Emergency Funding Continues

The Fed continued emergency repos today as firms are short of cash.

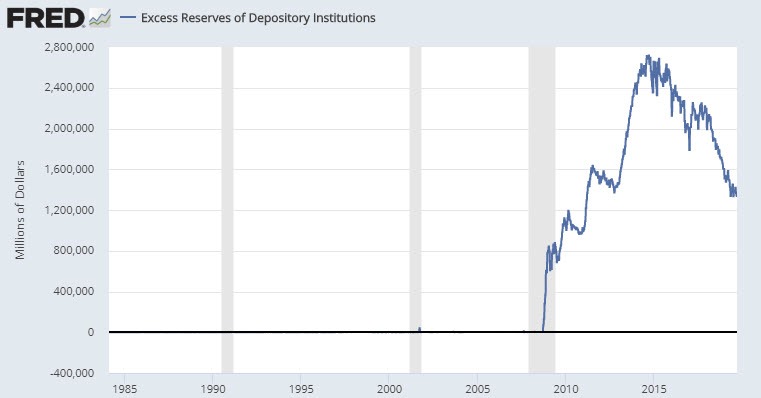

2/ Total reserves and excess reserves as a fraction of total bank assets. Compare these to pre-crisis history. To imagine that recent repo spikes reflect some inadequacy of reserves or the need for more QE is to misunderstand the nature of the constraint. pic.twitter.com/KsxsUPusgb

— John P. Hussman, Ph.D. (@hussmanjp) September 20, 2019

Fed Tackles End-of-Quarter Funding Angst by Extending Repo Plan

Bloomberg reports Fed Tackles End-of-Quarter Funding Angst by Extending Repo Plan

The New York Fed said it will conduct overnight repurchase agreement operations daily Monday through Friday until Oct. 10. The Sept. 23 operation will be for as much as $75 billion, while the actions thereafter will be for at least that amount. Separately, it will also conduct three 14-day term operations for an aggregate amount of at least $30 billion on Sept. 24, Sept. 26 and sept. 27, according to a statement.

“The Fed just reminded the market that they have complete control over the front-end if and when they want it,” said BMO Capital Markets strategist Jon Hill. “Given the volatility we saw this week, they want to ensure quarter-end goes as smoothly as possible.”

Complete Control?

That the Fed has to do these operations is a guaranteed sign that things are not under control.

Bad Optics

The NY Fed pumped another $75 billion into the system on Wednesday and then again on Thursday. “It’s very bad optics to have to come in with emergency anything day in and day out,” said Danielle DiMartino Booth, CEO of Quill Intelligence

@QuillIntel —https://t.co/J37xyHdyS9— Danielle DiMartino Booth (@DiMartinoBooth) September 20, 2019

“It’s very bad optics to have to come in with emergency anything day in and day out,” said Danielle DiMartino Booth, CEO of Quill Intelligence.

Understanding the Issue

So the banks are calling for the Fed to add permanent reserves to solve the funding pressures. How about if the banks stop buybacks and sell some shares back to the market and raise capital.

— Michael Lebowitz, CFA (@michaellebowitz) September 20, 2019

Overnight Lending?

We are clearly not talking about “overnight lending”.

A crisis has been going on for days.

Beneath the crisis is my observation that companies are using overnight repos, continually, to fund normal operations. Parties no longer trust the collateral.

It took a mid-month crisis to flush this out.

The Fed’s alleged solution is to give companies at least $30 billion “14-day” lending, repeated of course, indefinitely. This is on top of at least $75 billion daily.

Excess Leverage

I smell an excess leverage, borrow-short, lend-long scheme of some sort that has seriously gone awry.

Anyone else come to that conclusion?

Mike “Mish” Shedlock

The funny thing to me is that this article talks about ‘bad optics’. To me the real problem isnt that someone is in trouble, but that the system is now exposed as rigged because we can clearly see that some people inside the system know that someone is in big trouble and know who they are, but the rest of us dont have that knowledge. This asymmetry of knowledge impoverishes those who dont know and enriches those who do. If the Fed could take one action to help things, it would be to tell us exactly what is going on.

