The Fred Blog asks Who Absorbs the Price Jumps in Raw Materials?

The PPI measures how much producers charge for their products, while the CPI measures how much households pay for those products.

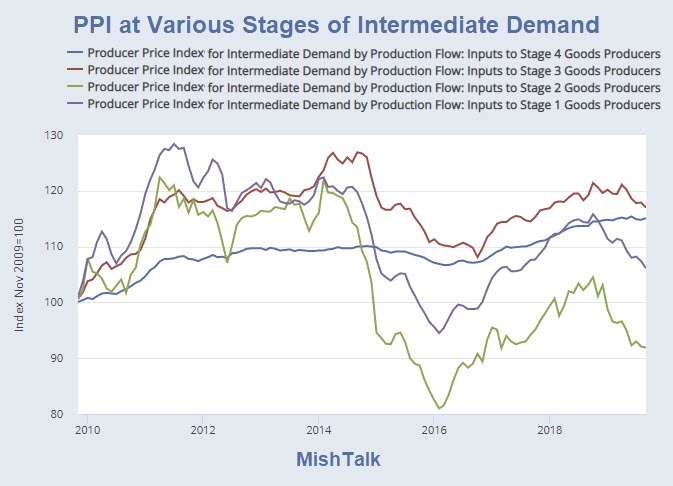

The PPI data above are organized in four distinct stages along the production process, from raw materials to final product. What’s striking in the graph is that we can clearly see fluctuations in the cost of raw materials for stages 1, 2, and 3 but not for stage 4. Stage 4 is quite steady. According to the Bureau of Labor Statistics, industries assigned to stage 4 primarily produce output that is consumed as “final demand,” which may have obstacles the other three stages don’t have. For whatever reason, the producers at this stage absorb the price fluctuations of inputs—which is something in economics we call “limited pass-through.” A similar mechanism occurs when fluctuations in exchange rates or import tariffs affect foreign goods: Not all input price changes are reflected in retail price changes for those goods.

Some goods and services consumed by “final demand” businesses at stage 4 are motor vehicle parts, commercial electric power, plastic construction products, biological products, beef and veal, engineering services, machinery and equipment wholesaling, long distance motor carrying, and legal services.

The BLS describes the first three stages as follows: Industries assigned to stage 3 primarily produce output consumed by stage 4 industries; industries assigned to stage 2 primarily produce output consumed by stage 3 industries; and industries assigned to stage 1 produce output primarily consumed by stage 2 industries.

Customize the Graph

Here’s a link to Customize the Graph

I wanted to see the relationship between PPI stages and CPI but the scales were so strikingly different that the resultant graph looked nonsensical.

Mike “Mish” Shedlock

Both the direct and indirect labor content of these categories has been sliding as a percent of total product cost for decades now. There was simply no other way to move five hundred million Chinese peasant workers into the global manufacturing workforce without this happening. Even Krugman has recently discovered this, and it’s knock-on effect, imho, of electing a populist, isolationist president due to governments utter bungling of massive, ongoing retraining domestically.

Not just retraining, the initial training also needs to be kicked up a few stairs if Americans want to be competitive with other countries.

How about the individual being responsible for their own education and skills upgrade. What happened before big govt tried to fix everything. Globalization has resulted in creative destruction and economic theory purports that those who lose their jobs will evolve into better jobs by being forced to upgrade their skill levels. This has happened throughout history, eg mass production of autos putting buggy makers out of business etc. Just because students and or their parents make poor choices on what college degrees they get doesn’t mean anyone other than themselves should be responsible. Govt trying to “help” with college via unlimited student loans have resulted in severe education inflation. The govt has achieved for college students what they achieved in the housing bubble. Private enterprise is probably the best conduit for attracting and creating high skilled jobs.

I’ve seen enough now to be convinced that Realist is right in that we are living in the best times in human history…by far. Eighteenth century European royalty could not have imagined the world in which even the homeless in Los Angeles routinely move today. A short, brutish life of disease, starvation and death has been the rule for most of human history. NEVERTHELESS, it pisses me off to see the obvious, cosmic scale squandering of opportunity in our time.

I’m even beginning to think I have the answer to the Fermi Paradox: Trade wars.

How much training does working the cash register at Walmart require? Will Walmart pay you more if you have more training? I think there are deeper issues here.

