Rogue Executive Actions

Biden is already bending to the wishes of Elizabeth Warren and Bernie Sanders to want to forgive student loans.

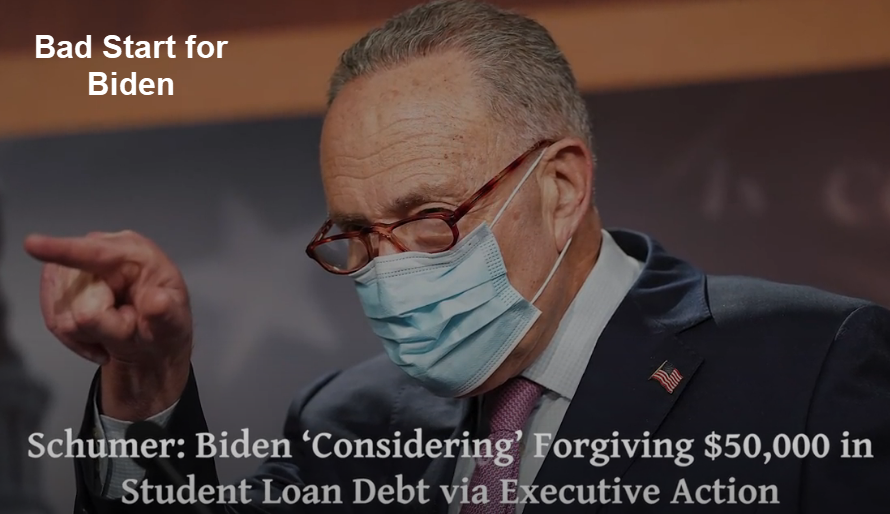

On Monday, Senate Minority Leader Chuck Schumer announced Biden ‘Considering’ Forgiving $50,000 in Student Loan Debt via Executive Action.

Schumer held a press conference alongside Democratic Congressmen-elect Ritchie Torres, Mondaire Jones and Jamaal Bowman of New York, during which the group announced they have “come to the conclusion” that Biden can “forgive $50,000 of debt the first day he becomes president.”

“You don’t need Congress, all you need is the flick of a pen and President-elect Biden — then President Biden — can make this happen,” Schumer said.

Asked if Biden will have the executive authority to forgive the debt, the New York Senator said the president-elect is researching that and “I believe when he does his research, he will find that he does.”

Congress, Who Needs It?

I believe we have seen enough rogue executive actions of dubious legality.

Even if legal, this is a terrible idea. It mainly benefits middle-class whites and unfairly so.

We can’t give money to people at the bottom who have lost their jobs, possibly permanently, due to government decree. But hey, let’s forgive $50,000 in debt to the upwardly mobile.

Less Education for Your Buck

The above chart is from US College Tuition & Fees vs. Overall Inflation.

Please note the acceleration in 2005. What happened?

The cost of education escalated madly when Bush passed the bankruptcy reform act of 2005 making student debt not dischargeable in bankruptcy.

Flashback 2005

On April 15, 2005, I penned The Deflation Guarantee Act of 2005.

Today Congress passed the “The Deflation Guarantee Act of 2005” currently known as the “Bankruptcy Abuse Prevention and Consumer Protection Act of 2005”.

Twenty years from now economists are going to be studying legislation from this Congress and signed by this administration and be wondering: “What the * were they thinking?”.

Anytime this administration passes a law with the “protection” in it, assume it will do just the opposite.

This was a bill written by loan sharks, and bought via payoffs (otherwise known as campaign contributions) to those voting for this bill. It has NOTHING to do with “Consumer Protection”.

I believe this will backfire in many ways, and not all of them are fully understood yet.

Disease vs Symptoms

I graduated from the University of Illinois in 1976 with a degree in Civil Engineering. The cost of tuition was $250 a semester when I entered college in 1971.

Some blame states for not contributing to education. Indeed, states would would not raise taxes to cover escalating costs because of voter backlash.

