annualized rate. At the current rate, banks take in over $33 billion in free money.

The peak annualized rate was probably in August of 2017 with the interest on excess reserves at 1.95% on $2.2 trillion. That’s free money to the tune of $42.9 billion at an annualized rate.

St. Louis Fed Proposal

Please consider Why the Fed Should Create a Standing Repo Facility by David Andolfatto, Senior Vice President and Economist, Federal Reserve Bank of St. Louis; and Jane Ihrig, Associate Director and Economist, Federal Reserve Board of Governors.

Market participants are projecting ample reserves in the $1 trillion range—a level much higher than their precrisis average of approximately $20 billion.

Why should banks prefer reserves to higher-yielding Treasuries? One explanation is that Treasuries are not really cash equivalent if funds are needed immediately. In particular, for resolution planning purposes, banks may worry about the market value they would receive in the sale of or agreement to repurchase their securities in an individual stress scenario.

The Fed could easily incentivize banks to reduce their demand for reserves by operating a standing overnight repurchase (repo) facility that would permit banks to convert Treasuries to reserves on demand at an administered rate. This administered rate could be set a bit above market rates—perhaps several basis points above the top of the federal funds target range—so that the facility is not used every day, but only periodically when a bank needs liquidity or when market repo rates are elevated.

With this facility in place, banks should feel comfortable holding Treasuries to help accommodate stress scenarios instead of reserves.

Treasury Sales On Demand – Guaranteed Bid

Lovely. The Fed proposes a facility that would allow banks to hold higher yielding treasuries instead of holding excess reserves, by guaranteeing a bid for the treasuries.

Sweet Spot

Given the inverted nature of the yield curve in many spots there isn’t all that much to gain, but there is some.

The current sweet spot in this scheme is the 6-month T-bill. It yields about 10 basis points or so more than the 2.35% the Fed currently pays on excess reserves.

Annualized Value

The annualized value of the proposed scheme is only $1.4 billion. Still, that’s nothing to sneeze at.

Hidden Beauty

Please don’t forget about the hidden benefits.

Like what?

See if you can figure it out before reading further.

Poof!

There are no longer any excess reserves.

Banks get to buy treasuries with a guaranteed bid. So they do. En masse. In a flash, the top chart will look like it did in 2005, with everything seemingly back to normal.

Judging from the top chart, one has to wonder how much this has been front-run already, above and beyond stated tapering, now on hold.

Mike “Mish” Shedlock

Excellent comment by Maximus Minimus – Bringing it to the top

“Negative interest rates meant EU banks had to pay the ECB to park funds! And they pass the negative ioer on; the EU bank customers have to pay the bank to keep their money. How much more convoluted can it get?! You keep saying: the end must be nigh, but like circus actors, they keep the plates spinning.”

Is this now totally clear?

“I don t quite get this …”

When the Fed did QE – It did not come from deposits. It handed the banks $2 Trillion.

The banks had no choice – they had to take it.

The banks had no real use for it. So they deposited the money back at the Fed at the stated rates in the chart.

YES IT WAS FREE MONEY

Contrast to the ECB policy of negative rates. The Fed slowly recapitalized banks over time. Negative interest rates meant EU banks had to pay the ECB to park funds!

BTW, the deposit rate is still close to zero in the US. In the eurozone it is negative. The ECB thought they could force consumers to spend. It did not work.

QE was described by Bernanke as an “asset swap”, which is technically correct. The banks sold the Fed “troubled” assets (for which their was essentially no bid) for full face value and received credits to their reserve accounts in return. The “money” the Fed used to buy these “troubled” assets was indeed created out-of-thin-air. The money the banks originally used to fund those “troubled” assets was borrowed from somewhere. The Excess reserves sit on the banks’ balance sheets as assets. There is a corresponding liability, which is the funding for the original “troubled” asset, or whichever borrowing eventually replaced it.

“Negative interest rates meant EU banks had to pay the ECB to park funds!”

And they pass the negative ioer on; the EU bank customers have to pay the bank to keep their money. How much more convoluted can it get?!

You keep saying: the end must be nigh, but like circus actors, they keep the plates spinning.

As long as there are some productive people left, who put up with being robbed, the theft rackets can go on. They will only end, once the productive classes finally grow up, and end it all: End the Fed, Gold at $20/oz, default on all federal debt, no activity taxes. Problems conclusively solved.

Tough, they are the greatest actors Hollywood wished to have: they pretend to know what they are doing.

