Please consider the polling results of a Study on the American Dream.

What Best Describes Your Views?

Key Findings

- 3% of Millennial live the American Dream.

- 16% of Boomers live the American Dream.

- 25% have abandoned the American Dream.

- 11% overall (13% of Millennials) never believed in the American Dream in the first place.

- 52% (54% of Millennials) believe the American Dream is possible.

Top Ingredients of the American Dream

Key Findings

- 56% of Millennials prioritize home ownership vs 68% of Baby Boomers.

- 49% of Millennials prioritize retiring comfortably vs 73% of Baby Boomers.

- 41% of Millennials prioritize having children vs 36% of Baby Boomers.

- 38% of Millennials prioritize car ownership vs 42% of Baby Boomers.

Point two is bound to change as Millennials get closer to retirement.

Points 1 and 4 are secular changes making the Fed’s attempt to inflate much more difficult.

Point 3 is peculiar and likely subject to interpretation error.

The ability of Baby Boomers to have kids at this point is very restricted. The same applies to the question about getting married.

Motivators to Buy a Home (Non-Homeowners)

Only 8% of millennials have no interest in buying a home compared to 46% or boomers.

This is despite the fact that 56% of Millennials vs 68% of Baby Boomers prioritize home ownership.

Home Ownership Plans

Key Findings

- 29% of Millennials who purchased a home dipped into retirement income.

- 19% of Millennials who plan to purchase a home expect to dip into retirement income.

If they are forced to sell for any reason and have a loss they have a bad tax consequence.

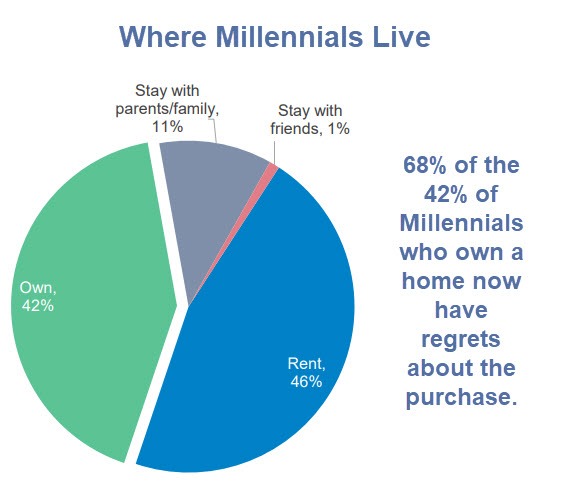

Regrets

Reason for Regrets

A whopping 68% of millennials who bought a home now have regrets. Only 35% of Baby Boomers have regrets.

The latter statistic is likely skewed to the downside.

Why?

Many Baby Boomers lost their homes in the Great Recession. I suspect most of them have regrets but were not sampled in the survey.

Also, many boomers who may have regretted their purchase a short while ago have no been bailed out by the Fed. There has been few comparably few bailout of Millennials.

Attitudes on Debt

This is a poor set of questions, especially the way two answers are lumped together.

Key Finding (Derived from 2nd Question)

- 68% of boomers are not comfortable carrying debt.

- 56% of Millennials are not comfortable carrying debt.

The second question suggests boomers have learned something that Millennials haven’t.

But we do not have breakdowns and the question is subject to interpretation errors.

Possible Interpretation Errors

- Does credit card debt paid off every month constitute debt?

- Is a car loan debt?

- Might some respondents view mortgage debt as debt and others not?

If the answers to those questions are random, it might not matter. But Boomers might easily think differently about those questions than Millennials and thus answer differently as a group.

Either way, it would have been far better had the survey not lumped two answers together.

Investment Horizon

Safe Investing Question

Financial Crisis Question

Despite Millennials saying time allows them to be more aggressive, it appears they haven’t done so.

But what does “aggressive” mean.

Might it mean one thing to Boomers and another to Millennials?

At this stage in the bubble, even passive index funds might easily be considered “aggressive”.

Investment Vehicle Question

Biased Interpretation

Here the question is perfectly valid.

The study’s interpretation of the answer is as biased as can be.

The study comments “This reluctance to invest is demonstrated by Millennials’ underutilization of investing accounts that could help them build wealth for retirement.“

What a crock.

Boomers most often worked for companies that had retirement plans. Millennials can not say the same thing, at least to the same degree.