But that is blaming the disease on the symptom. The disease was then and still is high administration costs, public unions, outrageous coaching contracts, unbelievable pensions, and serious lack of competition.

Five Student Loan Facts

Brookings has a set of Five Facts About Student Loans

that everyone discussing forgiveness needs to be aware of.

- Six Percent of Borrowers owe a third of the outstanding debt.

- About one quarter of borrowers who have about half of the debt borrowed for graduate school.

- The individuals who owe the most money are not the individuals who default on debt

- Most bachelor’s degree recipients graduate with little to no debt

- Even if financial aid covers the whole tuition bill, many students borrow to cover living costs

Questions of the Day

- Given those facts, why should borrowers be bailed out at taxpayer expense?

- If they are, when will it stop?

Dead on Arrival

On November 29, I commented Biden’s Progressive Agenda is Dead on Arrival .

The obvious implication is “DOA in Congress” as opposed to seriously misguided and dubiously legal executive orders.

Compelling Case

HedgEye author Neil Howe makes a compelling case in Is A Student Debt Jubilee Coming?

Colleges possess such extraordinary pricing power in part because they bar or discourage new competitors and in part because lazy employers rely on a limited number of them to act as credential gate keepers. What federal policy ought to do is actively promote new types of educational institutions better fitted to employer needs and to promote measures by which families can fairly compare the value-added of different schools. Colleges and collegiate associations actively discourage all of the above.

In sum, it’s a mistake to enact a student debt jubilee without first rethinking and recasting the whole market for higher education. Otherwise, we’ll either end up right back where we started (with millions of new students crushed by huge debt loads) or somewhere we don’t want to go (with taxpayers committed to covering the cost of whatever colleges want to charge… a bit like they now do with healthcare providers).

Huge Moral Hazard

Debt discharge is a huge moral hazard that encourages more overpaying for useless degrees.

It will do nothing to address the cost of higher education.

We need more competition, more accredited schools, more alternatives, and less public union graft.

Forgiving debt fosters less competition and more graft.

Under Pressure

Biden is under pressure from Bernie Sanders and Elizabeth Warren who believe Biden could not have won without them.

This claim is off by 180 degrees.

Election Message

The fact of the matter is rightful fear of Progressives could have cost Biden the election.

You can see this in the House and Senate races.

Trump lost but Biden had negative coattails. Why?

Fear of exactly this kind of liberal agenda.

Voters did not want Trump but they did not want liberal nonsense either.

Message Not Heard!

Trump did not get the message. Neither did Biden nor the Progressive wing of the Democratic party.

Biden is off to a bad start by listening to the Progressive wing that damn near cost him the election.

Mish

The new scam appears to be “coding school”….maybe it’s not a scam, but it is a new place to spend student loans. In the last couple of years it seems to be really hot around here.

I’d be interested in what some of you more tech-savvy guys think about that phenomenon….is it legitimate training…..and…..how many people sign up for it and pay….but maybe can’t hack the curriculum and drop out/

Our whole economy is built on scams.

An example that currently bugs me is CNN/MSNBC taking on a company like CarShield, which sells service contracts, as an advertising client. These companies will take money from anyone with no concern about whether the company has a good reputation or not. CarShield has an “F” rating from the BBB. This just allows more people to get snookered into their scam but that is OK with CNN/MSNBC because hey, “it’s all about the Benjamin’s”.

The FTC should block companies with a BBB rating of ‘D’ or lower from being able to advertise. But of course, everyone would scream bloody murder that doing so blocks companies from their right to freedom of speech (or being able to troll for more suckers), depending on your POV.

Now the message I’m getting for the election is, don’t change laws illegally. Let’s see how this plays out. Would be fun to see liberals heads explode with anger. lol. https://www.zerohedge.com/news/2020-12-09/how-and-when-scotus-will-overturn-election

Real easy fix going forward, get rid of gov getting involved in student loans and driving prices up. Pay the teachers what they are worth not what they’re getting paid now for 6 or 7 months of work. Get rid of pensions, let them pay for their own retirement like the rest of us. Get rid of all their perks, vacation time, cola’s ect like the rest of America. Prices would crash. Most of the colleges have worthless degrees anyway.

if every other Ahole in our country can default and move on, why can’t the young folks our old geezers hooked with loans when they were mere teens. screw the old geezers. they are the reason our empire is crumbling and so evil.

