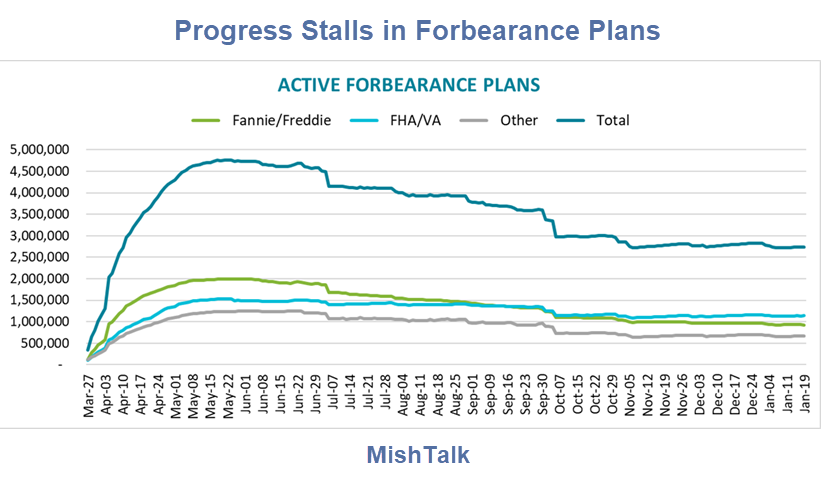

Forbearance Plan Plateau

The Black Knight Forbearance Tracker shows 2.74 million homeowners were in active forbearance as of January 19.

The number has vacillated between 2.71 and 2.83 million since early November, when the country began seeing new coronavirus case spikes and resulting shutdowns.

Estimated Monthly Advances

Covid-19’s Financial Toll Mounts

The Wall Street Journal reports Covid-19’s Financial Toll Mounts as Homeowners Keep Postponing Mortgage Payments.

The proportion of homeowners postponing mortgage payments had been falling steadily from June to November, an indication that people were returning to work and the economy was beginning to recover. But the decrease has largely flattened since November, when the current wave of coronavirus cases surged in communities across the country.

For roughly the past two months, that group of homeowners has flatlined at about 5.5%, according to the Mortgage Bankers Association. Though that is down from a peak of 8.55% in June, some economists are concerned about the stalling forbearance rate—and worry that it could even start climbing if the economy further sheds jobs.

Mortgages by Stage of Forbearance

Forbearance Math

80% of 2.74 million have extended forbearance. That’s 2.2 million people who have not made payment for an extended period.

9.4% of FHA/VA loans are in forbearance.

How are any of the seriously behind people supposed to catch up?

Most likely that can’t and wont. Instead balances will at some point be rolled into new mortgages by the lenders, perhaps by an act of Congress.

Mish

While those of us who were smart and waited out the bubble have to sit and wait more with artificially inflated prices with no true price discovery. BS.

In that case, why not stand by your convictions and short RE on a trading account or through a brokerage?

It’s what Kyle Bass did, he researched it and concluded R/E prices were unsustainable back in 2007.

At the very least, use a short as a hedge to any current r/e purchases.

I’m conflicted, I don’t necessarily want people to lose their homes but I’d like to buy one within the next two years. Prices are extremely out of line. If we were truly in a market driven economy, home prices would fall with increased foreclosures. Rent prices would also drop due to evictions…everything is artificial.

Putting 2% down on a home doesn’t make it “their home”. Sure, nobody likes to see people get kicked out of their present living space. When it comes to homes, just picture people cutting in line in front of you to buy what you had your eye on. You won’t feel so bad about the system “clearing the way” for you. Problem is, the system has been broken for more than a decade.

The question is how many are unable to pay vs how many can pay but choose not to. I suspect many fall into both categories.

I thought the mortgages simply had the schedule pushed back. Are the mortgage holders on the hook for accrued principal and/or interest?

Too much unnaturally-cheap debt on too-easy terms is driving up asset prices in every corner of the economy, from real estate to the financial markets. Human nature is to push things to the limit if allowed. My view is we’re up against that limit. As a nation, we’ve fallen for the “teaser rate” trick. The continuing wave of defaults can’t be swept under a carpet forever. Look out below!

“Too much unnaturally-cheap debt on too-easy terms is driving up asset prices in every corner of the economy, from real estate to the financial markets”

Winner, winner, chicken dinner.

Now, consider that the Fed has been serially cutting rates for 40 years, especially at each recession in order to free household disposable income to offset wages not growing at inflation.

Debt, especially mortgages, isn’t as easy as it was to get back in ’08, the reality is increasing rates now would suppress consumption without wages to match, but that could be an oxymoron, where higher wages would also pump demand, the Fed would then tighten.

After ’08, regulations on mortgage requirements were increased, back then “no income” loans were a huge contributor to the sub-prime bubble.

In other words, current housing demand and prices might be as close to natural as possible.

If you own, it’s good news, if you’re going to buy, not so much, maybe best to anticipate a reversal of the 40 year trend of lower and lower rates, get a fixed mortgage now while it’s affordable….assuming the rising popularity for a $15/hr min wage is done with Dem control in D.C.

