Albert Edwards at Society General, via email, notes the Renminbi had its worst month on record.

Edwards also says, let’s put things into perspective.

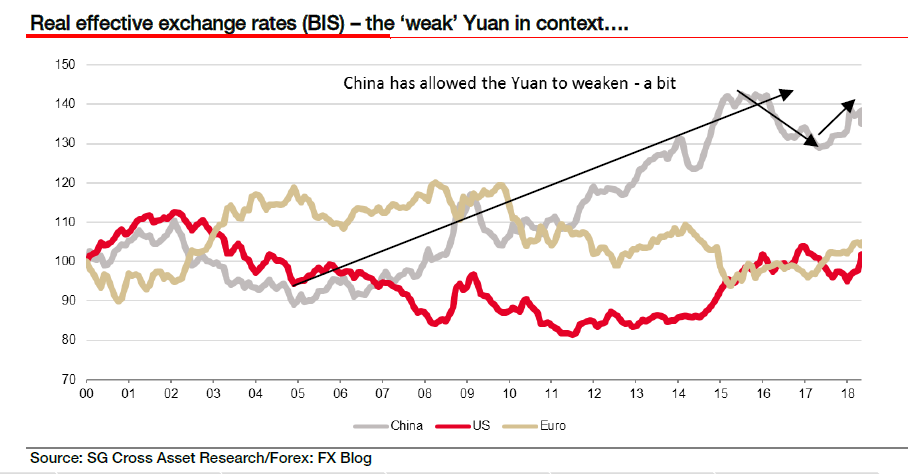

No Trend Yet?

Clearly the fear is that the Chinese authorities are using the weak renminbi as a stick to beat the US with over the trade war, but let’s put things into perspective. To quote Kit Juckes on the war of words over the yuan: “the chart shows its trend in real effective terms over the last 18 years. The 2015/16 policy of letting it weaken has been abandoned and the recent fall should be seen within the context of the bounce in real trade-weighted terms that we saw in recent months. It’s not clear that we will have a trend from here.” Not yet anyway!

I am more inclined to agree with Edward’s opening comment.

Despite the reassuring words from the PBoC, it is difficult to see how, if Chinese interest rates are being slashed, the renminbi can do anything other than fall sharply.

This all depends on how the trade war escalates. And there is no indication Trump is ready or willing to call it off.

On the other hand, US dollar sentiment is lopsidedly bullish. Sentiment is not a timing mechanism, but it does provide headwinds.

Japanese Labor Shortage

Shortages in the Japanese labor market mean that a record 98% of this year’s graduates and high school leavers have found jobs!

Capital Spending Plans

Our Japanese economist Takuji Aida notes that the Q2 Tankan report shows not only a very robust labour market, but it now appears these shortages are resulting in a rapid acceleration in capital spending. Plans for FY18 has been revised up to +13.6%, from +2.3% in the Q1 survey (see above chart) and core machinery orders for April grew by 10.1% mom (and 9.6% yoy), marking a significant pick-up in the new fiscal year.

Unlike in the US, all this is happening without the help of large tax cuts and repatriated foreign earnings. Japan is enjoying what ostensibly appears to be a healthy, balanced recovery – albeit with the very large caveat that it is dependent on the most ludicrous QE ever seen in a modern economy.

Sustainable?

The question at hand is whether or not this is sustainable. Japan is not only dependent on massive QE, but growth in the rest of the world, at least outside the US, is slowing.

Ultimately, Japan will reverse when its demographics reverse.

Mike “Mish” Shedlock

“Ultimately, Japan will reverse when its demographics reverse. ” –

Could you explain what this means. I honestly don’t understand. Thank you.