No they aren’t. They were born into this, just like you were.

But I agree that should be able to default, if they truly cannot pay. I understand that having no assets makes bankruptcy very enticing…..maybe there should be a waiting period before it can happen.

“that most student loan defaulters should get to take bankruptcy”…what I meant to say.

There is a simple fix for the student debt problem:

This would cause tuitions to collapse and becoming very deflationary, which should lead to colleges having to rein in cost.

This system isn’t perfect, but I think it would work better than forgiving $50,000 per student.

I agree, but many would claim racism any time a minority was turned down for a loan.

You have not fixed the underlying problem because you do not understand it. Student loans are the visible tip of the iceberg. Education beyond high school is not a right. It is earned. It should have a purpose beyond extending high school four years or more. This requires barriers to entry. The students who meet the appropriate standards will get jobs and will pay back the loans. The rest should not have been in college in the first place.

What must to happen in the USA is an open discussion of human differences and abilities without the racism burden. People differ in skills/abilities; what must happen is society developing in ways (programs, institutions etc) that recognize the differences and enable all of its members to succeed.

Yes. And Biden was a big supporter, so he would need to reverse himelf.

I’ve said it before, but relatively accommodating bankruptcy laws (and a second chance) were one the great things about America, and, in fact, the meaning of the ‘liberty’ text inscribed on the Liberty Bell.

Amen!

Is forgiving debt a one-time giveaway or will this usher in a defacto $50k per resident to spend at whatever “institution of higher learning” that they want? Given that various governments have already spent $100k+ per pupil from kindergarten to 12th grade, I could see some people just wanting to extend another $50k. The problem is that if that first $100k+ were well spent (effective) 1/2 of those finishing high school would be ready to be productive members of society and the 1/2 would be well prepared to breeze through college with a useful degree while collecting less debt.

Those talking about using conventional loan strategies have to remember that students fresh out of college have no assets. They can simply declare bankruptcy and be done with it. Giving away $50k of taxpayer money does not do anything to solve any problem except the immediate problem of people being in debt, mostly through their own unrealistic choices.

I still anticipate very little catering to progressives from Biden. The DNC feels more emboldened than they have in a long time. They shot down Bernie, Tulsi, and Yang in the primaries and still managed to take down Trump with a feeble old guy in the general election, threading the needle.

Biden’s desire to bring in Neera Tanden is especially telling, since her whole career is based on shooting down Bernie types in the party. The administration is shaping up to be very establishment rather than progressive.

Biden’s only purpose was to beat Trump. When Biden gets sick and steps down, Harris will take up the far-left and socialist agenda.

Harris is establishment too, not progressive. She’s valuable to the party because she’s not afraid to play rough with fellow minorities. She also went really easy on bankers like Mnuchin during the housing crunch.

The only way the Biden admin is far left is if you consider the status quo to be far left. All they want to do is go back in time to 2016 and pretend the last four years didn’t happen, while simultaneously fending off blue teamers who want actual change.

If debt is money, is not cancelling debt lead to deflation?

What in God’s good name did you expect???

The federal government needs to get out of the education business and tuition prices would drop dramatically. They have done a good job of flooding the market with lots of paper and making this paper easy for kids with no to little credit to get thus turning them into professional debtors.

It’s really evil.

But, then fewer kids would be indoctrinated with socialist views. the dems would never allow it.

Here’s a better plan: Give $50k to every citizen over 21.

Hopefully that was a joke gone bad. Or did you morph into some weird combination of Elizabeth Warren and Andrew Yang?

Not a joke at all. Why should people who knowingly took on student loans get $50k (or any amount at all) for free? If that $50k number can be justified, then the same justification can be used for giving free money to everyone else!

You don’t like the $50k number? So make it $20 for everyone. That will still make a big difference to many people and will boost the economy.

