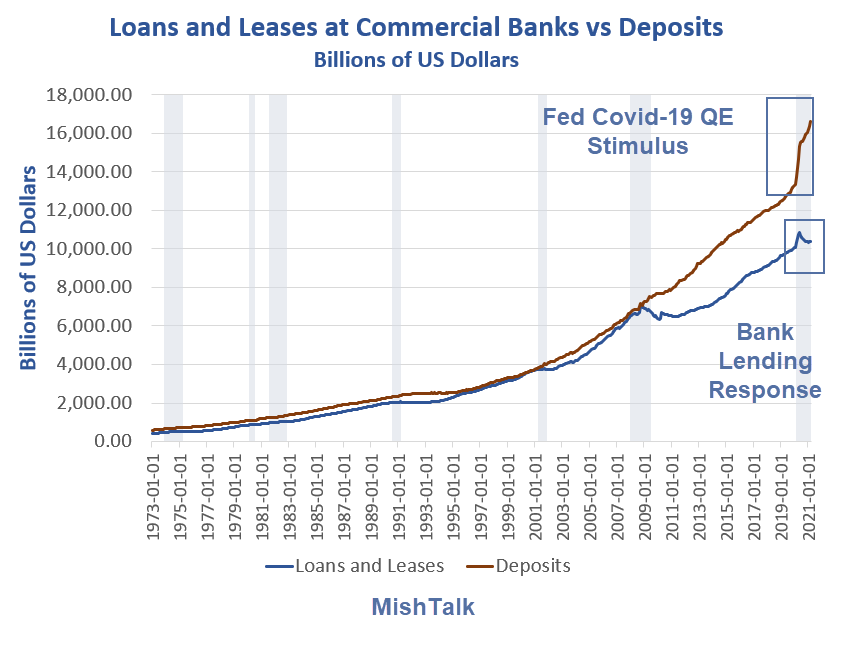

Bank Lending Since the Pandemic

What’s Going On?

That’s a good question and poor answers are easy to find.

For example, consider the Bloomberg headline that inspired this post: Biggest U.S. Banks Pile Into Cash, Securities as Loans Fall

The teaser: “The four largest U.S. banks sucked in a tremendous $919 billion in additional deposits last year during the height of the pandemic. Here’s what they did with it.“

Three Word Synopsis

Wrong, Wrong, Wrong

Banks did not “pile into cash”. Nor did they “suck in” deposits.

Rather, the Fed crammed money down the throats of commercial banks via QE policy although the banks have little demand for loans.

What’s Behind the Surge in M1 Money Supply?

On January 7, 2021, in What’s Behind the Surge in M1 Money Supply? I explained the surge in M1 is due to QE.

I later found a confirming New York Fed article with nearly the same name. Here is the key snip from the New York Fed.

M1 growth is highly positively correlated with the growth in reserves generated by Fed asset purchases. The reason for this is simple: Reserves held with the central bank are assets for banks. As the Fed expands reserves, banks must either sell other assets (keeping the overall level of assets unchanged), issue more liabilities or equity (expanding the level of assets), or some combination of the two.

Banks Don’t Lend From Reserves

The above charts are misleading in that banks do not lend from reserves in the first place.

Rather, banks lend when they believe they have creditworthy customers who seek loans. Alternatively, banks will lend if the assets pledged as collateral will cover any expected losses.

The banks can and do make mistakes regarding creditworthiness and collateral as happened with housing loans prior to the Great Recession.

There is one additional lending requirement. Banks do not lend if they are capital impaired. That is not the case here.

Bank Lending Current State of Affairs

Q: Why Aren’t Banks Lending?

A: Banks do not have creditworthy borrowers who want loans.

Cramming more money down the throats of banks has not and will not stimulate lending.

The ECB also found this out in spades with their negative interest rate policy that still did not stimulate lending.

What About Housing?

Banks are largely out of the mortgage business but it would not matter if the banks got back into mortgages.

Q: Why?

A: Fannie Mae and Freddie Mac still make mortgage loans. Shifting the loans from Fannie and Freddie to banks would not increase net lending.

Bank Lending as a Percentage of Deposits

Hoarding the Cash?

It’s important to understand that banks don’t lend from deposits. The Lending actually comes first.

Nonetheless, banks are sure to be accused of “hoarding the cash” the Fed has crammed down their throats.

Why So Little Demand For Loans?

Questions are pouring in today.

Inquiring mind want to know why with interest rates so low is there so little demand for loans.

