Overnight lending rates spiked as high as 10% in the past few week.The Fed blamed it all on end-of-quarter financing needs.

The Fed then made some emergency “overnight” and “short-term” repos to get through the end-of-the-quarter.

Following the emergency actions to suppress interest rate spikes, Philadelphia Fed President Patrick Harker explained “This is not QE4. This is not a monetary policy tool.”

WTH is It?

If it’s neither QE nor a “monetary policy tool”, then what the hell is it?

Tiddly Winks?

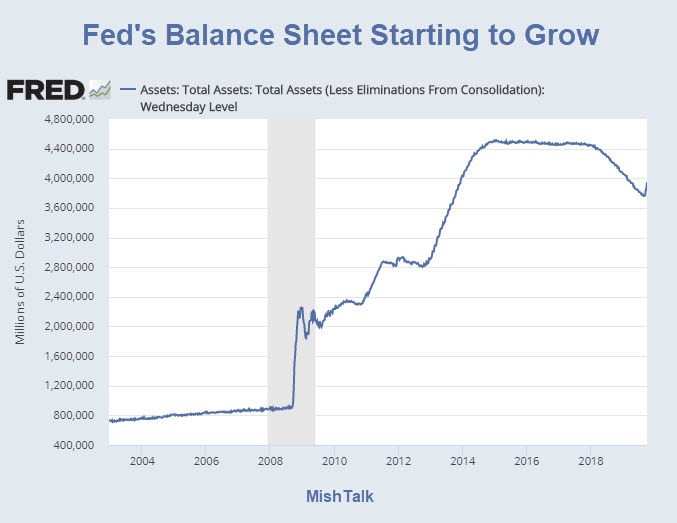

Looks Like QE, Stinks Like QE

The Fed’s balance sheet is growing again.

Harker explained QE growth will be “organic”.

Actions prove otherwise

Is the Third Quarter Over?

Inquiring minds may be asking “Is the third quarter over?”

That seems to be a simple question, but let’s check a calendar to be sure.

Yep. It appears the third quarter is over.

So let’s check on those Repo Actions to get us though the end-of-quarter financing needs.

Fed Repo Actions Overnight and Term

The overnight operations replace each other. One needs to add up what does expire.

I come up with 30+60+60+75 = $195 billion.

Not Monetary Policy

In regards to Harker’s statement “not a monetary policy tool” please note the repo landing page link name:

www.newyorkfed.org/markets/domestic-market-operations/monetary-policy-implementation/repo-reverse-repo-agreements/repurchase-agreement-operational-details

Note that end-of-quarter needs stretch all the way until October 11. But let’s not stop there. Let’s investigate Term Repo operations.

Scheduled Overnight and Term Repos

New Definitions

It appears we have new definitions of “overnight” and “end-of-quarter”.

End of third-quarter needs stretch all the way until November 12. Fancy that.

The $30 billion term repo that expires on October 8 (first repo chart) will be replaced by a $45 billion term repo on October 8 (second repo chart)

But also note that expiring a total of $120 billion in repos will expire October 10 and 11. Those will be replaced by only $90 billion in new repos on those dates.

If it played out exactly that way there would be a small $15 term repo reduction on October 11.

However, we also need to add in $75 billion “overnight” every day from October 7 through November 4..

At Least Kicker

Please note the “At Least” kicker. The first chart has an explicit dollar amount.

All items in the second chart say “at least”.

At Least $250 Billion Through October 17

The overlapping term repos between October 8 through October 15 all expire no sooner than October 17.

I count 45+45+45+35 in term repos + $75 billion in continual “overnight” repos = $250 billion (At Least)!

On October 17, at least $45 billion will expire to be replaced by at least $35 billion.

Then on October 22, at least $45 billion will expire to be replaced by at least $35 billion.

I just came across this Tweet.

Low and behold …

Fed Totally Clueless

I believe you get the idea here:

The Fed is totally clueless about allegedly “end-of-quarter” needs.

Addendum

Wolf Richter made this comment.

I just spoke with Wolf on the phone.

The basis of his claim is that repos have been under-subscribed. However, he admits my number is correct if the subscriptions are taken in full.

I now suspect we are both wrong, but in different directions, and the answer will be somewhere between “most will unwind” and increase to $250 billion.

Both of us think the very act of offering more than needed may have calmed the markets.

Also, we both agree that a number of financial institutions are using overnight funding to fund day-to-day operations, and someone got caught with their pants down when rates started to rise.

When trust in those institutions failed, rates shot up to as much as 10%.