Debt doesn’t matter in an MMT world anyway. Biden is going to leverage up debt just as the Republicans did for the tax breaks for the wealthy. Count on it. By the time his 4 years are up, USA debt will be $8-10 trillion. He’d be a fool not to do this, just as the Republicans did when they were in control. Tit for tat.

Instead, why not give everyone a $50k education voucher. They can use it to pay off student loans and/or use it for future education costs.

Thanks to njbr for the Brookings article. I updated my post with “5 facts”

DodgeDemon asked about my tuition costs. I added that to my post as well.

Let’s talk about how to actually fix higher education rather than how to waste money.

The problem is not student loans. It is lack of accountability and mismanagement in largely democrat-controlled intuitions (90% plus of faculty and administrators generally). We see the effects in irrelevant curricula and faculty hires, low admissions, standards, etc.

You do not fix systemic failure with a loan bailout. You hold the failing party responsible and reward success. Now, how to do this. If universities were required to be the guarantor for all student loans they accepted, what would happen? Go through the steps…

What about those students who want to study Ancient Aramaic 101, hiring a distinguished professor of Astrology, or offering a degree in Alternative Sexuality, for example? With few job opportunities in these areas, only the best students are accepted. Others might be accepted, if the university can afford it.

You make good points, except your “democrat-controlled” idiocy.

Many educated votes are Democrats, because we have no other choice. At least Democrats have some initiatives that we can support, though some are really bad.

GOP doesn’t stand for anything but corruption and tax breaks for the rich. No plan for the rest of the country whatsoever, just demagoguery. Ironic, since GOP caters to the regular country folk electorate. Conservative values (small gov’t, balanced budget etc..), are just bait, GOP hasn’t done anything in this direction for the last 20 years.

Except academia is ‘liberal/democrat controlled, largely a result of Vietnam, btw.

I was a professor/administrator for 30 years. I saw how the university operated first hand. At times, education verged on brainwashing, albeit usually insidious, sometimes blatant. However, a social/political bias was NEVER absent, whether in faculty hires, tenure decisions, curriculum, student recruitment, etc. Given what I observed, the bias increased significantly during the 30 years. The most affected areas were education and arts/sciences. Then, visual arts and law. Least affected: engineering, business, and medicine.

“Please note the acceleration in 2005. What happened?

The cost of education escalated madly when Bush passed the bankruptcy reform act of 2005 making student debt not dischargeable in bankruptcy.”

So, if you know that the costs and debts are in part due to bad govt policy, it it textbook procedure in common sense that the entity of that bad policy should consider/act to address to make right the wrong it created.

That’s basic and widely accepted.

So debt jubilee most definitely be in the mix of policy considerations to wrong the wrong govt did.

Is a blanket K50 forgiveness the right policy? It’s lazy. I can think of much better.

The simpler answer for college debt is to empower bankruptcy judges to forgive and modify student debt in the same way they do other forms of debt. Also the U.S. needs to undo the The Bankruptcy Abuse Prevention and Consumer Protection Act. There needs to be more scrutiny of for profit schools which prey upon students and take advantage of student loans. Also just like with mortgages the forms need to make it abundantly clear what incomes and payment schedules will be required to pay back the debt. We need to remember that borowers are 17 years old, not eve old eough to vote, drink , smoke or carry some firearms but yet we assume they can shoot themselves in the foot with a poorly chosen student loan

Thanks to Bush’s Bankruptcy Reform Act, judges have no legal basis to do so.

Yes. And Biden was a big supporter, so he would need to reverse himself.

I’ve said it before, but relatively accommodating bankruptcy laws (and a second chance) were one the great things about America, and, in fact, the meaning of the ‘liberty’ text inscribed on the Liberty Bell.

was it really bush or was it lobbyists and the legislature?

The gov’t needs to ensure that Wall Street eats these costs, aka lenders.

