Lira Plunge Resumes

#Turkey Lira keeps falling as #Qatar currency swap agreement fails to stop the Lira rout. The deal is first step after Qatar’s $15bn investment pledge to Turkey. pic.twitter.com/LdK82ebU2o

— Holger Zschaepitz (@Schuldensuehner) August 20, 2018

Interest Rates top 20%

#Turkey rout continues w/ Lira keeps falling and 10y yields risings as Germany not considering financial aid for Turkey, spokesman says. pic.twitter.com/D2vFT2Nw6i

— Holger Zschaepitz (@Schuldensuehner) August 20, 2018

There was a rumor Germany would come to the aid of Turkey. That rumor seemingly died today.

Robin Brooks Thinks Lira is Undervalued

A large negative credit impulse is shaping up from preliminary data for Q3, which will weigh on activity and compress imports, adding to the positive impulse to export volumes from Lira undervaluation. pic.twitter.com/Pvqva5FVaM

— Robin Brooks (@robin_j_brooks) August 20, 2018

Current Account Surplus

Our trade model — which feeds Lira depreciation into export volumes based on historical betas — suggests that the underlying current account could even be in surplus. External fundamentals — relevant for the Lira — are improving rapidly, at the cost of output loss. pic.twitter.com/megmqIvENs

— Robin Brooks (@robin_j_brooks) August 20, 2018

Switched Position

We spent much of 2018 being bearish on the Lira, since our models showed it to be overvalued. But at these levels the Lira is cheap on a fundamental basis. So we have been on both sides of the issue, just something I want to emphasize. pic.twitter.com/w8DH7qwijs

— Robin Brooks (@robin_j_brooks) August 20, 2018

Yesterday’s Story

Last year’s credit boom took Turkey’s current account pretty much to the bottom of the range across EM (red). But that is also yesterday’s story. A large adjustment is underway that — together with big Lira depreciation in real effective terms — could narrow the deficit a lot. pic.twitter.com/XoiR926OM7

— Robin Brooks (@robin_j_brooks) August 20, 2018

Yes, But Liquidity in Short Supply

The current account deficit is likely poised to disappear thanks to the lira ‘s depreciation and a coming credit crunch (see @RobinBrooksIIF). But the system is still potentially very short fx liquidity.

— Brad Setser (@Brad_Setser) August 20, 2018

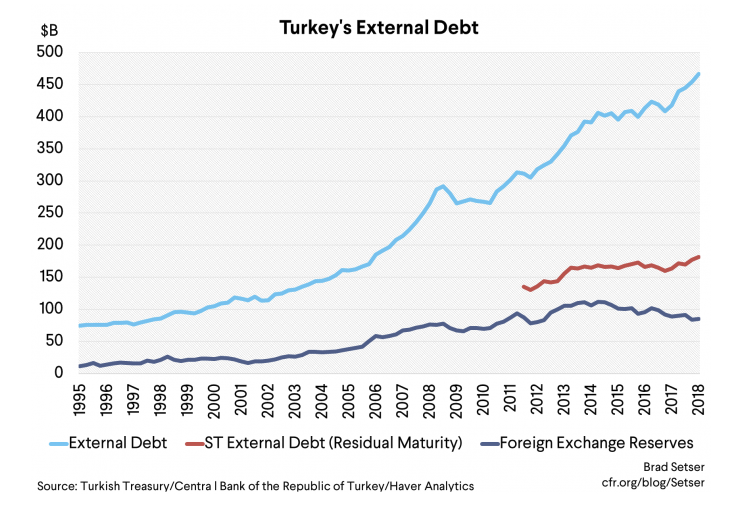

Bigger Crisis Possible

But in aggregate the banks own holdings of FX and the CBRT’s reserves fall well short of covering the banking system’s short-term FX funding base. the raw material for an even bigger crisis is there. pic.twitter.com/wTRQyXcp57

— Brad Setser (@Brad_Setser) August 20, 2018

Rapid Loan Growth

What makes Turkey unique and interesting, from a balance sheet point of view, is the recent ability of Turkey’s banks to use fx funding to support rapid TRY loan growth. That is what makes Turkey a bit different from the 1997-98 Asian crisis cases.

— Brad Setser (@Brad_Setser) August 20, 2018

Questions Abound

Turkey’s banks account for almost 1/2 of Turkey’s external debt, and about 2/3rds of Turkey’s maturing STD.

But it isn’t immediately clear why the banks needed so much external fx funding: their domestic fx deposit base is big & covers their (large) domestic fx lending … pic.twitter.com/c1cs1euzun

— Brad Setser (@Brad_Setser) August 20, 2018

Setser commented “I find the balance sheet of Turkey’s banks fascinating.”

Framing Turkey’s Vulnerabilities

Brad Setser frames Turkey’s Vulnerabilities: Some Rhyme with the Asian Crisis, but Not a Repeat

>There are a number of different ways of framing the cause of Turkey’s recent currency crisis.

>I think the emphasis should be on Turkey’s banks, and their large stock of external debt. The banks are the main reason why Turkey’s currency crisis could morph into a funding crisis, one that leaves Turkey without sufficient reserves to avoid a major default.