Millennials also have a need to pay down student debt. Few Boomers do.

Not investing means “no money” and/or “no corporate plans” as opposed to “reluctance”.

Men vs Women Investing Confidence

This one is quite interesting. But it is missing Bitcoin.

Confidence

- 69% of men confident about private equity? Really?

- 64% of men confident of futures? Really?

- 56% men confident on derivatives? Really?

Are men simply more confident than women about everything? Or do they just claim to be?

I suspect the latter.

California vs Rest of US

Conclusion

Despite some poor questions and biased interpretations of some answers, this was an enjoyable and informative poll on the attitudes of Millennials vs Baby Boomers.

Mike “Mish” Shedlock

Mish, I ust looked at the methodolgy for this ‘study’. I am not a statistician, I have my doubts about the verasity of this work!!!

Most millenials would presumably have bought after the 2008 crash. Surprising that they’re not happier about catching the bubble reinflation.

Its funny reading these comments about America. You could be talking about Australia and many of the comments would be almost identical.

Over here I see the housing market as hollowing out the economy. I know many prominent economists would say I’m wrong and that my experiences are purely anecdotal but from the people I mix with, discretionary spending is way way down due to mortgage stress and utility prices which always seem to be rising even as headline inflationary figures remain static or even decrease.

I think its only a matter of time before before a housing induced slowdown catches up with retail (its already begun) and we see malls around the country beginning to close as they have in the US. I think it would have happened except that that Australian population is so highly concentrated in urban areas that they’ve been protected in a way that their counterparts in the US were not.

On a purely personal note I worked as a concrete labourer of recent times doing residential construction. Its obvious that many first home owners are building places which are vastly too large and that land prices are frequently ridiculous. But I guess if they don’t build McMansion’s then the banks don’t approve their loans.

“Its obvious that many first home owners are building places which are vastly too large “

…

Yes, that is rampant. Know quite a few folks that have multiple rooms that are never used (or for storage only). Why? Oh, I know – keep up with the joneses. Never understood it, since my brain would try and calculate the wasted $$s on property tax, insurance, utilities, maintenance … as well as a higher mortgage than needed.

Surely, the millennials will save the day when they swoop in and purchase their 4 or 5 BR home …

“Its funny reading these comments about America. You could be talking about Australia and many of the comments would be almost identical.”

Yes, the housing scam seems to be a developed country phenomenon. Europe, Asia, North America – doesn’t matter. The pyramid scheme is practiced by every government regardless of political stripe.

I bought a house because I wanted to pay it off and never have to rent. I paid mine off after 12 years. The monthly savings allowed me to pay off everything else within a year. Without debt, I could care less if I get fired at my job. Since I could care less, I’m free to always do the right thing at work. Since I always do the right thing, I keep getting promotions and more money.

Of course I don’t live in California, Chicago or New Jersey. I bought my house at 1.5 times yearly earnings and put 20% down. My property taxes and insurance amount to $175/month.

Oh, and you have to learn how to fix stuff around your house. Turns out, none of it is rocket science. YouTube is your best friend.

University of You Tube!

I did the same, but I pretty much have to keep my job since my wife has cancer and our health insurance is though my work.

Real sorry to hear about your wife. I have a great old friend dealing with cancer too. It’s a terrible thing to go through.

I’m still working. My employer pays $19k/year for my family health plan. That’s a big nut to cover out of retirement income. I could do it, but there’s no guarantee it won’t go up 20% next year. Not to mention it takes a good attorney to decipher what the plan will actually cover.

“This reluctance to invest is demonstrated by Millennials’ underutilization of investing accounts that could help them build wealth for retirement.”

A 75% Nasdaq crash does not promote investment. 50% and 57% crashes in the S&P 500 do not promote investment. Choking on student loans does not promote investing in something one does not have money to invest in.

There are few young couples that recently bought in my neighborhood. A few things I’ve noticed. They have no clue how to fix anything. They’ve asked my advice. For some things, I tell them they can fix it pretty easily. The husband is listening while the wife gleans at us. She clearly wants to hire a professional. And it’s pretty clear who the breadwinner of the family is and who wears the pants.

They have gym memberships and they hire firms to cut their grass. They like to buy hybrid and electric vehicles. And they also like to have outdoor cookouts. My neighborhood always smells like charcoal. They sit outside staring at their phones while the grill spews smoke all over them.

