Ten years after Lehman there are numerous statements from bureaucrats, academics, media and others that banks are now better regulated, more solid and liquidity problems vanished.

Reader Lars from Norway Emailed this assessment today.

Price/Book Ratio

Deutsche Bank trades at 0.30 on the low side and BNP Paribas at 0.70 on the high side. In between we have Commerzbank at 0.40, Unicredit at 0.50, and Society General at 0.50.

The verdict is negative.

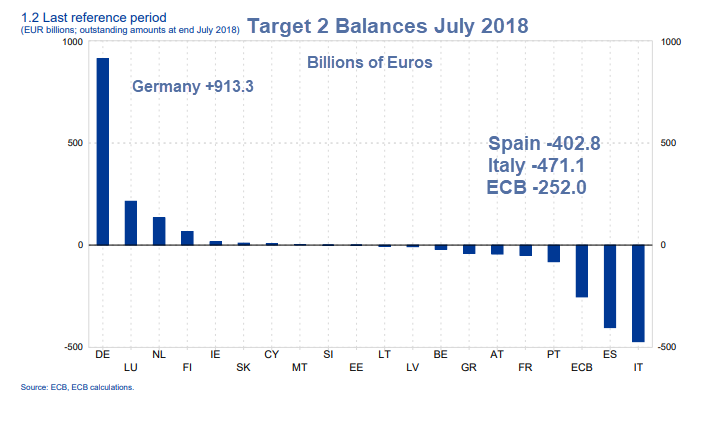

Target2

Italian and Spanish bank require € 900 billion in liquidity support on a permanent basis.

This element is mostly ignored by academics and others because they do not understand the implications of Target 2 as a capital flight phenomenon. This is a hidden crisis.

The verdict is negative.

Nonperforming Loans

Italian banks would all be insolvent if NPLs were to be written off. In order to keep the facade, NPLs are kept on the books as if it’s not a problem.

The verdict is negative.

Proprietary Trading and Derivatives

Some of the banks have huge portfolios, led by Deutsche Bank and BNP Paribas. As much as 45% of total assets.

Nobody knows what a strict mark-to-market exercise would lead to. Most of the derivatives are interest rate swaps that might suffer should rates rise.

The verdict is negative.

Emerging Market and Troubled Bank Exposure

French banks have huge exposures to Italy, and Italian banks have big exposure to Turkey.

The verdict is negative.

Contagion Risk

We learned from 2008 that interbank markets can freeze. Liquidity is no longer available. How much more than the € ,400 billion is the eurosystem willing to provide to insolvent Spanish, Italian and Greek banks?

Conclusion

Its a fools game to predict the future but to claim that banks in Europe are in good shape is far fetched.

Should Deutsche Bank fail we do not know the ramifications. Bundesbank may intervene but confidence will take a serious beating. And we know that everything is based on confidence.

Just a few thoughts from Oslo as a reaction to numerous naive statements out there on todays situation.

Regards

Lars

Thanks Lars

Mike “Mish” Shedlock

The obvious end result will be the ECB purchasing trillions of bad debts. The same thing the FED did.

Since Deutsche Bank is such a basket case that leads to the fact that Germany will allow ECB to do whatever it wants to save insolvent banks in Italy, Spain, Portugal, France, Austria and Greece.

This should show in Euro being much lower that it is currently because there will be massive creation of Euros and purchases of all kinds of crap bonds by ECB to save the insolvent banks including Deutsche Bank.

Very possible and German industry is helped by lower Euro whilst the electorate are blind to what is happening whilst told it’s all to protect them.

Ad-hoc = guess in my book. Worth a read, below. No winners.

“The European Banking Authority calculates that to comply with the new framework, E.U. banks will need to raise another 12.9% of tier 1 capital to meet the minimum requirements, amounting to €39.7bn.

This EBA assessment is based on an “ad hoc monitoring exercise” it undertook using data from 88 E.U. banks. The impact will be greatest on the 36 biggest banks in the survey: collectively they will have to raise an additional 14.1% tier 1 capital – a significant sum. However, the other 52 will only have to raise another 3.9% – which is less significant.

Mr Hills says “it remains to be seen as to whether there will be winners and losers amongst individual banks”. However, the situation already seems clear cut – there will be no winners, only losers and even bigger losers. As the EBA exercises shows, smaller banks lose because they have to find a bit more capital; bigger banks lose because they have to find a lot more.

About the author: Michael Imeson Chartered MCSI is Contributing Editor of The Banker magazine; Senior Content Editor at Financial Times Live where his role is to organise and/or chair events on financial services; and the owner of editorial services agency Financial & Business Publication. Michael is also a regular contributor to Wolters Kluwer’s Compliance Resource Network.”

Don’t mention Basel IV too, need to raise more capital buffers in European Banks. Someone, somewhere has to cough up cash to help meet capital requirements and/or some loans won’t be made.

Knowing precisely what extra capital will be needed is none too easy if some of the current borrowers are on life support from the ECB and tightening starts. ECB supported zombie corporations suddenly become new NPLs and the amount of capital needed increases.

Oh, not to mention the impact of South America on Spanish banks.

AVOID.

In other words, the ECB is trapped in a perpetual policy of Zero Interest Rates. Suits Deutschland just fine, as far as their export industries are concerned.

Currently reality doesn’t matter, perception and narrative do.

Reality will one unknown day crash through the facade of perception and narrative and then what?