Fed Fails to Un-Invert Yield Curve

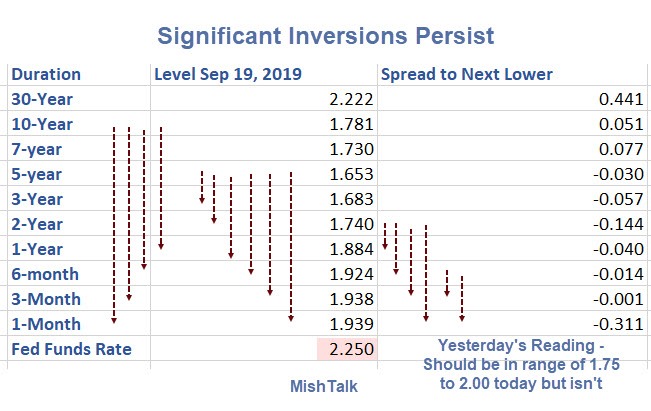

Huge portions of the yield curve remain inverted, just not as deep as a few weeks ago.

At the long end, the 30-year bond yield rose from 1.938% on August 28 to 2.375 on September 15.

Today, the long bond yield is now back to 2.22%.

Fed Struggling with Rates

The Effective Fed Funds Rate should be in the range of 1.75% to 2.00% following yesterday’s cut but it isn’t.

Yesterday, the rate should have been in the middle of the range of 2.00% to 2.25% but was at the high end. On Monday it was at 2.30% and thus outside the range.

The Fed has been struggling for day keeping interest rates in its target range.

On September 17, I noted US Overnight Interest Rate Surges to 10%, Fed Injects Emergency $75 Billion.

10% is more than a bit outside the range but the effective FF rate closed at 2.30% following emergency injections. The emergency injections continued for a third day today and will continue for a fourth day tomorrow.

Something is very wrong somewhere.

Mike “Mish” Shedlock

A taste of a market based interest rate if only for a few days. However, the market has been destroyed the FED, so it is in its own trap.

I forgot about the block Bloomberg has placed on external links. The article tried to link was “Get a Grip. The Fed Can Handle the Repo Market” by Bill Dudley, dated Sept-20-2019.

Attempting to answer my own questions posed earlier on this thread:

Could most of the Federal Funds shortage be due to large Treasury issuance recently sucking liquidity out of the banking system (i.e. money going to Treasuries is not available to lend to peer banks at Federal Funds rate)?

Possibly the reserves from QE parked at the Fed earning IOER were already 100% pledged for the prior purchase of Treasuries, so they are not at all liquid?

Federal Reserve only just this week realized that large Treasury issuance caused a shortage of cash that is expressing itself in the short term interbank funding market. They chose to call this a “timing problem” instead of a “US Government Funding Problem?”

Could “Organic Growth” be a euphemism for “Growth in the economy underwritten by federal deficit spending, and requiring monetization by the Federal Reserve on an ongoing basis to be sustainable?”

I am reaching at straws here. Insight from someone with a deeper understanding would be welcome.

Economy so ridiculously bad for such a ridiculously long time…only option left on the table is…..drum roll….QE forever/NIRP….forever….printing…….quadrillions,forget trillions,fed will print biblical levels of fiat (gloves comin off) in the next round of (overt)QE…..forever….. until they can’t!

“only option left on the table is…..drum roll….QE forever/NIRP….forever….printing”

I think, historically, impossible economic situations have been resolved by war. That shuffles the economic decks very quickly.

War today means nuclear annihilation and extinction.

“Shuffling” is no longer an appropriate term.

Between explanations from@Country Bob and internet research, I am thoroughly confused.

If a large bank does not have acceptable collateral to borrow at the official overnight rate from the intermediaries, why would their refusal to lend to that distressed borrower affect the published FF rate? Am I to understand intermediaries cannot say “no” without affecting the published rate?

If the intermediaries are flush with cash due to excess reserves collecting IOER and yet they still will not lend to the bank that needs funds for 24 hours except at very high rates, why on earth would the Fed go around the intermediaries and use a repo operation to lend to this borrower directly?

Powell reinforced the explanation that this problem was due to a timing mismatch between Treasury issuance and reserves/cash on hand. He suggested an open ended POMO (QE) might be created at some future date to better match “organic growth.” Don’t the intermediaries (primary dealers?) have something like $1T in reserves collecting interest at the Fed? Can’t they lend against that if they want to?

WTF?

Yes, very good questions. Obviously it cannot be lack of cash. There’s more going on…

Collecting interest on excess reserves is much safer than lending for a slim return. When they cut rates, they usually cut IOER, so there is barely any change there. The real issue is that persistent foreboding of the cliff. This will not calm nerves.

‘Something is very wrong here’….indeed.

I don’t want to see people lose their jobs. Hoping for a recession is always wrong -do you hear me, Bill Maher?- but in all honesty, I think it’s not only inevitable, but perhaps much needed. I mean, seriously….how long they can keep this up?

Since the debt gluttony just keeps going and society is not reversing course, the best one can wish for is a mere recession soon before a full depression comes due

“Hoping for a recession is always wrong”

???

What is right, is for things to be priced correctly, and scarce resources employed efficiently.

Hoping that thieves lose their well paying jobs as state certified burglars, is not in any way, shape nor form wrong. Even if it follows, that those living high off of selling those erstwhile burglars Jimmy Choos and BJs, will also have to find something productive to do with their lives for a change.

Crying over the guys losing their jobs in the slave trade, as a result of the recession following emancipation, doesn’t make much sense at all. And no, things are not different now. Those feeding off of the Fed’s theft of others’ livelihood and freedom, really are no different, in any meaningful way, than their Antebellum predecessors.

Problem is that the state certified burglars won’t be the first to lose their jobs. They may be the last…

I think we mean the same, we’re both sick of this lunacy.

… much needed? Pardon me, but name one benefit that “we the little people” ever got from the that spending.

I should’ve added, a much needed return to normality. Obviously, they are artificially extending the cycle and we need to head back to the situation where savers aren’t penalized anymore. It’s the upside down where the debtors have had a decade of advantages and the savers lost trillions.

Who the heck needs $100B-s in emergency funding and able to hide in plain sight?

I believe the reason for the Feds struggling with rates is that the tax collections are way down due to the 20% tax break for small businesses. In addition, professionals and small businesses set up new defined benefit pension plans because they could essentially no longer deduct state taxes and mortgage interest for 2018 so they set up these new plans for 2018 and the money needed to be deposited for 2018 on or before September 15, 2019. So there is a cash crunch due to all this idle cash going into defined benefit pension plan brokerage accounts.

I think the real question is whether there’s a lack of cash as the fed contends or if someone has crappy collateral like Lehman.

The banks are still sitting on Tr$ 1.35 of excess reserves, but they would rather sit on it than swap it for the securities offered at much better interest rates. Safe to say it is the collateral or there is some kind of extortion play.