I’m surprised “Earning a 4-yr college degree” was not one of the criteria of achieving the American dream.

Excellent comments by everyone here: 2Banana, Thimk, Abend, Country Bob, Herkie

We finally found something we can all agree on

We bought our first house in Pasadena, California in 1970 for $26,500. Both of us were working at decent jobs and we barely squeaked in qualifying for a loan. The same house sold recently for $840,000. That’s 7% annual appreciation. If we were starting out today, there’s no chance we could buy this same home in a decent, middle class Pasadena neighborhood, even without our piece of the gargantuan $1.6 Trillion college debt hanging around our necks.

Californians rebelled against property taxes in 1977 by passing prop 13. However, total property taxes per year at the state level have also continued to go up at the rate of 7% per year due to reassessment after sale to a new owner.

Finally, 2banana is absolutely correct, the upkeep of a home has continued to ratchet upwards. If you can’t do your own upkeep, you’re in a world of hurt. It’s a couple hundred bucks labor now just to get a stranger to swap out a busted water heater.

A couple of hundred to get someone in the front door just to LOOK at the problem. Then you gotta pay to fix it.

Hot water tank. Stove. Dishwasher. Refrigerator. Dishwasher. Furnace. Built in microwave. TVs. Fans. Washer. Dryer. Etc.

Thank gawd for YouTube fix it videos.

A couple of hundred to replace a hot water heater is a bargain. I paid about $500 a few months ago. It was a hybrid which required more work and it took a couple of hours to drain and haul away the old one.

Homes are freaking expensive!!!! Truth.

Besides P&I, taxes (always going up), utilities and insurance. You gotta take care of the place. Think of all the systems that need upkeep (water, HVAC, electrical, NG, propane, oil, ventilation, rain control, landscaping, etc.) plus every thing is decaying every day.

Think. Your 30 year roof decays 1/(30 x 365) every day. And that is if you take care of it.

I am an engineer. I keep excellent care of everything I own. And I do most of the work myself.

And I am still at Home Depot or on Amazon fixing something house related every weekend.

Why America’s real-estate brokers are such a rip-off

Selling a house in the United States is extremely expensive

Print edition | United States

Aug 29th 2019

| NEW YORK

THE PAST decade has not been great for middlemen, who match buyers and sellers for a slice of the transaction value. Travel agents have had their margins crushed by flight-search and hotel-booking websites. Stockbrokers have been squeezed out by whizzy algorithms that carry out transactions for a fraction of the cost. Taxi dispatchers have been replaced by Uber and Lyft.

There is an exception, however. Even though there are plenty of sites, like Zillow and Redfin, which offer home-buyers in America the chance to search for properties, commission rates for real-estate brokers (estate agents in Britain) have not fallen much, staying close to 6% (3% for the buyer’s agent, 3% for the seller’s). Americans pay twice as much as people in most other developed markets, where similar sites have done much to depress residential-property transaction fees (see chart).

This irks many. “Why is it that residential real-estate brokers’ fees are two to three times higher in the US than in any other developed country in the world?” asks Jack Ryan, who founded REX Homes, a property brokerage that offers to sell homes for just 2% commission. He believes the problem lies in the anti-competitive practices of the Multiple Listing Service (MLS), through which nearly every broker in America lists and searches for homes, and the National Association of Realtors (NAR), a trade association with 1.3m broker members in America, which regulates it.

That opinion is growing in popularity. Two class-action lawsuits have been filed against the NAR and some of the largest real-estate brokerages, such as Realogy and Keller Williams. In America, a practice called “tying” is common, whereby home-sellers are forced to agree upfront on the rate they will pay the buyer’s broker. The lawsuits allege that sellers’ brokers put pressure on homeowners to offer the industry standard of 3%. If they refuse, buyers’ brokers may refuse to show their home to clients.

This is possible because of the MLS. In April, the Department of Justice (DoJ) began to subpoena information about how brokers use the system, looking for evidence that they search for homes by commission rate. If found, it would corroborate the idea that buyers’ brokers invariably steer buyers to homes that offer the juiciest commission. The NAR moved to dismiss both suits in early August. John Smaby, the President of the National Association of Realtors, says the lawsuits are “wrong on the facts, wrong on the economics and wrong on the law”.