As for Mish’s guess as to what it is, well it sounds about right. What Mish wont say, because use doesnt know, is who it is. Someone is desperate to keep the plates spinning for some reason. It must be a pretty amazing reason because if you have to borrow at 10% then you can be pretty sure that you have lost at that point and you need to come clean and wind yourself down. The Fed will know who this is, and the fact that they are lending to this bust entity rather than closing it down must mean it is a big player than they dont want to fail.

Try negative yielding bonds!

Maybe banks would have more cash if they didn’t:

NEW YORK (AP) — The nation’s largest banks are rewarding shareholders by spending tens of billions raising their dividends and buying back stock after getting the green light from the Federal Reserve.

Oops

usnews link won’t go thru. From June.

They’re not out of cash, they just don’t want to use it to buy securities/Treasuries from some parties despite attrative interest rates.

They are not buying anything.

EFFR is unsecured lending of cash overnight to banking brethren.

Well yes, but the question is why they aren’t using the cash that some are saying they don’t have to swap for securities in the repo market at rather attractive interest rates. EFFR is something entirely different, although related.

If you want perspective on this issue, go to the guy who is a foremost banking -finance industry analyst and worker therein – R. Chris Whalen. This is his take on the subject issue: link to theinstitutionalriskanalyst.com

As he says, the problem is an “LCR” (Liquidity Coverage Ratio) regulatory issue, passed following the “Great Recession.”

“the problem is an “LCR” (Liquidity Coverage Ratio) regulatory issue,”

…

What a hoot. LCR as “the problem”.

LCR is a firewall between taxpayer’s wallet and bank bailouts in the INEVITABLE next crisis. A higher LCR (bad per Whalen) means banks have to sit on more liquidity. The horror. Yes by all means lets lower reserve ratio so banks can lend even more now … and get into trouble quicker and deeper.

Whalen is a creature of Wall Street. Worked for NYFRB and Bear Stearns. I wouldn’t trust his word on anything.

Interesting that he failed to mention the rework of FASB157 … March 2009 Wall Street got Congress to strong arm FASB move from mark to market to mark to model on assets sitting on big banks balance sheet.

When the move happened that is when – almost to the day – stock market started its relentless march upwards.

Now, at the end of cycle, players are not certain of other players’ balance sheets. Individual banks (and their regulators) only know the TRUE situation of their balance sheet.

Works great on the way up … on the way down? Exacerbates the problem.

That article was actually written by Brian Wesbury who has never seen a problem in the markets or economy in his entire life..or at least since he has worked as “Chief Economist” at First Trust. He sat on TV with a smug smile back in 2007-2008 saying there were no issues at all with the housing and mortage markets.

There’s still Tr$1.35 of cash among the banks. LCR does not hamper lending or leverage ratios, it just constrains the banks balance sheet composition so they are not stuck with stuff that cannot be sold prompto if push comes to shove. It may affect their earnings, but not their leverage.

And the problems is not that the banks are lending too much: the problem is that they are not lending enough, there is little demand from people who are in a position to borrow (responsibly). The screaming demand is all on the side of the people that want to swap savings for fixed income in the future, hence the negative interest rates and the sky-high bond prices.

@ Brutus’ Admirer

The explanation explains nothing. The idea that a lot of the liquidity comes from Arab cash that is distracted by the latest ??? operation is ludicrous — as if this isn’t delegated to money managers who are paid to go to work.

As for the fact that TED and LIBOR are not spreading, LIBOR only measures interBank lending. What if the thirsty partners are non-Bank financial entities? What if it’s parties that don’t have access to the discount windows?

SOFR rates (the designated replacement for LIBOR) ARE elevated.