Student loan reform should happen, and yes, it’s annoying to those of us who paid off our student loans that some people might get their debt wiped away, but the fed has literally printed trillions of dollars and given it to the Goldman Sachs banker class and I see only a fraction of the handwringing about that wholesale theft.

Two wrongs make a right?

OK. Both sides can play “what aboutism”. What about Fat Donnie from Queens’ destruction of immigration?

What about it?

Trump blocking immigration means the flow of both foreign “free-of-charge” professional brain power is reduced, as well as foreign “ultra low cost farm / hotel / whatever” workers is reduced. Reducing flow of either one is bad for U.S. economy.

Clear now?

Would you support a visa program that would flood our country with foreign university professors, lawyers, and doctors, all allowed to practice without going through an expensive credentialing process, so as to increase competition in those fields and lower the market price? I would. However, I think most democrats would not, as those fields (save the medical field, as far as I know) are disproportionately democratic.

I would support university professors, lawyers, doctors flooding USA from select European countries, France, Germany, UK, Netherlands, Switzerland, Sweden and a few similar ones where brains are highly valued by society / gov’t and whose credentials are likely equivalent or better than US, and also from countries that are not adversarial in nature, e.g. China. Not from 2nd tier countries in Europe or around the world – although could filter by specific universities or degrees. India is a 2nd tier country and there is significant immigration in the medical profession, although it must be followed by an expensive credential process – this is a good thing for medical profession.

Myself I’m in engineering / applied science profession and we have significant immigration in my profession, or alternatively companies just set up an additional design shop in a foreign country – no problem, already implemented for 20+ years in my industry. More than 50% of my design team resides in Asia.

What’s driving the need for degrees ? It is corporations who are making them mandatory. Microsoft is the only company I know that publicly stated they no longer consider degrees mandatory for any job they hire for. The truth is people are not looking at alternatives and want the “college experience”. Most companies don’t even look at if a degree is online or in person or what accreditation it was conferred by. I blame the parents as much as anyone else.

Widening chasm between the rich and the poor. If you’re not making 150k+ now, you’re on the wrong side, and headed south.

Government entities pay far more attention to degrees when hiring than private companies do.

A college degree is routinely required and often when it’s not, there’s a 3-10% “incentive pay” for having it. What they don’t care about: which college, which degree and (sometimes) whether the degree is relevant to the job.

Public position and reality are two different things.

It’s not Microsoft who hires, it’s the engineers and managers who work for Microsoft.

I work for a big tech company in Bay Area, and the resumes of engineers who don’t have an engineering degree don’t even make it my desk for review. We’re looking for smart people not only with degrees (aka proof that you can solve canned academic problems), but also with some experience to do the job, so that we don’t have to digest everything for you for 2 years on the job. While it is true that there are people with excellent engineering skills without a college degree , this is a profession that requires continuous education, and without a college degree you generally don’t stand a chance at learning it. Very few exceptions.

Student loan info

18% owe $5K or less

17% owe $5 to 10K

21% owe $10 to 20K

21% owe $20 to 40K

9% owe $40 to 60K

5% owe $60 to 80K

3% owe $80 to 100K

4% owe $100 to $200K

2% owe $200K+

That is, 86% of borrowers owe less than $60,000.00–and 14% owe more than $60,000.00

Given that a college degree results in a significant life-time advantage in earnings (perhaps $300K for 2 year degree, and $1 million for bachelors over a HS diploma), to what extent should pay-to-play apply?

Seems to me that a $50K forgiveness is a broad stroke solution to a non-problem. A discussion of the cost-benefit of free college is a different issue.

A portion of the debt over $60K is for degrees that will very greatly enhance the recipients future income–should their future wealth be subsidized by everyone else?

I would guess a better solution would be a lending limit based on potential future earnings with the lender at-risk for future defaults on inability to pay.

Why not just allow bankruptcy to clear these… just like any other debt? Let the lenders eat it.

The reason is the debt doesn’t have collateral. You can’t sell the borrowers brains. And everyone would just file for bankruptcy right after they graduate.