But the market seems to think there is plenty to worry about. Many large real-estate brokerages are privately held, but the share price of Realogy, one of the brokerages named in the suit, has fallen by half since the end of April, just after news of the DoJ investigation leaked. The value of RE/MAX, another listed brokerage, has fallen 40% over the same period.

If transaction fees are being kept artificially high by these practices, that is bad news for homeowners. Some $1.5trn worth of homes change hands every year. If anticompetitive practices are elevating American brokerage fees by two to three percentage points above where they might be otherwise, this is costing consumers as much as $70bn per year, or 0.25% of GDP.

The costs to the American economy are probably higher than that. When moving house is so expensive, many people may not bother. That means less spending on services associated with moving home, such as gardening and decorating. Worse, it may also be suppressing mobility in America. Ben Harris, who was the chief economist for Joe Biden when he was vice-president, argues that average incomes in poorer cities are not catching up with those in rich ones, “in part because people aren’t moving any more”. Extortionate real-estate commissions are hardly the only problem—wealthy cities such as San Francisco need to build new housing if people are to move to better-paying jobs there. But they certainly do not help.■

This article appeared in the United States section of the print edition under the headline “Sellers beware”

Print edition | United States

Aug 29th 2019

Millennials are doing it all wrong as usual. You’re supposed to buy low and sell high, not buy after the bubble!

It’s their own fault for not buying before the market went full retard in the mid 2000s. I don’t care if they were only in high school at the time, you have to have the foresight to seize the moment!

They’ve been screwed by socialist government policies that made it easy to borrow, Without the GSEs, there wouldn’t have been a housing bubble. Without Fannie Mae, there wouldn’t be an education bubble. And they fail to see the obvious and support the democrats.

Every time I meet a millennial, it makes me wonder how the US education system got so fouled up so quickly?

The millenials are the first generation trained entirely by college professors who have more in common with Peter Pan than Joe the Plumber (I don’t ever want to grow up!).

Imagine “paying” (or borrowing) tens of thousands of dollars to be lectured at by people who couldn’t hack it in the real world. Millenials were told that college is a sure thing, they would be crazy not to go to college…. and they went, they have massive debts to prove they went, and yet the college professors (as a group) who taught aren’t prepared for real life. How can Professor Peter Pan possibly train someone to do something Prof Pan can’t do himself?

Having made that whopper of an mal-investment, the debtors — make that millenials — are told that home ownership is the next “sure thing”. Buy a house in a market where the government is absolutely focused on destroying whole industries while raising property taxes to pay for that destruction.

Low skill, low pay jobs will not float a half million dollar McMansion with massive property taxes. It doesn’t matter what mortgage rate the Fed conjures up.

The difference in attitude is not with Millenials vs Boomers. The difference is that socialist municipal governments have destroyed the jobs that are able to fund home ownership.

Even the millenials are connecting the dots. We are just waiting on the bureaucrats to figure it out.

Universities have never taught trade skills like plumber, electrician, etc… .

The whole reason to go to college was so you wouldn’t have to be plumber.

And they’ve never taught useful skills unless you go to law or medical school. I have a BS and MS in engineering and do computer programming. Which I taught myself. Although my first 2 jobs out of college was writing engineering software.

My plumber has a college degree in marketing. Marketing pays bupkiss.

His dad is a plumber, so he apprenticed “temporarily” until a marketing opportunity opened…. that was 25 years ago. If college was supposed to help him avoid becoming a plumber, it didn’t work.

I would think marketing is a lot more career oriented track than white privilege transgender normative studies.

I suspect transgender normative studies will allow new grads to avoid being in marketing or a plumber or anything else — they aren’t qualified to be a plumber or anything else.

68% regret buying? Just wait till the next great crash when they are nearly all underwater on their mortgages and they can’t sell, they will have to surrender the place to move.

“Sorry man, but like your house is worth like less than the back property taxes on it.”

If public employees can retire with full pension after 20 years (and racking up overtime their last 2 years to bump up their pension pay), someone has to pay for that. If you aren’t sure who the sucker is paying for this…. check your mirror.

Q: What is the first thing a public union goon does when he/she retires at 55 on an full OT spiked, tax free disability, COLA, free medical for life pension?

A: Moves to a low tax, right to work red state.