No Support for a V-Shaped Recovery

Please consider a FiveThirtyEight report on the shape of the recovery.

In partnership with the Initiative on Global Markets at the University of Chicago Booth School of Business, FiveThirtyEight asked 34 quantitative macroeconomic economists what they thought about a variety of subjects around the coronavirus recession and recovery efforts. The most recent survey, which was conducted from June 19 through 22, echoed many of the predictions from the last round — though there were also a few new wrinkles in their forecasts.

When we first asked about the shape of the recovery, 58 percent of respondents thought the trajectory of future U.S. gross domestic product looked like a Nike “swoosh” — a sharp downturn followed by a long, slow recovery. This time around, however, a consensus has formed around a slightly different shape: a reverse radical (i.e., a mirrored version of the square-root symbol).

Twelve of the 17 economists who had predicted a swoosh in our survey in late May changed to the reverse radical this time, leaving just five respondents sticking with the swoosh in this round of the survey. (And no economist switched to the swoosh, another sign that other patterns fit the trajectory of this economic recovery better.)

Reverse Radical

Worst Case Scenario

The economists now favor the Reverse Radical but that is an oversimplification of things, even if reasonably accurate on average.

What’s happening now does not look like the Great Recession or any recession that preceded it.

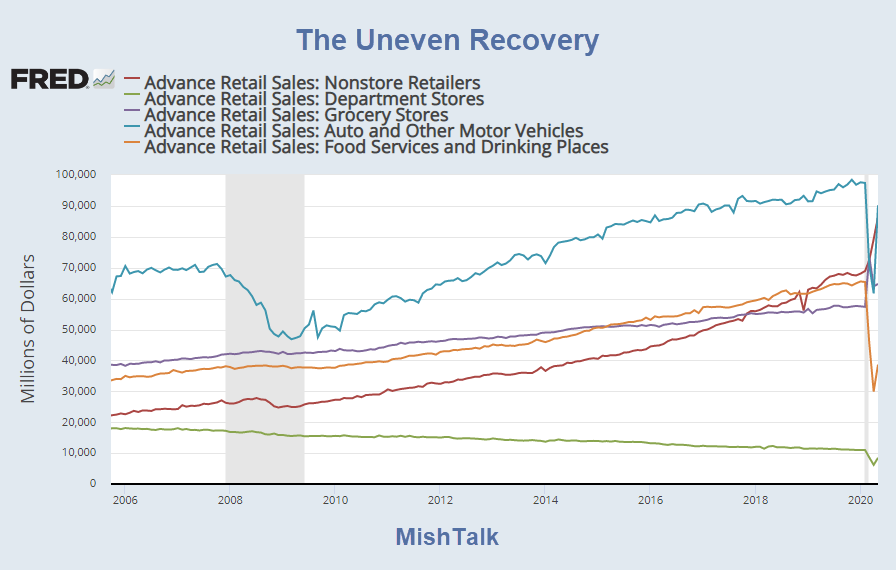

Compare the lead chart to this one.

The Uneven Recovery Detail

Can there be a recovery with no decline?

Nonstore retail sales (think Amazon) accelerated and never looked back. The worst case scenario for online shopping is the current uptrend slows.

There is nothing to recover from, nor will there be.

Grocery stores advanced in the recession but as people returned to eating out sales declined, Nonetheless, grocery store sales are well ahead on the prior trend.

That change is going to be permanent because more people will be working from home and thus driving less and eating out less for lunch.

Department stores are in a world or hurt and the trend is unmistakable. The best-case scenario is a U to the trendline before the collapse resumes.

What About Housing?

Housing has positive and negative factors in play, both short and long term.

Positive Factors

- People have to live somewhere. The population is still growing.

- There is a bit of pent-up demand. People were forced to put off moving plans when Covid suddenly hit.

- Interest rates are low and the Fed will keep them that way.

Negative Factors

- Jobs, Jobs, Jobs

- The attitudes of millennials and generation Z are quite different than that of their boomer parents towards housing and family formation.

Demographics

Aging Boomers want to downsize. There is no one to sell their mansions to.

But eventually boomers will die.

The kids who inherit the houses will each get a chunk of money and perhaps will then decide to buy a new house of condo.

I believe attitudes are the key, long term. They may change. In the short term, it’s all about jobs.

Continuing Claims

For 8 weeks, continued claims are at or near the 20 million mark. Those claims are ate the state level.

There are perhaps as many as another 10 million collecting Federal assistance.

These claimants are not going to buy a home. Most were not candidates anyway, but some were. And others who were not impacted at all may have had second thoughts.

Mortgage Applications

There was a huge surge in mortgage applications recently, but that was a reversal of the housing plunge in April and May, two of the busiest months in the year.

Throw those busy month applications into June and July and then seasonal adjustments make the rebound look bigger than it really was.