But that is no different than other kinds of debt. Credit cards are issued to less credit worthy borrowers. For all kinds of debt, they are truly giving loans based on the ability to pay. You could think of the borrower’s ability to work and the degree. There could be more rules on the loans like, if you change your major after getting a loan, then the loan gets pulled and you have to reapply.

… then maybe the lenders would wise up and stop lending to people that can’t repay.

Exactly. People are really smart when it comes to lending their own money. You don’t need a complex system of lending laws if the government gets out of the marketplace and allows lenders to take losses.

Zardoz, you’re being logical instead of focusing on the law.

During Bush Jr.’s Presidency, they passed legislation preventing exactly what you’re suggesting.

Step 1 is repealing that legislation. Without doing that, all options are either bad, futile or both.

The problem with the government subsidies, bailouts, or guarantees for anything is that the market simply adjusts higher to take advantage of the free taxpayer money. The incentive system is backwards.

Federal taxpayers are the lenders. The loans are federally guaranteed. So we eat the losses if they are forgiven or discharged. This program has distorted the market and caused the price of higher ed to go through the roof.

Stop the federal loans and go private again. They won’t hand out loans for BS degrees and will only concentrate on people that want a real degree and want to work. Too bad the left won’t allow that because they will call it racist………..

Want to see the cost of college drop. Take away the government backing of the loan.

Instead of wiping the debt away drop the backing of the loans that are out. Problem solved

I guess Biden’s Progressive Agenda is Not So Dead on Arrival, eh?

I think he was referring to a legislative agenda. Clearly a President’s EO agenda is on the table during the entire Presidency.

That said, the call on left-wing legislation being dead is premature. Georgia runoffs will determine that. If Dems sweep those, they have 50% + the tie-breaking vote. Can’t afford any defections (Manchin…), but Congressional leadership has consolidated power over the last decade — when it matters, they line up their ducks.

For a good background on student loan debt–see the Brookings link below.

You will note that the highest proportion a big debt amounts is from the students at for-profit schools, which are not public or private universities.

These for-profit schools have high pressure sales that over-promise and under-deliver on post-graduation jobs.

…The Website For Profit U claims that an associates degree awarded at a for-profit college may cost up to four times as much than a similar degree awarded at a comparable public university located in the same region, and bachelor’s degrees cost up to 20% more at for-profit colleges.

Supporters of the for-profit education sector are sure to make the argument that though degrees from for-profit institutions cost the student more, they make up for that differential in costing taxpayers less. This is only partially true. As this study shows by comparing data from the National Center for Education Statistics (NCES.ed.gov) taxpayer costs for an associate degree are almost $4,000 higher per student in the public sector than the for-profit sector. However, the statistics also suggest that the combined costs (student and taxpayer) are approximately $16,000 per student lower at community colleges compared to their for-profit counterparts. This means, on average an associate level degree at for-profit college will cost the student $20,000 more than the same degree earned at a community college. Though on average, still higher than the costs of public colleges and universities, private-nonprofits also cost much less than their for-profit counterparts.

The higher costs associated with for-profit colleges may be justifiable if the degrees earned translated to higher earnings; however, students at for-profit institutions default on their loans at rates staggeringly higher than those of public and private-nonprofit colleges and universities. According to For Profit U, 1 in 5 students (22.7%) from for-profit colleges default on their loans within 3 years of repayment. That is compared to 7.5% of students from private non-profit colleges and 11% of students from public institutions. This statistic could suggest a number of things: perhaps graduates could not find meaningful employment after graduation, or maybe the program didn’t lead to employment that would generate the kind of income the student was promised. Perhaps the higher tuition and fees simply caused the student to take on too great a debt to be reasonably repaid. A number of factors could contribute to this statistic, but one thing is for sure, having substantially higher default rates coupled with substantially higher net costs means the higher cost is not providing greater return on the student’s investment in their education…..

Interesting data

I really don’t understand student loans well. Who holds the debt? The federal gov? The colleges? Banks? I’m hearing people having non-dischargeable loans with %8 interest (How is %8 justified?). If the loan is guaranty by the US how is %8 justified? Is the loan guaranty also for loans to go to private schools? (like Trump university?). So if I was Biden, I push to make college loans dischargeble in BK. I will also only guaranty loans for students going to accredited public colleges. What am I missing?

