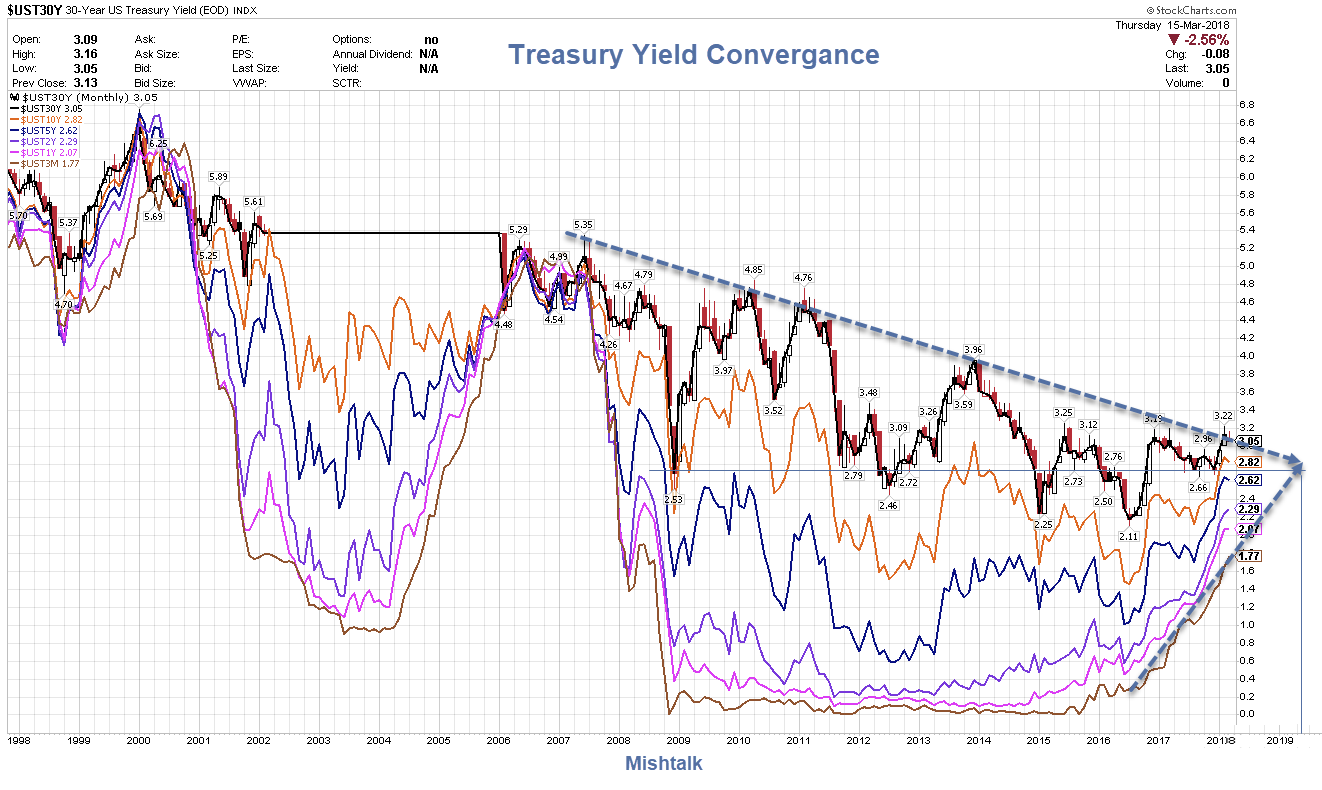

At the current rate, the US treasury yield curve will achieve perfect flatness in mid-2019.

That’s what the long-term trend on the long-side, coupled with a shorter-term trend on the short-side suggests.

The convergence point is approximately 2.72% in mid-2019.

I am quite sure that won’t happen in the 2019 timeframe, but it could easily happen this year.

All it would take is three rate hikes in 2018 with the rest of the curve not reacting.

That’s not my call, but the more aggressively the market prices in future rate hikes, the more likely it is.

If we get to that point, we will be on the verge of economic collapse.

Inflation is in the Rear-View Mirror

Those looking for a huge inflation boost fail to understand credit dynamics.

Austrians who only look at money supply keep expecting pent-up inflation. The Monetarists at the Fed (central banks in general), are clueless about the situation they fueled.

Perhaps we get consumer inflation for a quarter or two, but inflation is in the rear view mirror, primarily having impacted asset prices, not consumer prices.

Rising interest rates are already starting to impact the housing market.

The auto market, home supply markets, and consumer credit in general got a temporary housing boost.

What’s next won’t be pretty, and almost no one sees it coming. They can’t. Inflation is in the rear-view mirror.

What economists expect to happen, already has. They don’t see it because they do not understand what inflation really is.

Weakening Economy

The economy is weakening and the Fed, fearing inflation is hiking right into it.

- March 16: Housing Starts and Permits Well Below Most Pessimistic Estimates

- March 16: GDP Forecasts Dive: GDPNow Forecast Dips Slightly: Baseline 1.8%, Real Final Sales 1.1%

- March 15: Import Prices Rise 0.4%, Exports 0.2%: Bond Yields Mostly Yawn

- March 14: Confidence? Retail Sales Down Third Month

- March 12: Synchronized Global Growth is Ending: Shocks Come Next

- February 28: Pending Home Sales: Pending Sales Unexpectedly Dive to Lowest Level in 3.5 Years.

