No Clear Skies Yet

Inquiring minds are slogging though the 78-page BIS annual report looking for an all clear signal.

It’s nowhere to be found. The BIS explicitly warns “No clear skies yet”.

Monetary Policy Cannot Be Engine of Growth

Hitting the nail squarely on target, the BIS chastises central banks “What is good for today need not necessarily be good for tomorrow. More fundamentally, monetary policy cannot be the engine of growth.”

Central banks, beg to differ. Markets are going gaga over expected rate cuts while Trump plays a year-long tune of on-again off-again tariff threats.

Overheating

The corporate sector in some countries has shown clear signs of overheating. Perhaps the most visible symptom of potential overheating is the remarkable growth of the leveraged loan market, which has reached some $3 trillion.

For quite some time, credit standards have been deteriorating, supported by buoyant demand as investors have searched for yield. Structured products such as collateralised loan obligations (CLOs) have surged – reminiscent of the steep rise in collateralised debt obligations that amplified the subprime crisis.

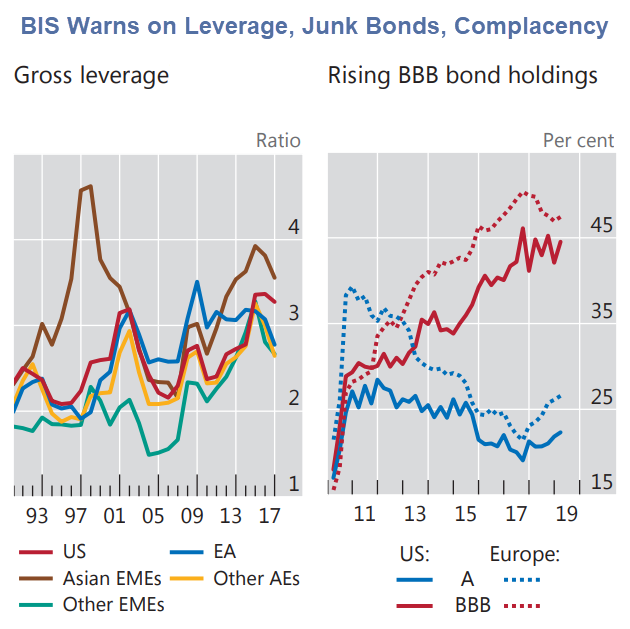

Fire Sale Collapse in Investment Grades

Given widespread investment grade mandates, a further drop in ratings during an economic slowdown could lead investors to shed large amounts of bonds quickly.

As mutual funds and other institutional investors have increased their holdings of lower-rated debt, mark-to-market losses could result in fire sales and reduce credit availability.

The share of bonds with the lowest investment grade rating in investment grade corporate bond mutual fund portfolios has risen, from 22% in Europe and 25% in the United States in 2010 to around 45% in each region

Zombie Corporations

Firms that are unable to cover debt servicing costs from operating profits over an extended period and that have muted growth prospects – so-called zombie firms – have been on average 40% more leveraged than their profitable counterparts.

They sap economy-wide productivity growth not only by being less productive themselves, but also because they crowd out resources available to more productive firms. Evidence suggests that their increase over time has had an economically significant macroeconomic impact.

Bank Profitability

Unfortunately, bank profitability has been lacklustre. In fact, as measured, for instance, by return-on-assets, average profitability across banks in a number of advanced economies is substantially lower than in the early 2000s.

Both macroeconomic and banking-specific factors have sapped bank profitability. On the macro side, persistently low interest rates and low growth reduce profits*.* Compressed term premia depress banks’ interest rate margins from maturity transformation. Low growth curtails new loans and increases the share of non-performing ones. Therefore, should growth decline and interest rates continue to remain low following the pause in monetary policy normalisation, banks’ profitability could come under further pressure.

Moreover, low profitability may also lead to credit misallocation. Less profitable banks are more likely to evergreen loans or lend to zombie firms, thereby crowding out funding for new, more productive ones. In turn, over time, credit misallocation may depress bank profits further, thus setting in motion a vicious cycle.

Monetary Policy Balancing Act

There are diminishing returns and costs in relying too much on monetary policy. Such an overburdening can contribute to the re-emergence of financial vulnerabilities and reduce the room for policy manoeuvre. It becomes natural to ask where the limits to this approach are. Ostensibly, monetary policy cannot be the engine of higher sustainable economic growth. More realistically, it may be better regarded as a backstop.

Structural Reforms and Productivity

The only way to raise long-term growth on a sustainable basis is to implement structural reforms. Indeed, productivity growth has been on a long-term downward trend in advanced economies.