Private lenders can charge 8%.

Almost all of the debt is held by Sallie Mae bond holders.

Yes, part of the problem is that student loans are still being made, especially to people in grad school or med school, that carry interest rates just as high as rates on student loans were when I was a student in 1980, when prime was 20%….It’s basically government sanctioned loan sharking.

The loans are made by banks and credit unions, but the government guarantees them, so there isn’t any risk to the lenders. No reason why these loans shouldn’t be at 2-3%…..that’s what I refer to as a “conduit scheme”…a scam that benefits the donor class by putting government money in private pockets.

Thanks I suspected that much. To me the solution would be to 1) stop all government guaranty to this loans. 2) Provide state community college education and trade education for free (Public schools only). 3) Target student financial help to needed fields (MD? RN? Long term care? etc). This will probably be less expensive and provide the biggest bang for the money.

…and (4) would be to democratize the credentialing process. So, courses could be taken online, anytime, then tests would be taken at a local testing center (where ID’s are verified). Degrees could be earned this way – as an option to attendance at a brick and mortar.

I forgot….since 2010 the government has become the primary lender now….that came with ACA….just slipped my mind earlier. I wanted to correct what I said. So the government is the creditor for most of the new loans

The Government, via the GSEs, is also the main lender for home loans. The past 11 years they have backed 95 to 98% of all mortgages. That is why they can do forbearance on so many loans. They do not need the money if home owners quit paying. The MBS owners are happy because they keep getting paid even if the home owner is not making payments.

The GSE’s are really the biggest landlord in the U.S. They in a round about way own over 50% of all the houses in the U.S.

Look at the chart. The housing bubble and corresponding recession is when all those non-agency (Bear Sterns) started making loans to all those sub-prime people.

Since you bring up the housing subject. Are all these hoses being bought by investors to rent (Blackrock) or are they truly being bought by people to live in? Is the data broken down somewhere?

This is another unexpected consequence of trying to level the playing field for minorities, imho. A largely misunderstood story that no MSM media would ever touch.

The defaults in 2008 were predominately non-white households who were suckered in by predatory lending practices that were legislated into existence. They were left holding the bag when the no-doc ARM’s they signed went up and the economy tanked.

The only saving grace is that the easy mortgage money has made it easy for somebody like me to greatly increase the size of my real estate portfolio…..I bought at good prices after the sell-off, and I was able to lock in 30 year money at 4.5% which ain’t bad for investment property. Ordinary people always pay at least one point higher for investment money than for personal mortgage money. Black Rock, I ain’t.

I’m hoping to do it again if COVID (eventually) makes RE correct…..Here, it might not, given the juice we’re getting from the demographic shift.

Is it time for a debt jubilee? https://www.patreon.com/posts/is-it-time-for-44658139

https://www.patreon.com/posts/is-it-time-for-44658139

I wish they wouldn’t say forgiving student loans. The debt is just being transferred to taxpayers. The colleges, I assume, will get their money owed almost immediately.

The colleges already have their money.

Just like selling a house, the seller gets their money at the closing, not when the buyer makes payments.

Make the colleges disgorge their past tuition paid for by taxpayers, instead of just stiffing the taxpayers.

It wouldn’t be transferred to taxpayers. It would be paid for by money created by the FED. Effectively, there would just be a bunch of money created that would go into the stock market and/or bond market and the FED balance sheet would get even bigger.

Money printing is effectively a wealth tax. So long as you define wealth as being dollars or things easily transformed to dollars. I dare say most of the actual wealth of the US is in citizens, themselves. So, in effect, money printing lowers the value of valuable people – young people.

Sallie Mae sells tranches of bonds by year and credit risk. Bonds are not individually owned. Rather you own a piece of the entire portfolio for a given calendar year. You can get a higher return at the risk of taking a bigger principal loss and vice versa. I’m not sure how forgiving $50k of debt can work from an administrative perspective. The FED can buy debt, but they can’t buy individual loans. And if the FED isn’t buying the debt, I don’t see any way to finance this.