- February 27: Durable Goods: New Durable Goods Orders Dive 3.7%

- February 26: New Home Sales Down 7.8%: Six Reasons Sales Can’t Break Out

I can find only one good hard data report in the past few weeks: Industrial Production. Add jobs if you like and call it two.

However, real median wages have fallen in seven of the last eleven years!

This helps explain the falling savings rate. It certainly does not support consumption.

Debt Deflation Coming Up

I expect another round of asset-based deflation with consumer prices and US treasury yields to follow.

Buy long-term treasury calls or long-duration Treasury ETFs.

The higher rates get, the better those calls and ETFs look, even if we do not hit convergence.

Mike “Mish” Shedlock

There are other fundamental reasons that might lead to higher rates – whenever a boom leads to sufficiently pronounced imbalances in the economy’s capital structure, interest rates will begin to work their way back to the natural rate which is determined by actual society-wide time preferences. Empirically the Fed tends to follow rather than lead such trends.

How brain dead does one have to be to buy long term govt debt?

Think you have it right Mish, I was just looking at treasury ETFs, as a way to play LIBOR with the flattening yield curve. LIBOR peaked at a bit over 5% in 2007. With the Fed doves as hawks, and no inclination (stated) to back off the rate hikes even if the economy slows. Personalities aside, the tax cuts are causing a credit squeeze in Europe and we use their rates as well as ours, so the end of days is near. Counter intuitively TIPs seem to prefer a low nominal rate environment.

In theory, yes. However, the FED can always launch another round of QE and just buy the issue themselves.

To what degree does supply of government debt affect the interest rate? More supply should mean higher rates in spite of FED efforts, right?

@AWC

The debt added over the past 40 years have served two purposes: To encourage wasteful, unproductive malinvestment, and to transfer of the “share of America owned,” and “share of Americans’ purchasing power”: From those who have created, and is creating, whatever decreasing amount of value has been/is being added, to those contributing nothing but who are situated closest to the money printers.

Neither development of which there would arise any real, lasting, negative effect from simply reversing overnight, however harshly, as of yesterday. The only focus needed, is on vastly streamlining bankruptcy processes. In order to smooth the transition to a more productive, more equitable, less extractive and destructive America. Rather than fighting to preserve the falling off a cliff cleptocracy that is all the current US is, while pretending any feature of that abomination has anything in common with economic well being.

Smart/ precision bomb : S&P % off the high -10.16%, – as first leg, not the peak to bottom, – is the largest ever? Bigger than 1929, 2007, 2010, 2011 and Oct 2014. The counter leg up is about over and a very major leg 3 down will follow. The US treasury switched to the long duration and fill ordnance to max, preparing themselves for a long slog down ==> in half a year gov debt up by 1 T to $21T, debt to GDP = 21T/20T.

Yep. Record debt and a negative yield on government debt gives us a massive deflation. No doubt about it.

There is no risk in he horizon, a gov shutdown can change everything.

Considering we have had a 40 year, at least, period of almost unbroken artificially low interest rates, no amount of hiking will bring about anything resembling an “economic collapse.” No factories nor infrastructure will go up in smoke, almost no matter how high interest rates go. No workers’ skills will be forgotten, no natural resources will evaporate….

All an additional 50 to 100 rate hikes this year will do, is flush out some economically destructive malinvestment, and allow for a more accurate, less manipulated pricing of labor vs capital. Hence be economically beneficial. People will be incentivized to create genuine value, rather than attempt to use the government and legal system to seek unearned rent. Which, tah-dah, will result in more genuine value being created. Which is just another way of saying the economy will get stronger. Not weaker. And certainly not collapse.

I do not read Jeffry Snider. But if he says banks, not the Fed, control the money supply he is pretty much on target.

Have you read articles by Jeffry Snider? It is the banks that control money supply and therewith the economy. They are more carefull now with extending credit and rightly so. The big problem is the crazy debt level, which has only increased after the financial crises. There is no easy way out of it and the longer lowering it is delayed the nastier it will get.

Yes, the economy is weakening. ECRI has been warning about that already for some time. Now the facts come rolling in. But prices are also going up. The FED has a big problem. It has to keep inflation in check, but also keep the economy going and in the back of their head is the big price tag for the goverment if interest rates go up. My guess is that the FED will mind the economy and price tag the most, leading to increased inflation expectations and increased long term interest rates.

It’s not the convergence – It’s three more hikes into a weakening economy

Mish, what would be the connection between such a convergence and imminent economic collapse?

Bam, I believe you have it nailed. They are lying about their reasons even though they are stupid enough to still believe in the Phillips Curve.

I personally don’t think that the Fed is hiking because they “fear inflation”. That is what they want people to believe. They are hiking because they are desperate to get as far above the zero bound as they can before this “recovery” comes to an end and the next recession begins. Because of the asymetrical nature of their monetary policy, they now find themselves in the position where they are forced to hike into increasing economic weakness. I think they are deathly afraid (and rightly so) of what might happen geopolitically if they ever adopted a negative interest rate policy.

Yup. I have a 30% allocation to TLT, with almost nothing in general equities but some in gold miner ETFs and stocks.