The new paradigm is as soon as you save 2% down for a house, you “buy” it! Lose your job? Nob prob. Just chill out in the pad for as long as you need to get another one, then resume payments with a modified plan. Sure, you might accrue some fees which gets added to the “what you owe” column, but all that goes away once you sell and our government/banking sector are always making sure house prices will go up, so that problem will go away. Additional wiggle room for making prices go up can be had with longer loan terms (i.e., 50, 100, etc.) since Fed is already in a corner with respect to low interest rates.

How many renters not paying?

They really don’t count since they ain’t playin’ society’s take-on-lots-of debt game. We are all supposed to play it you see.

I am looking into that for an article

Mish, if it’s worth anything, here in NC I manage 130 rentals and about 10 percent are not paying. Some of those 10 percent are making monthly payments but not catching up, which is better than nothing.

HOnestly, from my perspective, it’s almost over. Most of my renters are catching up except 2.

This is NC though, and everyone is moving here from NJ and NYC.

Kicking people out of their homes will only create more problems. One solution as Mish mentioned is a new roll-over mortgage. Another possibility would be equity sharing with the government if the government makes up the missing payments (I would only do this with owner occupied homes not rental/investment homes).

Are we running out of houses to sell. We are going into Spring with a historically low amount of inventory.

Thanks. Nice analysis.

I have six houses in 5 widely separated Austin neighborhoods in close in burbs, counting my own house, and all are still showing rapid price appreciation trends right now, according to Zillow. My personal house (the most expensive) is rising the fastest.

I doubt we see prices drop much at all in this particular market…but I do expect them to flatten. This current trend is kinda scary. I’d like for it to flatten a little.

Hope I’m not too old to sail a boat when that time comes. 🙂

Short term, many renters in the city are buying a suburban home for 2 reasons. If they can work from home, no need to pay a premium to be close to work and after the BLM riots, who wants to live in a city?

COVID won’t affect RE long term as much as subprime did……unless we never beat it. Then all bets are off.

I think you’re right about the solution. It looks like the 5.5% of homeowners who lost their access to paying jobs (and business bail-outs are going to lose their houses unless the government makes the mortgage lenders make modifications…..which they will, probably by adding payments on to the end of the loans.

Some smaller percentage share of that group will default anyway.

The difference I think, from 2008-2011…will be that prices will not drop as much….which will do a lot to keep the defaults from turning into a snowball.

After subprime only about a third of the people who lost homes managed to get back into them. So now we will probably see many of these new defaulters become part of the growing renter class.

Again, less than 50,000 jobs were created in January 2021. Also Christmas 2020 was horrible. When people don’t have jobs for extended periods, everything snowballs. Trump was trying to get people back to work. Biden killed over 15,000 high paying jobs during his first week in office and messaging of a long dark winter is less than upbeat. That messaging tells employers not to hire, and they haven’t been hiring. As foreclosures heat up, homebuilders will go under again, causing more job losses. Bankers will lay off mortgage departments, more job losses, finally there will be another stock market crash because enough people will have lost jobs, homes, etc. Just like last time. And home prices will crash again, causing a new round of underwater mortgages where someone paid $200K for a home that due to crisis drops to $100K, and making the owners walk away from their homes.

Elections have consequences folks! To make matters even worse? Kids are now 2 years behind in education, meaning USA job market will be fucked for another decade because it will lack qualified workers. Thanks teachers unions!

New Mortgages seems highly likely to me too.

Especially since rates are hovering around an all time low. Many of these mortgages were likely taken out a few years ago at higher rates. If the gov’t mandates new mortgages, especially if the gov’t covers the re-fi fee (or forces it to be done for nothing for certain borrowers – those without jobs) many may find they have lower payments than they did before even with accrued interest over the last year when they haven’t made any payments.

I can’t imagine this gets anywhere close to what we saw after 2005-2008

I just paid $12,000 of $18,000 in 1 check of my forbearance since April, and I will say with less than 50,000 jobs created in January 2021, that this foreclosure crisis will be worse than the last one. And keep in mind Biden doesn’t know how to create jobs, he only knows how to bankrupt everyone. Also keep in mind that it is easy to pay back something if you are only a few hundred behind. When more than $5000 or $10,000 behind, it will be a blood bath. For example in 2005 my house was worth $350K, by 2010 it was down to $120K with no buyers. It took until 2015 for prices to recover. Now my house is worth $277K. And it will quickly drop to $120K again once foreclosures start again. My case is even more scary because I only owe $70K on mortgage now. My home won’t be stolen from me, but it is going to be a bloodbath for millions. And repercussions will be a housing industry that dies again. It won’t be just foreclosures. Everything will be fucked for another decade.

These will become 100-year mortgages.

I think they have 50 and 100 year mortgages in Switzerland. Interestingly in many “poor” eastern European countries people own their residences outright and taxes are minimal.

I believe that might apply to rural areas in the US too. I have no facts to back it up just an impression from living in fly-over country.