Tax payments and increased bond issuance as a cause seems a non-starter to me, as long as there’s Tr$1.35 in excess reserves. The main volume in Repo are treasuries, so it’s not distrust of the collateral, unless the shortage is entirely limited to the non-treasury securities, which nobody is reporting.

I’m going with Country Bob’s hypothesis.

Actually your post doesn’t really explain anything. How do you define ‘reserves”? Do you really believe the Fed has that much cash on hand? Please do a little more research and get back to me. You remind me of Trump bragging about all these new jobs when in reality these so called jobs are nothing more.

See if Soros’ or any of the major currency speculators and their funds has made any recent money shorting the dollar. That will tell you lots about why the Fed is panicking. And they are. And if a war is brewing with Iran no doubt some OPEC nations will want to redeem their dollars into something else…like gold. This could be the beginning of a flight from dollars into whatever. If it is the U.S. is screwed.

The quickest and safest way to resolve this distrust is to convert corporate bonds to shares and dilute the shares until remaining private debt becomes manageable. Additionally, banks would have to raise capital in the equity markets.

There is no mystery here, and all the stories about a USD shortage are bull sh!t.

As I wrote yesterday, no one is going to lend money to an entity that won’t (or probably won’t) be able to pay it back tomorrow.

It doesn’t matter if you hypothecate Treasuries as collateral, because (1) the checks to make sure one bond isn’t hypothecated multiple times has broken down; (2) even if you have a claim against a Treasury bond, there is good reason to think a pompous bankruptcy judge (or corrupt Obama appointee) will simply ignore centuries of precedent and protect their political cronies.

Even if repo collateral is held at the FRBNY, if foreclosing on that collateral will send a major bank into Lehman Bros arms, the Fed might intervene and ignore the law. See LTCM, Bear Stearns, etc for examples where the Fed ignored the law.

When the politically connected don’t even pretend to obey the law (see Comey and Brennan and McCabe and …) people quite reasonably assume the law is a joke and only enforced on those without political connections.

Now excuse me… I’m going to smoke a joint, curse and stick my middle finger up at the SEC — and see if I get the same treatment as Elon Musk

” people quite reasonably assume the law is a joke….”

Now, wouldn’t that be great!

Lawlessness works great in…. give me a minute, I’m trying to think of a place where lawlessness works. Must be an example somewhere….

Comey and Brennan are going to have to go to prison, or else the federal political system will collapse. I would think the smarter bureaucurats would arrest Comey/Brennan out of their own self interest.

All the federal agencies (and courts) that have taken upon themselves to write new laws in pencil and modify them whenever it suits them are going to find that what goes around comes around. That is not a comment about the breakdown of ethics, its thousands of years of human history. Live by the sword, die by the sword is a thousand years old. Modern version: use state authority to steal from others, expect others to steal from you.

“Lawlessness works great in…. give me a minute, I’m trying to think of a place where lawlessness works. Must be an example somewhere….”

Ditto “law”-abidingness, when “law” is simply newspeak for what Ayatollah Something-or-other dreamt about last night, or what a bunch of lobbyists figured they can get a totalitarian Junta to agree to for cheap.

You’ll get no argument from me that “Rule of Law” is not superior to either above. As long as “Law” refers to something even remotely resembling valid law. But when, otoh, what is passed of as “The Law” is literally, no exception, just a 100%, obvious, full on joke; people recognizing it for what it is, beats people continuing remaining delusional forever.

To be blunt with you Bob you can make that argument about most countries. Many countries are bankrupt and survive because of faith. The belief that somehow they will get their money back. The belief that somehow their paper assets such as stock will someday actually be worth something. When people lose trust and decide it is time to head for the exit and redeem their paper assets for cash or gold is when the system really breaks down. The very recent attack on the Saudi oil fields and now this unexplained need for more liquidity by the Federal Reserve is not a coincidence, in my opinion. You just don’t understand how much money the Arabs have invested in our economy and what will happen when they decide to get out of dollars. It is ROLLOVER 2019 and 2020. Watch the movie. I may be wrong but I doubt it.. Enjoy you joint Bob.