The problem is there is too much stock put into “lack of skills”. It is a farce when you see high skilled talent being laid off for bonded labor work visas for over 30 years. This is now reversing as I’ve witnessed cases every week of work visas now needing to be justified and cancelled until proven otherwise. Of course the baby will get thrown out with the bathwater once Trump is evicted from office. The government should intercede when a citizen loses their job to a non citizen. Stories from the department of labor are now heard by Ken Cuccinelli of citizens directly affected by work visas.

The real problem is still wages to the masses are flat relative to prices of all things . It turns out more labor availability leads to slow wages for all and stagnant lives for all except the upper crust.

I have to agree with you on this. Looking at Mish’s other topics, it appears Americans -and the rest of the plebs worldwide- are stretched too thin already, highly indebted and the wages are just way behind. So far behind, they struggle to keep up with the explosion of assetprices and cost of living. But no worries, the FED came to the rescue by pumping 100 billion a day into the accounts of all people and therefor there is absolutely no slowdown or any reason to be concerned about the bubblification of everything!

The 100 billion a day comes from somewhere. That somewhere is FROM the accounts of 99% of the people. TO the accounts of 1%. Hence the struggles you refer to.

My comment was dripping with irony, of course.

But yeah, it’s one gigantic, vampiric and maniacal circus and us normal folks are paying for their gambling. I’m just a keyboard warrior and obviously no expert, but even I recognize, the social contract has been broken, perhaps because the Bretton Woods system collapsed and in its place, rampant& crony, unregulated capitalism took its place. And now, with the world on fire and with the insanity of negative interestrates, instead of this bullshit left vs right division, we should be aiming to build something that works and is sustainable. Because obviously, this isn’t working anymore.

Not more labor availability. Less capital availability.

The money required to allow idle upper crusties to consume as if they were doing something useful, has to come from somewhere. That somewhere is the capital which would otherwise be available to make labor efficient enough to justify more decent wages.

You can’t have both. EITHER resources are spent on overpriced remodeling and shoes for idle idiots, OR it’s available for productive uses.

Prices of stuff sold retail is much harder to gauge. Stuff that doesn’t sell for list price (trends have a huge effect on marketability) goes to second tier stores, then is sold in bulk to outfits that find other outlets, discount stores, etc. A pair of slacks might start out at 140 and drop to 14 2½ years later. This is impossible to gauge, and the whole retail complex earns (or loses) vastly different margins on various items. So the complex of middlemen (the links in the global supply chain can go to hundreds in retail) absorbs a large part of the price swings but this is impossible to track in the aggregate. Don’t forget that many items list at 10× or even 20× the price of manufacture — if they didn’t, they could not absorb losses and other costs involved in the whole chain: the price of actually making something has less and less to do with actual costs. We are a long way from ordering a pair of shoes at the village cobbler whose costs are the shop, the leather, and the time.

Who absorbed, emphasis -ed, as opposed to -s, would be a much less fundamentally misguided headline.

As is always the case in social “sciences”, there is simply no justification for supposing any empirical observation carries any relevance at all, for any other time, place and circumstance than the one specifically studied.

The graph makes sense to me. The major buyer’s price discovery systems today are essentially real-time, and their leverage on the seller is the same, making for stickier final product pricing.

Individual buyers in the product supply chain, of which there may be many, however, have far less leverage and fewer real time pushback options. Dickering with a supplier over a piece part too much can put a line down and send a thousand people home.

A buyer’s rejection of a seller’s price increase for 1,000 widgets is more likely to send the seller agent home if things aren’t worked out quickly.

My old firm used to do high volume machining which is a very competitive industry…probably the closest thing to pure competition. We would make thousands upon thousands if not millions of the same part. Raw material costs roughly averaged 30% of total cost depending upon materials used. Machining time is what we were really getting paid for.. We always looked at ‘Value-added’ as a reflection of our profit.

In some cases of machining expensive stainless steels, titanium alloys, and bronzes, we would most likely eat a cost increase in raw materials a time or two hoping the market would stabilize. No need to upset the apple cart with our major customers that can and would shop the item worldwide. I really couldn’t blame them, because their corporation was under the same pressures as we were with competition all over the place.

If raw material prices continued to escalate, we would have to pass on an increase. We figured that our competition would be getting hit with the same increases as we were seeing.

Tough business. Some customers would move on to other suppliers at a drop of a dime. Others were more sympathetic to the issues of raw material increases.