A series of questions will serve as the answer.

- Who wants to start a restaurant now?

- With more people working at home, do businesses want to expand office space?

- How are malls doing?

If housing stalls for any reason, the Fed will have a huge problem. Meanwhile, the bread and butter of bank lending has stalled.

This is yet another reason the recovery is not as good as appears on the surface.

Related Articles

- Housing is Going Gangbusters, Thank Covid-19 and the Fed

- Retail Sales, What’s Hot? What’s Not? And What About Amazon?

Two Key Ideas

If you hand out free money, especially to those who are working and suffered no job loss, people will find a way to spend it. Then what?

This surge in online sales and work at home is a big disinflationary if not deflationary force.

For further discussion of disinflationary trends please see comments from Lacy Hunt in my discussion Expect Inflation to Accelerate? Here’s 8 Reasons to Expect Decelerating Inflation.

Add this post on bank lending to the discussion of deflationary forces.

Mish

Good!

re: “Why So Little Demand For Loans?”

It’s perfectly obvious (as predicted). Both stagflation and secular stagnation were predicted in 1961. Unless monetary savings (income not spent), are expeditiously activated, a dampening economic impact is exerted. From a macro-accounting perspective, all bank-held savings are un-used and un-spent, lost to both consumption and investment, indeed to any type of payment or expenditure.

The demarcation began in 1981 with the “S-Curve” hybrid dynamic damage (sigmoid function), or the culmination in the “monetization” of time deposits by the first half of 1981, with the widespread introduction of new negotiable demand drafts, e.g., the effervescent “saturation value” of ATS, NOW, Super-NOW and MMDA accounts (i.e., the end of most DFI gate keeping and gov’t regulatory interest rate restrictions on bank deposits).

So, what you are left with is secular stagnation, chronically deficient AD. Any increase in bank-held savings destroys money velocity. Banks are “black holes”.

Q.E. and changes in reserve requirements in no way change a bank’s balance sheet. Equity is still assets less liabilities

Looks like they decided to make an example out of Mr. Chauvin….guilty on all counts.

Not too surprising. It will be interesting to see if that matters after nightfall.

Thank g-d. Never has a verdict been as obvious

Well, yes and no, Sechel.

Yes, the video was damning, as was much of the testimony. However, Floyd was a drug addict with lots of fentanyl in his system, and he was sick, and he had a serious heart condition.

Also, there was no real smoking gun as far as to whether what Chauvin did was enough to kill him. The prosecution witnesses said it was. I expect the evidence offered by the actual medical examiner (who said Chauvin killed him) weighed very heavily.

In one sense it’s an easy out for all concerned, and politically it’s very expedient. Maybe the harsh verdict will quell the violence. I hope so.

So Floyd could have died at any time but chose to die under Chauvun’s knee. Only one direct cause. With your logic Jesus didn’t die from crucifixion but from high blood pressure

I think that’s gilding the lily a little bit. Jesus wasn’t a junkie AFAIK.

All I’m saying is that there were other contributing factors in Floyd’s death besides Derek Chauvin’s knee. I’m glad I wasn’t on the jury. I wouldn’t want to have to make the call they made, and I’m not even saying they were wrong.

But my understanding of the murder two charge is that you have to actually have INTENT to kill in order to be guilty of that on. I can’t see how or why Chauvin would have had that kind of intent.

Former Minneapolis police officer Derek Chauvin was found guilty of second-degree unintentional murder, third-degree murder and second-degree manslaughter by a jury Tuesday for his role in the murder of George Floyd last May outside of a local convenience store.

I suspect the Jurors just ran for their lives (guilty on all account) and kicked it down the road. Can’t say I blame them.

It will get appealed and re-tried in a year or 2 in a different venue once everyone has calmed down. At that point he’ll be convicted on a lesser charge (manslaughter 2 fits exactly what happened).

So you’ve decided the jury convicted an innocent man. Interesting…

Your putting words in my mouth. I sad he was guilty on 1 of the 3 charges.

#1 is essentially what you get if you kill someone while robbing a bank (kill while committing a felony)

#3 would require showing Chauvin had a depraved mind. That would require psych evals and lot of other things to show depraved mind.

#2 perfectly fits what happened. Chauvin died while in his care due to unreasonable risk (knee on neck too long).

You don’t understand the legal meaning of “depraved mind”.

Minnesota 609.19 MURDER IN THE SECOND DEGREE.

