by Mish

When it didn’t, Bloomberg promptly noted that a rebound in inventory build-up will add to third quarter GDP.

It won’t, because inventory-to-sales numbers remain in the stratosphere. This is something I have commented on for months. Last week, someone else noticed.

As Good As It Gets?

Joseph Calhoun, at Alhambra Investment partners took a look at inventory and other factors and asked is this As Good As It Gets?

The last two years we have seen a pattern of a weak first quarter – for which economists have been searching frantically for an explanation – followed by a second and third quarter rebound. Fourth quarters have tended to the weak side. This cycle was a kind of mini inventory cycle within the larger business cycle. Businesses, told by the Fed and Wall Street economists – possibly redundant – to expect the ever elusive economic acceleration to finally arrive, built inventories in anticipation of what never came. It appears now that US businesses may have finally reached their limit of credulity when it comes to Fed forecasting.

There was no inventory build in the second quarter; indeed inventory subtracted 1.2% from GDP in the quarter. As did almost every other investment category; intellectual property was the lone exception. That isn’t exactly comforting when one considers the nebulous nature of that category. The press almost universally reported the inventory GDP subtraction in positive terms, i.e. inventory contractions are followed by expansions of production to build them again. That is, I believe, the triumph of robotic article generation, algorithms copying what has been said in past articles, ignoring the context. It is often true that inventory contractions are followed by increases in production – but not when inventory/sales ratios remain elevated even after a contraction. And slowing of inventory accumulation has not yet reduced those ratios to levels associated with recovery and certainly not enough to warrant an increase in production.

And while everyone concentrated on the inventory numbers, the more important investment categories were mostly ignored. Gross private domestic investment contracted 9.7% from the first quarter which wasn’t exactly gangbusters either. Year over year GPDI is now down 2.5% a number not seen outside recession since the second quarter of 1967. In other words, it’s pretty darn rare. Even residential investment was down in the quarter – by a not insignificant 6.1%. Maybe last week’s new home sales report was good news – up 25% year over year – but starts and permits are down year over year and Case Shiller says prices have stopped rising. Last week’s durable goods report certainly didn’t offer any rays of sunshine for the goods side of the economy; that report was bad from top to bottom, overall down 6.4% year over year.

The US economy is not in recession – yet – but it is surely slouching slowly in that direction. The drop in investment is very concerning since it is investment that leads; consumption is a consequence of growth not a driver of it. From 2012 to 2015 the economy grew at a 2.2% pace. With this quarterly release and downward revisions to Q4 2015 and Q1 2016, we now have 3 consecutive quarters of 1% growth. And I don’t expect it to get better in the third quarter either. We have an election in November and with none of the above winning in a landslide right now I would not expect a surge in corporate investment. I have never bought into the secular stagnation theory but for now, this may be as good as it gets.

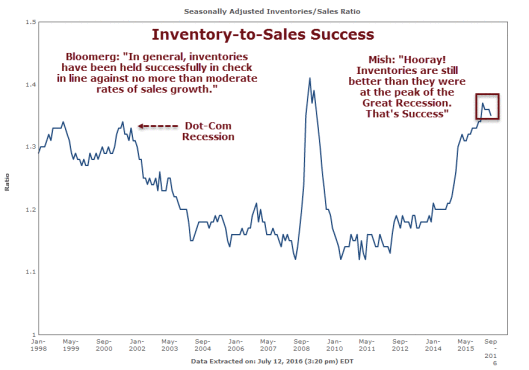

Inventory-to-Sales

Unless sales pick up, and perhaps even if sales pick up, there will be no inventory build.

On July 12, I noted Inventory-to-Sales Ratios Extremely Elevated. Here are some charts.

Motor Vehicles Inventory-to-Sales Ratio

Durable Goods Inventory-to-Sales Ratio

Apparel Inventory-to-Sales Ratio

What’s Behind the Inventory Crisis of 2016?

Kiss the idea goodbye that inventories need to be replenished. But why are they so high in the first place?

Please consider What’s Behind the Inventory Crisis of 2016?

The last time the inventory-to-sales ratio was this high was 2009, when we were in the throes of the Great Recession – people lost jobs, businesses closed, nobody was spending, nobody was growing.

What does it mean that inventory levels are this high in 2016? Are consumers not spending? Are we headed for another recession? Or are other forces at work?

One major culprit is the way consumers shop. Their expectations have changed. This is the age of Amazon Prime, Instacart, Uber and Lyft. Free shipping. In-store pick-up. 1-hour delivery. Easy exchanges and returns. Above all – convenience. If it isn’t convenient for a customer to buy something they want, they won’t buy it – or they’ll buy it somewhere else. Fulfillment has usurped the throne of customer satisfaction.

One common tactic has been to keep buffer inventory on hand. Out-of-stock inventory kills customer loyalty. Not being able to fulfill quickly kills customer loyalty. But having lots of inventory doesn’t equate to efficient fulfillment.

The Business Model

J.C.Penney recently announced its plan to test out a new business model with its supplier, Ashley Furniture. J.C.Penney won’t carry any Ashley Furniture inventory in stores or in its distribution centers. Instead, it’ll just hold floor samples and when customers choose to purchase an item, it will ship direct to consumer from Ashley Furniture. If successful, J.C.Penney hopes to extend this showroom strategy to other departments like appliances.

Execution

Wal-Mart Stores, Inc. recently announced that it is employing drones to manage its inventory. The drones would move through a distribution center, capture images, and flag misplaced items. The process would allow Wal-Mart to check inventory in a day, instead of in a month when it’s done manually. For Wal-Mart, using technology to enhance visibility is a big part of getting a handle on inventory.

Inventory Management by Drones

It’s unrealistic to blame the entire inventory buildup on Amazon and online shopping. We also have a saturation of stores, all duplicating inventory.

Drones can help manage inventory and so can a change in the business model such as J.C. Penny hopes to do with furniture. Both point to a drawdown in inventory, not an inventory revamping as has been widely touted in mainstream media.

If consumer spending falters, the inventory-to-sales ratio will stay elevated on top of it all.

Third quarter GDP is likely to be another disappointment.

Mike “Mish” Shedlock