It should work similar to mortgages. People move/refi and thus prepay all the time – that is one of the risks in holding mortgage backed paper.

I think the better ‘solution’ for existing borrowers would be to reissue the outstanding debt with a fixed rate of 1.25% and a term extension of up to 10 years. For new loans, I think there needs to be a cap on the notional amount that can be lent with any type of government backing.

It’s never been done with mortgages or any other publicly held debt as far as I know.

I guess the government could issue bonds which would be bought by the FED and then the money would pre-pay loans.

Not sure what would happen to the sallie mae bond holders. Would they get a huge one time dividend to cover the loss of principal in the securities? If so, there would be a flood of investment money in other securities.

Sallie originates private loans to people with income that is too high for the Federal programs. Nothing would happen to Sallie or its bonds under these forgiveness plans.

Hi Mish. Please compare cost of your tuition at U if I per credit hour to the present. Is it about 12x to 15x now? Probably worse at private colleges, which can’t use the shop-worn excuse about state funding decreases. Follow the money to the dogs that ain’t barking: the college administration staff. Presidents, Chancellors, Provosts, Deans Of Diversity, Deans Of Bathrooms, Deans Of Coloring Books and Comfort Dogs and so on.

Unpayable student loans should be able to be discharged in bankruptcy court. We could fix that, but we probably won’t, because the donor class doesn’t want it.

In general, I think it’s a bad idea to discharge student debt…but in the short run it would be great for the economy…..talk about a stimulus.

I do think a $50K forgiveness makes more sense than a $10K forgiveness, because it would tend to benefit those who actually completed a degree rather than those who didn’t….and it would put a lot of money in the pockets of young families who are held back from being homes because of student debt.

“buying homes”

The only thing that remotely makes sense to me is to adjust the interest rate down to 1% or even 0% from it’s current level of 10% (or is it 7?). That would help pay down the loan over time because the principal wouldn’t increase. As tax payers all we would lose out on is the interest payment.

Forgiving money not only helps the middle class (as Mish mentions), but it also severely punishes anyone who has paid off their loans. Millions of such people would be rightly clamoring for their money back. Not to mention if this was known ahead of time you can bet millions more will be borrowing as much as possible before the deadline in order to get it all forgiven and net free cash.

Prior to 2010, the government didn’t loan money directly…..that came with ACA. Now most of the new loans are not private, but there is a lot of interest still going to banks, fwiw. It doesn’t all go to the taxpayer.

I don’t see that the government needs to be the lender…..but they need to set interest at low rates. With a federal government guarantee, the banks are not going to lose money.

Think of people who thought about going to college and but chose not to because they did not want to go in debt.

If you are going to forgive 50k in student debt you also need to offer 50k credit to anyone who wants to go to college. Maybe give them 3 years to decide.

Maybe handing out student loans for fake degrees like gender studies should not be allowed. Obama opened the floodgates and gave anyone with a pulse a loan. He knew what would happen when he turned thousands of people into debt slaves. Just look at the ghettos. The democrats are masters of slavery.

That means those students got 50k in free education money. What about those who did pay it off? What about those future students who didn’t get the chance to borrow and have it give to them. Thats 50k of free money the new students don’t get…unless public University is heavily subsidized by 50k. What about those kids who picked private school. They have 300k in debt.

10k vs. 50k. by eliminating 10k you are helping pay off many who have ben paying for years. 50k debt forgiveness is teaching an entire generation you don’t have to be responsible for YOUR actions. Not the schools who are the definition of greed and complete rip off.

10K gets almost ALL real the deadbeats off the books. That would be the main reason to do it.

10k vs. 50k. by eliminating 10k you are helping pay off many who have ben paying for years. 50k debt forgiveness is teaching an entire generation you don’t have to be responsible for YOUR actions. Not the schools who are the definition of greed and complete rip off.