Factor in Credit Risk

With lending standards at tightest in six years, it’s easy to see a higher % of pending home indications not come to fruition because of denied applicants

To your point, pending home sales will overshoot transactions until unemployment abates which is key to income verification https://t.co/xc5zqzXBSO

— Danielle DiMartino Booth (@DiMartinoBooth) June 29, 2020

For discussion, please see Banks’ New Dilemma: They Cannot Tell Who is a Good Risk.

Also note see Mortgage Forbearances Rise for the First Time in 3 Weeks

Every Sector Will Have Its Own Shape

On average, I think the economists are correct with the Reverse Radical idea.

However, there are a small number of big winners coupled with a rising threat of bankruptcies and so many sector variances that averages mislead.

Multiple shapes is the right idea.

Reopenings in Reverse

- Drinking Banned at Florida Bars and What About the NBA?

- Texas Shuts Bars at Noon as Covid Cases Surge

Those reopening reversals are what caused over 40% of the economists to worry about a worst-case scenario.

Mish

Meanwhile, the Nasdaq looks like this:

Good article.

If they could get rid of the second wave fear porn and stop the rioting, then the country could rebound that much better, esp. if there is a massive infrastructure program in 2021.

Of course that is unlikely, given that we are now in a vicious civil war in which one sides is relying on the economy being in the toilet to so demoralize their opponents as to not only win at the ballot box, but so retool the system as to ensure that anything resembling the old Republic is buried forever. Totalitarian Utopia, here we come!!

Results from Sweden as of 7/1/20. Death rate for those under 70 = .86% and for those 70 or more = 6.8%. Time to protect old folks and go back to work.

Two things.

One, contracting virus is not binary – die or live normal. Stories seeping out even asymptomatic positives have health problems once negative.

Two, the liability issue re business needs to be answered.

The importance of an effective vaccine cannot be under-stated.

As I have said from the beginning, this will be a long-term issue with portions of the economy blinking on and off in response to spikes. Supply chains will remain disrupted. Productivity will not be strong. People have to be confident in order to spend money. Until certainty returns to the economy, it will remain shit. The helicopter dump of federal money to individuals and programs used by individuals will need to continue to keep this ship above water until a vaccine or some sort of other end to this pandemic will occur.

But now, with the rise of the anti-masker, anti vaxxer components of society (not necessarily the same group), there are further wild-cards being thrown into the mix.

Even if it is decided to let the chips fall where they may “because we’ll all get it in the end”–there WILL BE long term effects. How many small and medium businesses with no viable succession plan are out there that depend on people in high risk categories? How many families depend on those people? What about the people who end up in the hospitals–who’s going to pay those bills? And how confident are you that you won’t get it a second time? How confident are you that the damage you receive the first time (and studies DO show long-term damage in even asymptomatic people) won’t mean a worse time with a second bout?

Too many unknowns.

But all risks to the downside.

But hey, I’m up over 6% total for the year in my investments.

Did you mean “The importance of an effective vaccine cannot be over-stated.” ?

Yup, my bad….

Fool’s gold.

recovery? nasdaq is at new all time highs. there is nothing to recover from. you snooze, you lose.

Ditto the IBC index in Venezuela. The Venezuela “economy” and “markets” are rocking!

Trump and Maduro are, like, the Dearest Leaders evvah!!

Yep, we’ll need some confirmation though from earnings release.

well, you can sit around and wait for earnings if you like. again, you snooze, you lose. all aboard the stock market expansion train.

The expected hit to GDP 8-9 % downward, the FED and fiscal stimulus 14% of GDP, looks like to me asset prices will run upward in the short term. Asset prices tho are not the “real” economy.

“There was a huge surge in mortgage applications recently, but that was a reversal of the housing plunge in April and May, two of the busiest months in the year.”

…

Waning already?

“Mortgage applications fell last week despite mortgage rates hitting another record low in MBA’s survey. Investors are contemplating the risks of the recent resurgence of COVID-19 cases to the labor market and economy, and Treasury rates and mortgage rates are moving lower as a result,” said Joel Kan, MBA’s Associative Vice President of Economic and Industry Forecasting. “After two months of strong growth, purchase applications declined for the second week in a row. The weakening in activity is potentially a signal that pent-up demand is starting to wane and that low housing supply is limiting prospective buyers’ options. The average purchase application loan size increased to a record high in our survey – more proof that tight inventory conditions are leading to faster price growth.”

Many people who took 30 year low-down-paykent mortgages without a second thought a year ago are now likely pausing to consider what such a move would mean for them if they lose their jobs, see their pay cut, or see their employers pivot to a work-remotely model.

“On average, I think the economists are correct with the Reverse Radical idea.”

…

Really?

What bounce we’ve had courtesy of almost $3 trillion in fiscal stimulus (a lot still to be spent) and probably another $1 trillion or so when Congress passes something this month + huge amount of forbearance / moratorium. When all that starts to wane (H2 and 2021)?

The country as a whole has spent the last 11 years since GFC taking on massive amount of debt to paper things over. Payback coming. As delinquencies / defaults surge (and stimulus wanes) credit will tighten … then economy will settle lower.