>While Asia offers the best parallels, the analogy to Asia is also just a bit off. Turkey has, rather miraculously, been able to use external foreign currency funding to support a domestic boom in lira lending to households… something Asian banks never did, to my knowledge.

>The financial mystery in some sense isn’t how the banks’ lent foreign currency to domestic firms, it is how they used their external foreign currency borrowing to support domestic lira lending.

>Turkey’s banks do hold a decent amount of regulatory capital. And they hold that capital in lira. Fair enough. A lot of folks think U.S. and European banks would be a lot healthier if they funded their lending with one dollar (or euro) of equity and six dollars (or euros) of deposits rather than funding their lending with a dollar of equity and close to twenty dollars of borrowed money. Equity isn’t “set aside” per se, it is invested alongside other sources of funding.

>But by holding all of their equity in lira even though a large part of their funding and lending was in dollars, the banking system’s capital ratio falls as the lira falls

>Turkey’s banks borrowed foreign currency in part to have dollars to swap into lira in the cross-currency swap market. A borrowed dollar or euro swapped into lira is effectively lira funding, not dollar funding—it just shows up as foreign currency borrowing in the external debt data. As far as financial alchemy goes, cross-currency swaps are pretty plain-vanilla.

>It was also the fact that the swaps generally had a shorter-maturity than the underlying foreign currency borrowing. Five year bonds were issued to raise dollars. But then the dollars were swapped for lira on a 3 month contract.

>The result is that Turkey’s banks have a maturity mismatch on their lira book. They will start taking losses quickly if domestic interest rates rise too high, as they have longer-dated lira loans and shorter-dated lira funding.

>The banks also had the option of meeting their reserve requirement in gold. As a result, Turkey found a way to make gold deposits effectively available to support household lending (by letting the gold substitute for other forms of required reserves).

>The net effect is that the banks have an extremely interesting—but rather complicated—foreign currency balance sheet, with an unusual mix of vulnerabilities.

>So what’s my bottom line?

>Simple—from a balance sheet point of view, the risk of a run on the banks’ foreign currency funding poses far larger vulnerabilities than the government’s funding need. The government, excluding the state banks, has almost $100 billion in external debt, but less than $10 billion coming due in the next year. The banks have just over $150 billion in external debt, but over $100 billion coming due over the next year.

>The rise in Turkey external debt in 2017—which corresponded to a rise in Turkey’s current account deficit—now looks to be the straw that broke the camel’s back.

Bears Have It

There is much more in Setser’s post. For those interest in FX, It’s worth a read in entirety.

Setser concludes, and I agree, “I would bet that the dynamics in Turkey get worse before they get better—in most crises, creditors want to reduce their exposure, not just stop adding to it. The underlying risk of a severe crisis, one marked by systemic defaults not just an epic depreciation, remains.”

The bears have the far bigger case with liquidity issues, Trump sanctions, and timing considerations.

Old Story, New Complicated Method

The story is an old one “complicated borrow short and lend long derivations eventually blow up, especially with foreign financing.”

On July 10, I commented Spotlight Turkey: Hyperinflation and Mass-Migration Crisis Inevitable.

On July 14, I commented Hyperinflation Avoidance Advice for Turkish Citizens as Fitch Cuts Ratings.

On July 10, the Lira closed at 4.876. It is now 6.080. That a whopping 20% decline in just over a month, but it’s nowhere near hyperinflation material.

Hyperinflation is a political event, not a monetary one, and Erdogan is on that path.

The primary bull case is not the one Robin Brooks suggested. Rather, it is a potential for a huge Lira rally if Turkey heeds Trump’s demand and unconditionally releases US Christian pastor Andrew Brunson, absurdly held by Turkey on charges of terrorism.

Mike “Mish” Shedlock

It is ALWAYS a stupid idea to take currency loans because they have a lower interest rate but lots of Turkish businesses still took currency loans and Turkish banks gave them so since the Turkish Lira crashed the companies have trouble even managing never mind repaying those currency loans and as a consequence Turkish banks are also in deep trouble because they have currency loans themselves coming due backed by currency loans to Turkish companies that have trouble paying those loans.

Unique Turkish twist seems to be that the banks themselves also thought they would be clever and they borrowed in foreign currency like US dollar and then converted those dollars to Turkish Lira and then borrowed to Turkish consumers in Lira thereby trying to get a good spread and lots of profits based on the difference between LOW dollar funding interest rates and higher Turkish Lira loan interest rates.

.

I would say Turkish companies that have currency loans are fcked and Turkish banks are super-fcked but Turkish consumers might be OK if they did NOT have currency loans.

.

ONLY borrow in your own currency is the lesson here.

Congratulations on calling it a couple months ago. However, Turkey is part of the EU, so will they be saved by Central Banks like Italy, Greece, and Spain before them, or be allowed to rot like Venezuela?

Turkey isn’t part of the EU. Never was. They applied a generation or two ago, but despite American pressure to get them in, for cold war type reasons; France and Germany have never been comfortable with not being the unconditional Big Dogs. So they managed to put Turkish entry on hold, all the way up until Turkish internals got tricky enough that even America is no longer pushing for membership.

Turkey is NOT part of EU.

Due to exposure Turkey will be bailed out by EUssr, if Trukey falls EU falls