To be blunt with you@[Ted R] , I know that black on black violence dominates the ghettos from which Obama came. They rob and rape each other all the time. Look where it gets them. I know that third world banana republics rob and rape each other all the time also — and look where it gets them. I know there is no Saudi economy. It was God / Allah / mother nature / dinosaurs vs meteors that made the crude oil deposits. The humans in Saudi Arabia had nothing to do with it. Saudi Arabia’s so-called economy is the Bin Laden family hiring a bunch of ex-pat Pakistani workers to pour concrete and build various structures. That’s hardly an economy.

Africa has plenty of natural resources — the Chinese are there exploiting them right now. European colonialists exploited the resources a century ago. US corporations do it on a corporate scale, not national…. but guess who doesn’t exploit the natural resources? Yeah, the ghetto thugs / third world Africans.

You can take Britney out of the trailer park, but you can’t take the trailer park out of Britney…. And you can take Obama out of the ghetto, but clearly the ghetto never came out of Obama.

There are places where the law is enforced more or less — and the USA used to be one of those places. Its not a coincidence that economic growth is MUCH higher in places with laws, and much lower in places where there isn’t.

I do not accept Obama’s ghetto thinking. I don’t care if he goes back to the ghetto or back to whatever third world sh!t hole his daddy came from — just so long as he and his lifestyle go.

The Fed can’t fix ghetto thinking by ignoring basic banking laws, which is why Bernanke’s FOMC failed. Its not a coincidence that when Powelll restarted ZIRP/QE (aka robbing the savers to pay the bankrupt), the repo problems began. The markets expected (demanded?) a return to normalcy from Powell, not black on black violence

Could be related to anything.

China, Iran, something in the EU, Saudi Arabia, Fannie Mae, Mortgage lending, or even the GM strike.

The Fed sure won’t disclose. Is the Fed so clueless they don’t really know?

Minsky moment, anyone?

So who is needing the excess cash? My guess is that it’s not needed for “normal banking”. Maybe for the trading arms, hedge funds? If they need the cash and no one wants to lend it, I would guess the collateral isn’t great.

Banks (those not in the trading or brokerage business) have excess reserves.

I think there is plenty of cash in the system.

Fed should make those that need overnight funding raise capital.

No. More likely to be the usual suspects: hedge funds like Renascence Capital, George Soros, and overseas fast money artists. They have uncovered a way to profit from causing this kind of turmoil in short term liquidity markets.

“Maybe repo rates are going up because nobody trusts anyone’s collateral that isn’t treasury”

Correct observation

It seems to me that corporations are bleeding investors and government/public with worthless corporate debt just like financial institutions bled investors and the government/public with worthless mortgage backed securities. Corporate executives and hedge fund managers/inside traders pocket trillions from leveraged buy-backs that inflate their holdings and then cash in before the shit hits the fan. (See your recent article on rise in CEO retirements.)

As with the housing crash, the instigators stuff their ill gotten wealth into DFIs, and fraudulent shell companies where they can’t be traced. I suspect that why we never saw the predicted inflation after the feds pumped trillions into TARP, buy-backs and QE. That money was already gone. Now the wealthy leaders of industry and finance have nearly run through all the leverage their over-stressed balance sheets can justify. I think we’re in an artificially extended market as with the last year of the housing market when the players were cooking the books to make it look like all was well as the syphoned off the last easy money.

“Not a collateral issue. Lack of cash issue.”

Both really but lack of cash is a collateral issue. There is $1.4 trillion in excess reserves, banks would lend that if they can get more than interest paid on excess reserves. Yet the overnight rate shot to 10%.

That means no one trusted the collateral offered leaving someone short of cash.

Not sure I agree with this. Unsecured lending. Now, if you’re worried counter party might blow up overnight. OK.

