by Mish

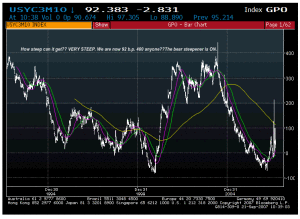

Don’t look now, but the bear steepener is on. And it is on big. How big? Well in the chart at the bottom, you will see the spread between 3 month bills and 10’s. The spread now? 92 basis points. Yes, this is much steeper than the inversion we were used to.

Previous steepeners go to 400 basis points over the past 15 years. Considering all the global dislocations and the dollar, and a Fed that is insistent on blowing bubbles, 400 may be be a bit conservative.

Welcome to the bear steepener.

(click on chart for a sharper image)

Ways The Yield Curve Can Steepen

- 1-Yields on the short end drop with long term yields flat

- 2-Yields on the long end rise with short term yields flat

- 3-Yields on the short end drop faster than yields on the long end

- 4-Yields on the long end rise faster than yields on the short end

- 5-Yields on the short end drop and yields on the long end rise

Let’s discuss the relative merits of the above 5 options and see how we come up with a 400 basis point steeping.

1 – Depending on where one starts measuring (let’s assume 5.25 for the sake of argument) a steepener accomplished solely on short end dropping with the long end staying flat would take the short end down to 1.25.

2 – Option #2 is achieved if Bernanke is done cutting yet after one move, yet yields on the long end continues to rally . I suppose it is possible if the market were to force Bernanke to stop cutting, but this option does not seem very likely.

3 – The problem with option #3 (assuming one is looking for a 400 basis point move) is that Bernanke will run out of room. Interest rates won’t go negative.

4 – Option #4 suggests Bernanke is about to start hiking. With weakness in housing and worries over financial contagion, this scenario seems unlikely unless you buy the Goldilocks mid-term cycle correction theory with everything coming up roses. I don’t buy that rosy outlook for numerous reasons.

5 – If one starts measuring from the first rate cut then option #5 is what has happened so far. Long end yields have risen as Bernanke did a shock and awe campaign during two consecutive options expiry weeks. But with the continued spillover in housing, if the long end yield rallies as the short end drops, Bernanke might be forced to stop his rate cutting campaign. Again, this option does not seem likely.

Struggling Job Market and Falling Consumption

To help resolve which one of the above is most likely one must ask: Are the conditions now more like mid-cycle 1994, late-cycle 1999, or more like 2001 when Greenspan slashed and burned rates to 1% in a panic move to stave off deflation?

Chris Puplava writing for Financial Sense Fill ‘Er Up, Please is looking at the jobs market and falling consumption as the tell.

“When looking at the figure above, it’s hard to go along with the mid-cycle slowdown mantra when the two above indicators look nothing like they did in the mid 1980s and mid 1990s mid-cycle slowdown periods. In the mid 1980s period, retail sales bottomed near 5% with the change in employment dipping below 100,000 only slightly and briefly before both reaccelerated. Both employment and retail sales were even stronger during the mid 1990s mid-cycle slowdown with a recession averted. However, the three month moving average for the current change in monthly employment is 44,000, declining sharply from last month’s reading of 108,000 and retail sales on the verge of falling below the 4% level with a current reading of 4.14%. If both trends continue we may enter a recession as early as the fourth quarter of this year as recessionary risks increase.”

Well stated Chris. That is a compelling rebuttal to the mid-cycle correction thesis. But let’s also take a look at the yield curve from 1999 to present to see what clues we can find.

Yield Curve 1999-Present

Does anyone remember Greenspan’s Conundrum? He was puzzled as to why long term rates barely rose in the face of 17 consecutive hikes on the short end.

What about a Reverse Conundrum? Why can’t the long end barely budge relative to the short end when Bernanke continues his shock and awe campaign. I think that’s likely, which is the scenario presented in option #1.

I just somehow doubt we see 400 basis point but at least the overall idea seems plausible. If so, I would expect the long end to drop somewhat (just not much compared to the short end), and certainly not enough to help because the problems are with mortgages on the long end. For more discussion why rate cuts won’t help, please see Will Rate Cuts Save The Economy?

Several people Emailed me about Bernanke’s Bullet Misses The Mark. An objection presented was that Bernanke hit his mark, because his mark was bailing out banks. Yes his target was in reality banks (and the stock market) and I have said before that “banks, banks, and banks” are his top three concerns. So yes I was aware of it. Thus a better way of saying things is Bernanke missed the mark in helping those who need help most (cash strapped consumers).

Prof. Scott Reamer addressed that very idea as well as the moral Hazards of the Fed in his latest missive: Bernanke Stumped by Representative Ron Paul. His post is as of this writing sitting in the top spot on the DollarCollapseBest of the Web list. Prof. Reamer’s post is well worth a read and deserving of making that list.

Mike Shedlock / Mish/