Whoever does either of the following is guilty of murder in the second degree and may be sentenced to imprisonment for not more than 40 years:

(1) causes the death of a human being with intent to effect the death of that person or another, but without premeditation; or

Not guilty of that. I saw no evidence presented that said he intended to effect the death of Chauvin. Most of the prosecutions case rested on the video of knee on neck causing death. Not on motive or possible motive.

Same with depraved mind. I saw nothing about that in the case at all. Half the country can be described as anti-social (pretty much any introvert). Knee on neck is not a knowingly dangerous act. It’s done ALL THE TIME by police forces. It’s legally sanctioned (rightly or wrongly) so it can’t be a knowingly dangerous act with reckless abandon.

Let me ask you this, if it was a White Cop on White person or Black Cop on Black Person do you think this case gets this publicity AND this specific conviction? I say not in a million years. It would get the manslaughter charge which is pretty what most people (my black and white friends) I talked to thought would happen. This gets appealed obviously and will be re-tried again in a couple of years (while Chauvin sits some place in protective custody) in a different venue when things have calmed down.

In these days, video rules…actions without regard to a dying person beyond the point of incapatation requires consequences.

So sorry you’re disappointed by our trial system..are you going to loot a Target tonite?

…..a depraved mind involves “a knowingly dangerous act with reckless and wanton unconcern and indifference as to whether anyone is harmed or not.” It was also described as “a state of mind just as blameworthy, just as anti-social… just as truly murderous as the specific intents to kill…”

Living life, seeing what scams and schemes they can get away with.

That describes both Floyd AND Chauvin.

You are aware that Chauvin claimed to be a full time Florida resident while working full-time for Minneapolis for the purposes of real-estate schemes and tax evaision. Voted illegally in Florida, for those of you who are worked up about voter fraud. Knew Floyd–worked along-side him as security in a bar at night on the side. Had disagreements with Floyd previously at the bar.

Original police report…

Unfortunately, from the smallest jurisdiction to the national courts, justice is what is chosen to be enforced by the power that be, not what is law.

All the way from the cop letting his buddy off the red-light violation, on up….

Unrelated to the switch I cannot post new articles. There is an authentication outage somewhere affecting me, TheStreet, everyone.

Here is a viewpoint that I endorse

The verdict of a ’13th juror’ on Chauvin — and the trial

We must strive to respect the rule of law, even though our politicians don’t.

Paywall, unfortunately.

Looks like the verdict is in already. Obviously means it was a slam dunk in the mind of the jurors. The question is which way.

My guess is he gets 1 lesser charge (Second-degree manslaughter is causing death by unreasonable risk).

In either case, expect appeals that will drag on for a very long time.

The jurors took an oath of impartiality & discharged their duty in a highly charged case; their service should be praised by all. Still, I’m very surprised that venue wasn’t changed, given the possible implied pressure on any jury to avoid a repeat of what occurred in Minneapolis last year. The task of guarding against that danger falls on the judge, who determined that such danger was not material. I would’ve probably come to a different conclusion, but — given the record before him — I don’t think he necessarily erred.

Are email alerts for posts going out?

I do not see any email alerts as of yet.

In my case banks are throwing 0% cards at me so I live on their dime and invest the rest until the 0 is up.

also have banks making ridiculous offers to refi my house. Locally they are keeping the loans and not selling them to the gov’t. Could have used the forbearance to keep more cash but I’m doing ok, no need to push it

REIT’s suck in money and disburse wads of cash.

REITs still building like mad, hoping no-one catches on.

I can’t figure out Maven. I’m pretty sure I should have received an email for this post and it says that I’m “Following.” There aren’t any places that I can see that say, “Turn on Notifications.”

Sold the GLD in the fun trade for a modest profit. I think the dollar might be turning back up…..at least for the daily cycle timeframe. The bounce today looked like a good place to lock in recent gains.

Asset prices will not be allowed to decline like in 2008 and 2009. No way no how.

I’d guess that assets speculators are still borrowing, given rising prices for stocks and land, but there are trends that lead to a contracting economy and hence less demand for consumer and business lending :

And then COVID over the top and further kills demand for services and travel as well.

Interestingly folk who do have spare money seem to be at a loss on how to spend it and the prices of collector items, such as vintage cars even push bikes has shot up in the last year.

Low rates themselves kill lending and thats the trap of Japan and the Fed.

Low interest rates cause high prices and low yields. High interest rates cause low prices and high yields. As high interest rates have no change other than down, so low interest rates have no change but up. Anybody taking a loan in a low interest environment faces the consequence of high interest on a high price.