Labor arbitrage was a big deal in the last couple decades. But now consumers who are tapped out and unwilling to borrow more money to pay union labor overtime prices for Chinese produced stuff are going to demand the China price for that stuff.

Arbitrage killed the golden goose of premium pricing.

Case in point: Henceforth, Apple will be selling way more $300 Chinese-made phones than $1,500 Chinese-made phones, and customers won’t be going into debt to finance those $300 phones over “24 easy monthly payments” like they used to. That’s why Apple is pivoting to trying to use its App Store monopoly to extract more monopoly rents from companies who offer services on Apple devices. That’s where their future profit growth will come from.

The same will be happening in many other industries.

Here in rural NC homes have not slowed at all. In fact, they are accelerating.

I’m a property manager, and the primary driver of the property acceleration in my area is people moving here from more densely populated areas (think NYC and New Jersey).

A person moving here likely has a pension that goes much further here than it does where they currently live. It will be interesting to see how that may change if 1. The pension bubble pops and 2. COVID changes mindsets from moving to the city back to moving to rural areas.

“In fact, they are accelerating.”

…

No doubt.

And in urban areas (aka – where the $$ is)??

In the urban areas where the $$ is (which are by definition the areas where those receiving the largest welfare checks live), the Fed will pick up the tab. Funding it, as they always do, by increasing the robbing of those in areas where the $$ are not.

Until those in the latter, are both truly flat broke, AND no longer willing to even supply the slave labor required to keep the delusion alive, that process will continue. No different from how things have been for the past 50+ years.

Sorry, but that’s not even remotely close to how it has worked for the last 50 years.

Metropolitan areas with productive economies in blue states have been net payers into the system; rural areas with less productive economies in red areas have been net collectors of the production of blue states.

Very few red states are net contributors to the federal government — in fact, most are voracious consumers of the surpluses paid in by blue states like NY, CA, IL, MA, etc.

More data here for your edification:

Now what could possibly be more productive than sitting idle one ones rear while The Fed pumps up ones “home vaijue…”?

Maybe…. doing utterly useless makework picking random numbers while collecting Fed welfare in the form of pumped up “assets”, on “wall street?” Or in a “fund?” Or, perhaps, Trump style, selling 300K condos to those receive such welfare by the bucket load, for $5million? Safe in the knowledge the Fed and government will ban anyone else from building the same thing next door and sell it for less…. Massive amounts of productive work, going on right there….

THE, FAR AND AWAY, primary engine for redistribution of wealth, in financialized dystopias, is debasement. It’s not “taxes,” even though those do play a part a swell. Debasement driven redistribution, is how purchasing power is stolen from the productive, and handed to the idle and connected connected. Specifically BECAUSE this allows those receiving the loot, the connected, to flaunt their economic utter illiteracy by spouting nonsense about “which states have surpluses.” And hence flattering and fooling their stupid selves, by pretending any of what they did with their life was somehow “productive.” Makes them feel better in their blissful ignorance that way, I suppose…. Never mind none of them actually “produced” anything.

The so called “surplus states” are, invariably and virtually without exception, the same states where people have gotten wealthier NOT FROM producing, building, creating, extracting, growing etc. anything at all. But, instead, from simply sitting idle on their rears, while the Fed and government has robbed those who have done any of the above, in order to hand the loot to the connected idle. (Maybe some small, resource rich states, like Alaska, is an exception…)

Fed pumped up “asset appreciation”; mandated “insurance” for productives, so that ambulance chasing produce-nothings have something to loot and other idles can make money from the “insurance” rackets etc. etc; has exactly nothing whatsoever to do with productive anything. And this is how wealth in America, pretty much all of it, has been redistributed over the past 50 years. From those who actually produce anything at all. To pure, Fed and government dependent deadweights.

Who do you think did the productive work, required to create the purchasing power increase accruing to someone sitting idle, on his rear, in a Manhattan condo for the past 50 years came from? Santa Claus? Roaches in his wall working hard doing productive stuff? Magic?

In the real world, someone had to create, by producing something, every penny of that purchasing power. Then that someone had to have it stolen from them. So that idle deadweights closer to The Fed and government, could live large from doing nothing productive whatsoever. While pretending picking random numbers, playing courtroom drama with others whether said others want to or not, receiving bailouts and subsidized interest rates, banning other people from putting roofs over their kids heads etc., in any way whatsoever have anything to do with “productive.”

Great post.

“In the urban areas where the $$ is (which are by definition the areas where those receiving the largest welfare checks live), the Fed will pick up the tab.”

…

Maybe. My point is that “the rich” city dwellers are fleeing to rural areas. If they move there, why would the Fed save cities (if they fall into disrepair populated by the poors)?

You make a good point.

Latin America has been ahead of us wrt societal development (Peron beat Johnson and Nixon by almost a generation), and developments there do bear that out: Most parts of most cities, will be largely abandoned by the Fed welfare rich and their security apparatus; as they retreat to easier to guard gated enclaves outsode cities, as well as to fortified rural retreats in areas cleansed of possibly threatening “natives.”