As Much As It Takes

For now, the Fed has offered “as much as it takes” for as “long as it takes”.

Sound familiar?

That’s what’s become of ECB policy. For discussion, please see What the Hell is the ECB Doing?

But let’s not call any of this QE nor monetary actions. Let’s call it Necessary Tiddly Winks.

Meanwhile please note that the Fed has Recession Tools, Promises to Use them Quicker Next Time.

Mike “Mish” Shedlock

You know the world has gone crazy when@CautiousObserver writes a comment that doesn’t mention his Trump impeachment fantasy

What is it with people on this blog thinking I am anti-Trump? I am pro-Trump. I do not want the President to be impeached. I only predicted that the Democrats will impeach him if they can, and that they would not be able to do if for Russian collusion. That was quite some time ago made that prediction, Country Bob. Perhaps you are confusing me with “Casual Observer?” (Not the same person)

As for my being critical of the Fed misrepresenting what they are doing, I laid out what they publicly stated versus what they actually did. If you disagree with that, then tell me where I am mistaken.

I am wondering if Fed President Patrick Harker waved his hand aimlessly through the air as he said: “This is not QE4. This is not a monetary policy tool.” After that, did his audience repeat in a trance-like state: “This is not QE4. This is not a monetary policy tool.”

It reminds me of other things the Fed has said, such as “We will not monetize the debt.” (Bernanke) or “The committee is really thinking of this as a…mid-cycle adjustment to policy” not “the beginning of a lengthy cutting cycle.” (Powell)

Beginning with Powell’s mid-cycle statement, the Fed has cut 0.25% consecutively twice and is expected to cut at least a third time at the October FOMC meeting. Since Patrick Harker’s statement, the Fed has extended it’s temporary overnight repo operation from the end of the quarter to include term lending and overnight lending all the way through at least part of November.

Jedi mind tricks or not, I am tired of being lied to by these guys.

I just came across this Tweet.

Low and behold …

That would imply that it’s actually the treasury that is the culprit, would it not?

Can somebody point me to a TBTF bank that has not paid enormous fines for criminal activities? Of course I accept their assurances that they were not guilty ( So why pay the fine?). I understand that there is one ex-JP Morgan employee who has pleaded guilty to fraud charges and is helping the authorities with their enquiries. Is it three JP Morgan executives who have been arrested on RICO charges. Does this put Dimon at risk? Every scam at a national government level seems to involve alumni from Goldman Sacks. Is it all one giant criminal conspiracy against the rest of us?

Money center banking is fully dependent on legally enforced, privileged access to scams, period.

Local knowledge provides a competitive advantage in every field. And funding in a free economy come from distributed deposits. Leaving no possible edge for Money Centers. Instead, their very existence, is proof positive that the playing field not equal for everyone. Hence rigged. Hence a scam.

I’m beginning to believe that it is more than a scam or the powers that be rigging the law to their advantage. It is serial and severe law breaking. You don’t get RICO charges for stealing a baby’s dummy.

Powell knows that’s not close to enough,every major bank in insolvent,the federal govt is completely insolvent,that’s gonna require tens (hundreds)of trillions just to keep big govt from default.Banks in deep chit,no one’s payin em back!TARP 2.0 will be in the trillions to buy time to at least get through the year!

QE is now a bad work, not to be spoken of, like that word that starts with R.

Yup.

All of Progressivism, along with all it’s institutions, are 100%, fully dependent on Newspeak. In progressives’ childbrains, things magically change if “we” just call, or “deem,” or “find,” or “judge” them to be something else.

Emphatic ambiguity is everything when you’re dealing with the public about economic matters.

I wish they’d clear releases with me. It would calm markets tremendously. I’d have said,

“The Fed stands ready to do whatever it takes, temporarily, through the end of the century. We don’t view the present situation as being nearly serious enough to lie about, possibly.”

I can also tell you from experience that the Fed is a totally incompetent bank regulator. Their examiners are generally young, inexperienced and far too few in number. This partly explains why they have no idea what the hell is going on at the TBTF banks that they are responsible for regulating.

That seems to be a feature rather than a bug. Sometimes I wish I’d gone into a field where the desired goal is to produce a lack of results. I bet a regulator’s day is comprised of mostly hobnobbing and long lunches. Banksters have it good!

At the TBTF mega-bank that I used to work at, the Fed examiners were regarded as a joke. At the time, we were also being regulated by the OCC and the OTS, who in all fairness were not. However the OCC and OTS do not regulate the TBTF mega-banks – only their S&L and State-chartered subsidiaries. The Fed is the only regulator of the TBTF mega-banks, themselves.