This is the point of QE. Its effectively a manipulation of the interest rate below zero to maintain the trend. Whats worrying is that as a policy it doesn’t clearly doesn’t work because lending still hasn’t restarted after a !decade!

The cause was preventing the crash in valuations to restart.

And the risk is clearly, in the end, inflation. And how will the Fed be able to deal with inflation with interest rates when the money in the economy has no counter-party loan. Its positive money. There is no attached debtor to provide the interest.

So what to do. The only way out, whether its taken or not, is to raise interest rates and allow the crash that should have happened in 2008 to clear out the debts and motivate people to borrow to invest to renew and legislate to protect the retail bank customers. Effectively this debt cycle is an end game ponzi. Whats amazing is how long its taken. I remember saying this ends in a crash (as was the common opinion of economic blogs of the time with the usual excess of explanation) back in 2006/7 and was amazed when the central banks broke the taboo of printing funds. To think the whole mess has lasted until today. Wow.

“The only way out, whether its taken or not, is to raise interest rates and allow the crash that should have happened in 2008 to clear out the debts…”

According to Klaus Schwab and his elite “Build Back Better” sycophants, the only way out is the Great Reset, where we will “own nothing and be happy.”

“The only way out, whether its taken or not, is to raise interest rates and allow the crash that should have happened in 2008 to clear out the debts…”

According to Klaus Schwab and his sycophant elitist “Build Back Better” WEF, the only way out is the Great Reset, where we will “own nothing and be happy.”

Of coarse Schwab and his elitist friends won’t be among those owning nothing and being happy.

Would you elaborate how you see a route from deflation to inflation?

QE as government financing, inflation expectations, treasury oversupply, global real rates. If you mean what event (as opposed to cause), I don’t know. I have been in the States when the dollar was 2.10 to the pound, and life moved on. Currently its 1.39 so the switch doesn’t seem imminent, but on we go same as before.

Are PPP loans and EIDL loans tracked by that chart? The PPP’s were made by banks. Not the EIDL, that’s SBA direct lending, I think. Correct me somebody if that’s wrong.

Technically, my business borrowed more money in 2020 than any time in the last 30 years. Some of it, roughly half, stands to be forgiven, but I still took on debt that I would have never taken on had circumstances been normal.

My business was nearly debt free pre-COVID…..and with retirement for this boomer on the mid-term horizon (five years?) that’s the way I wanted it.

I might borrow to build another house….a rural house, which would have to be financed by an ag bank like Capital Farm Credit, most likely. The rates would be higher than typical mortgage interest…but with my house in town at nosebleed highs, I need to sell it.

In general a lot of small business people my age are probably like me…..a decent credit risk, but averse to taking on more debt given the EIDL overhang.

The economy doesnt need more investors buying homes.

What I was talking about is not an investment per se. It’s just the normal path to cashing out of a personal house, which was never meant to be a real investment, but has fortuitously made crazy gains that can now be tapped and the capital gains can be at least partially taken tax free. The first 500K, until such time as the Dems rescind that.

That’s what old people do in a good market. Expect to see more of it.

In terms of making investments, I see nothing wrong with owning homes, as opposed to owning paper assets with no tangible value. But right now is NOT a good time to buy in my local market.

BTW, I don’t base my investment decisions on what “the economy” might or might not need. I base them on cash flow and the leverage and the tax considerations of owning RE. My goal is only to make myself even more shockingly rich, not to end wealth inequality as it exists, or to reform the broken system.

Sorry about that, but I’m not some billionaire, just an old fart who wants to live well in his

old age.

By building a nice new home on land I already own, I enhance another asset that was never meant to be an investment either…just a place to do a little hobby farming and enjoy recreation.

But…..it does appear that it’s likely I’ll make out like a bandit on that one too, if I hold it for maybe five or ten more years and then sell it. If the 500K capital gains exemption is still in place, I’ll take it again too. Kaching.

If it isn’t, I’ll just pay the tax and net the profit, which will still be a lot, unless we fall into a real depression……in which case I’ll keep it and farm in my old age.

I own 3 properties that were never intended to be investments…..but if they appreciate in value, I have to cash at least two of them if I live long enough. I’ll keep one to live in….barring a depression, I’ll sell the farm and keep the lake house, which I’ve been working on and upgrading for the last few years.

Since very few potential assets I could buy have the kind of return I get from my rentals, I do expect to buy more of them…just not until we have a correction. Why wouldn’t I?

“What the economy needs”…….LMAO.