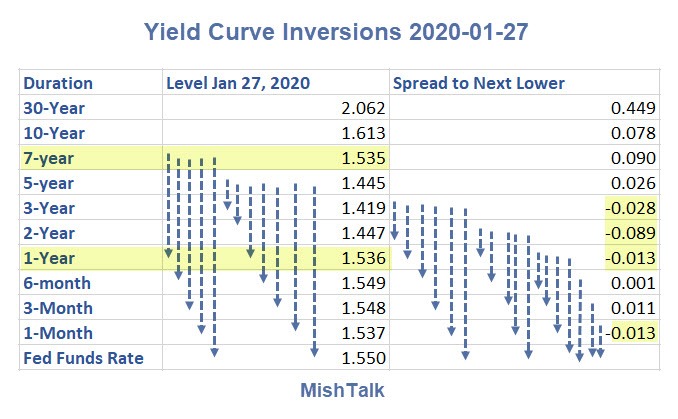

With growing concern over the Coronavirus, yields dropped again today and portions of the yield curve are inverted out to seven years.

For example, the yield on the 7-year not is lower than the yield on the 1-year not and everything shorter in duration.

Yellow highlights show the yield on the 3-year, 2-year- and 1-year notes is each lower than the next shorter duration.

And the yield on the 30-year long bond is again flirting with the 2% level.

For discussion of the coronavirus threat, please see Hundreds of Virus Carrying Planes Headed for US, London, Paris, Vancouver.

Also see Chris Martenson’s proclamation regarding the World Health Organization: “WHO is Derelict” on Coronavirus

Mike “Mish” Shedlock

create debates!

Mish has mentioned many times that duration mismatch (Borrowing short term at low rates and lending long term at high rates.) is a fraud allowed to exist in the financial system. Yield inversion certainly would punish lenders who not only simply participate in duration mismatch, but also make it a leveraged portion of their business.

Yep… been really watching it crush down for the last week especially. Take a look at the collateral side of the repo market. Is this caused by MBS?