I think it reveals lack of cash of borrower AND lender.

Anyways, firms could always hit the Discount Window (at higher rate) … THIS is when firms get hit with stigma … other players know someone hitting the DW is last resort … and to steer clear.

Maybe splitting hairs.

If you said “worried about counter party’s balance sheet”. OK.

Still think more of lack of cash in the system problem.

Apart from the issue of a catalyst causing a cash deficit, isn’t the declining level of reserves “available” to banks really more like 800B rather than 1.4T, when you take out the reserves in foreign banks in US?

“It makes you think of the definition of excess reserves. These were created as a result of QE, i.e. FED buying toxic securities at face value, and replacing expired ones with re-inflated securities. “

Not quite – The Fed pretty much bought Treasuries and Agencies not garbage (unlike the EU)

What banks did with the cash is another matter. The bottom line on bank-to-bank lending is there is no trust in bank balance sheet collateral as opposed to the Fed sitting on bad collateral.

You’re right, that was TARP. QE was treasuries and agency MBS.

Not a collateral issue.

Lack of cash issue.

“The federal funds market consists of domestic unsecured borrowings in U.S. dollars by depository institutions from other depository institutions and certain other entities, primarily government-sponsored enterprises.”

The question is why lenders lack cash? The bump in rates excuses – treasury issuance and corporate tax deadline were known weeks ago. Powell acknowledged these excuses, but FR caught flat footed by demand.

Someone(s) needs cash BAD.

Agree that is also part of the issue. Most banks are not sitting on large piles of excess Reserves at the Fed.

“Someone(s) needs cash BAD.”

While others, who were prior willing to spot the needy a buck overnight, are increasingly concerned about being the last to recognize the music has stopped; and that all chairs are taken.

Thieves may not, as a rule, be the sharpest tools in the shed; but they tend to have a reasonably good nose for signs that the guy they’re robbing is about to wake up and call the cops. Or rack the slide.

And to paraphrase the old bear country saying: It’s not so important to get out ahead of the cops; as it is to get out ahead of enough others, that those behind you can reasonably be expected to occupy the pitchfork wielders while you clamor to safety.

For all those people calling for and end to the federal reserve, how would this be handled w/o their help? This is what the fed was originally created for. The other mandates should be eliminated.

If I could print money willy-nilly whenever I felt like it, I could “help” too!!!! So could anyone else. The problem isn’t The Fed being able to print Washington’s head on paper. It’s rather than not everyone else can do so equally. Privilege is what destroys all possibility of civilization.

More practically pressing for the “situation” at hand: What “problem”? Why is “this” a “problem” again? If some candyshop, bank or lemonade stand can’t borrow overnight at 1%, they’ll have to offer 10. Or 100. Or close up shop and free up the resources they are hogging for someone hopefully more competent. At some price, qualified lenders and borrowers meet. Problem solved. No half literates with printing presses, out to distort perfectly naturally occurring economic equilibria, required. Nor desired.

I disagree with your point

With so much European and Japanese sovereign debt now yielding less than zero, it was only a matter of time until the repo market began to seize up. Negative-yielding debt is unfit to serve as repo collateral or as Central Bank monetary reserves.

Spot on

It makes you think of the definition of excess reserves. These were created as a result of QE, i.e. FED buying toxic securities at face value, and replacing expired ones with re-inflated securities. Was there a contract to buy these securities back in reversed repos?

Isn’t the primary dealer system supposed to minimize the risk of this ever happening, especially on multiple, consecutive days?

Could it be that various parties worldwide have finally bought down Treasuries’ yields to where primary dealers are acting like exchange “liquidity providers” and disappearing in a flash when algos run against them? I.e., quietly no-bidding and looking for better deals for their cash?

I’m with you. Everything is leveraged to the hilt. I don’t fully understand how this happened, but ever worse, I don’t see a way out of this upside-down reality.