Yup. Lots of Venezuelans kept cheering for Chavez, pretty much all the way up until they keeled over from downright starvation…. And despite all the grandstanding babble of some pseudo “conservatives,” it doesn’t look as if Americans posses any more of neither brains nor a backbone.

No secret that banks are subsidized, they are like middle men, also gamblers, skimmers, and wheel greasers. My CU pays me 1 tenth of a point interest rate, but other banks want the deposits and will pay 2%+ currently. Obviously we are living in more “free money” times than anytime before. Banks seem very loose right now, and many are back to HELOC’ing their futures again. With lower margins, and unemployment at 50 year lows, their is no shortage of lendees and subprime loans, even with lower rates, they can just lend more out, they make most of their money on the front end of their loans so they don’t really care to much if people pay their loans off or not. The debt piles are so big, even small returns add up. If they are getting money from the fed/government so what, who isn’t these days, government borrowing is what’s floating us, i.e. a trillion a year goes toward defense and medicare.

Why dont you jackasses hide some my $ in my account? What a racket. Not to mention a lot of BS. This is like being a young kid playing board games and making up rules as you go to always keep yourself ahead. I would ask at what point does everything they say and do become complete nonsense but im pretty sure were long past that.

It’s pure folly to believe that the thieves benefiting from a theft racket, will ever be the ones ending it.

The ones who need to wake, and grow, up; are the vast majority whose designated role in the rackets, are being robbed harder and harder.

Unfortunately, most of those saps, seem to be too indoctrinated, and economically illiterate, to even have the faintest idea of what is going on. “Not one man in a million,” as Keynes put it, back when he was still practicing economics, and not the charlatanism he is mostly infamous for. So, the saps instead prefer to be led around in dumbcircles. By charlatans blaming “Mexicans,” “Chinese,” “Racists,” and all manners of other utterly irrelevant nonsense.

The US Treasury complex is their “Citadel”. Uncle Scam, the Fed and its TBTF member banks will collude to ensure that there is ALWAYS a bid for Treasuries. Looking at Japan, you can see just how this will work (until it doesn’t). It is stealth MMT.

Yes. During WWII, the US government didn’t have the money to fight the war. So the government ran a giant deficit. In order for interest rates to remain low, the Fed simply and quietly printed the money and added it to bank reserves. The banks were required, by law, to use that money to buy the treasuries.

The young men were sent to war and young women were sent to the factories. The government put price controls on just about everything. Not so much to keep inflation low, but to minimize profits on consumer goods. That pushed manufacturers to focus on higher-profit war materials.

Making MMT happen is relatively simple. Just allow the treasury’s account at the Fed to go negative. Federal spending ends up in the banks anyway. The banks would use the incoming new money to buy treasuries. We essentially have that on an intra-day basis already.

To be fair, banks earn money on interest rate differentials, which is hard in a Zirp world. They also have more (interest rate) risk on their assets in a world with depressed interest rates. So the Fed is helping them out, that’s the function of the Fed. You might ask, Why do they get help when others get to go bankrupt or earn practically nothing on their savings? Well, that’s a good question. The whole playing field is always tilted in favor of privileged parties that helps funds trickle their way, but all such measures are always justified by referring to the supposed greater good for the “economy” at large.

Of course the other option would be for the Fed to simply pay far less of a percentage on the excess reserves. Say, 0.25% instead of 2.35%. The interest rate paid has just marched up with the FFR.

QE should have been handled as a repo, taking assets off of banks balance sheets and replacing them with cash at par during the height of the panic. Then, when the economy turns around, putting those assets back and destroying the cash.

Unless they might need the money on very short notice, depositors do simply buy T-Bills instead. In exchange for having deposits available on demand, many banks do borrow from their depositors “for free” (almost). Along comes the Fed and says: “You’re a bank. We will do you a special favor so you can earn higher rates with that demand deposit with no risk. Buy T-bills to earn higher rates and, if you need the money back right away, the Fed will repo the T-bills in exchange for cash with almost no penalty.”

Fractional reserve banking is such a racket when there is a printing press standing by to paper over bad decisions.

“Fractional reserve banking is such a racket when there is a printing press standing by to paper over bad decisions.”

Emphasis A. It all works out if there is either no printing press, or if one is available to everyone. It only becomes a guaranteed theft racket, when some animals are, a priori, designated more equal than the rest.

I don t quite get this, american banks do pay their depositors, don t they, so what s left of that 2,35% ‘profit’ ?

The banks DO NOT have to pay for the funding that they “deposit” to the Fed.

It was literally FORCED on them via QE

Of course it’s free money

The Fed pads its balance sheet giving the banks money. The banks park the money ate the Fed at 2.35%.

The proposal is to give the banks still more

It is not free money as it is a repo on which they have to pay interest at a rate greater than IOR. And the goal here is to reduce the balance sheet while allowing for ample reserves in time of stress but they do a poor job of communicating what is to take place to do this.

As the quote from the article says:

“This administered rate could be set a bit above market rates—perhaps several basis points above the top of the federal funds target range”

That means it will be set above IOR (currently 2.35%), which is below the top of the FFR (Fed Funds Rate) range (currently 2.5%). Doing a repo to get reserves that pay 2.35% and having to pay > 2.5% on the repo is most certainly not free money. They are setting the rate above the top of the FFR range so that normal behavior would be to borrow needed reserves more cheaply in the Fed Funds market.

The article implies they will discount the security, i.e., the bank will not receive face value for it. I would think it reasonable to assume a discount something along the lines of margins set for the Discount Window. See

This proposal is not clear. They are talking about draining reserves from the system but QT must continue for that to happen, which will also drain M1 (and the markets aren’t going to like that). Reserves cannot be destroyed by the banks buying Treasuries. They can only cause them to be reclassified. When a bank buys a Treasury it reduces reserves TEMPORARILY. The reason it does this is the reserves “move” to the Treasury Account, which is a liability to the FRS just as reserves are – it is a reclassification of an FRS liability. But as soon as the government spends the funds they “move” back to the reserve liability from the Treasury Account. This process will “drain” excess reserves as it usually (as long as the government payment is to a non-bank) creates M1, thus increasing required reserves (and obviously lowering excess reserves). But it does not change TOTAL reserves. They don’t mention QT in the article so exactly how this all fits together is unspecified.

The banks have to pay for the funding that they “deposit” to the Fed. And they’re generally paying more than Fed Funds and T-Bills.

So I don’t see how this is ‘free money’ for the banks. If anything, it costs the banks’ shareholders to place deposits into this facility.

If the Fed were to eliminate this program, then the banks would either return funds to depositors, or the banks would buy T-Bills.

You are half right. The banks do have to “fund” their excess reserves. Even those excess reserves created by QE originally had to be funded when the original (pre-QE) asset was put on their books. However the TBTF mega banks’ overall funding costs are quite a bit lower than the Fed Funds rate, leaving them with a nice spread that is totally risk free and attractive enough to them so that the excess reserves just stay on deposit at the Fed.

The system is set up to make bankers rich at everyone elses expense. Anyone who sees it any different must be a banker.

So you reckon a Fed guaranteed bid to buy your car back, no matter what market conditions are, at no less than 5% below current purchase price for the next 6 years, is not free money?

Aside from that, the fundamental reason this is “free” money for the banks, is that it is not available to all and everyone. Hence, it is yet another transfer of wealth/purchasing power from others, to the banks and those who benefit from the banks getting wealthier. After all, the purchasing power represented by the money is not “free” in any global sense. Every penny of benefit the banks gains from this, is paid by someone else, whose purchasing power is being debased in order to provide the banks with this guaranteed return.

It’s this asymmetry itself which represent the wealth transfer from others to banksters, which inherent in all a central bank does. Since simply printing Washington’s face on paper pieces does not create new real wealth, any central bank facility and policy aimed at “rescuing” or “facilitating” banking, can not ever, under any circumstance, avoid being ultimately funded by those who can not avail themselves of these facilities. Simple arithmetic is all that is required to demonstrate that “no new wealth created by printing”, and “bank made wealthier when resuced than when failed,” must add up to the rescue making someone else less wealthy.

OTOH, if things were fully symmetric, IOW if all men were still treated as equal, the problem would go away. The Fed could print money, but so could anyone else. That way, a bank faced with a “liquidity crisis” when a loan come due, can avail themselves of freshprint. But so could anyone else, when faced with a “liquidity crises” when his car payment is due. Hence, problem solved. But as long as the fundamental asymmetry inherent in “some can print/counterfeit, others can not” remains, no amount of attempting to cover up the graft with obfuscative jargon and pointless roundabout excuses, can ever pass even the most basic test of simple arithmetic.

Your M3 money at work.