Unfortunately, over the past decade, the momentum in structural reforms has been lost, as the sense of urgency associated with the GFC has faded.

Europe and China

Europe and China are the two arenas most in need of structural reform.

Italy, Greece, and France are basket cases. ECB and EU policies do not help. A Eurozone breakup is but one accident in Italy away from happening.

China is overly dependent on State-Owned-Enterprises (SOEs) and property bubbles as a means of growth.

Trade wars with Trump, capital controls, and lack of property rights contribute to the problems.

US

Trump’s trade wars with the world are a huge negative.

Worse yet, Democrats are in a heated rate to promise more and more “free stuff” as if there really is no cost.

Globally

Globally, central bankers are hell bent on pursuing the same bubble-blowing policies that led two huge economic busts.

This third bubble is the biggest of all but they do not see it. The BIS did not mention it.

Meanwhile, there is no impetus for change anywhere, except in the wrong direction!

Good luck with that.

Mike “Mish” Shedlock

The Fed has become the great enabler. A key role of a reserve currency is to force other currencies to toe the line or pay a stiff price. Ignoring this economic reality translates into pain for those holding the currency of any country that abuses this economic law.

The rapid expansion of debt and credit during the last decade could have occurred without the Fed being totally complicit and in agreement. It has been the Fed that decided to allow the dollar to be used as a global prop.

Trump’s desire to manipulate the dollar lower to boost exports would take the world down a very slippery slope. The article below explores the problems it could cause.

I’m confused. The BIS is an international financial institution which is owned by 60 central banks. Shouldn’t its reports be spouting the great success and heroic economy saving actions by its member central banks?

Instead, why are they issuing reports challenging the veracity of the predominant central bank policies being implemented across the developed economies?

I think someone needs to get with the program or find another job.

nailed it. This one Mish item is the biggest news in 10yrs. What the hell is going on here?????

It all makes gold sound useful, just in case.

“Worse yet, Democrats are in a heated rate[sic] to promise more and more “free stuff” as if there really is no cost.”

That’s because the Fed has monetized it all thus far, so there hasn’t been an (obvious) cost to any of the hand outs! The rise of socialists is entirely predicable because it’s always someone else’s money paying for it!

The biggest handouts recently have been the tax cuts for the richest and corporations – odd nobody seems to ask how that was going to be funded – but try to do something for average Americans and suddenly everybody is shouting about socialism.

Last I checked my bills said “Federal Reserve Note”.

The rise of the socialists was predictable because whatever form of capitalism that is happening now is failing for the vast majority of people. The reason you don’t hear anyone with a lot of money saying anything about the debt or deficits is because they have been the beneficiaries of most of it. There is so much money in such few hands since ww2.

Yeah, if we’ve monetized the wealthy’s gambling losses why can’t we do that with our education, health care, pensions….they will, it’s coming barring some major conflagration

“BIS warns of Diminishing Returns of Monetary Policy”

Pushing on a string.

I trust bond ratings about as much as I trust unemployment and inflation rates. I remember during the Lehman collapse, many companies were investment grade up until they filed bankruptcy.

Structural reforms must mean breaking up monopolistic cartels and a significant increase in real corporate taxes. That’s the only way to push corporate CEOs to actually invest in productivity growth. Without healthy competition and a difficult time increasing marginal profitability, these companies just go into lazy no growth mode.

I agree with you but the problem is what takes the hit in the short-medium term? Workers, who vote. I don’t see major change that doesn’t involve increases in unemployment and more especially in geographies that are in desperate need of the change. They just so happen to be those with already high unemployment.

US could probably achieve necessary changes if the was a Gov with strong enough mandate. More of a problem in the EU where it will help fuel more discontent.

The system is in a cul-de-sac of central bank & central planners making.

I find it hard to believe that US bond rates are this high. In a world were the French 10 year is negative, 2% seems high.

Please don’t take this wrong, negative rates make no economic sense to me. Central banks have ventured into insane policies and the negative impacts of the policies never seem to show up! Japan continues with unsustainable deficits and nothing happens. So what makes it unsustainable?

MMT is coming and I have no idea what it will bring.

The difference is the US supplies way more bonds than France. Our high supply keeps our rates above water.

That and the fact that something has to be a safe haven and still be liquid. The US has the advantage of the being the defacto reserve currency of the world and the currency on which most markets rely on.

…..the FREAK show must go on; the unsustainable cheap debt driven rat race to the bottom, serving sick, Central Banks manipulated capitalism …

I think this is the real cause of the treasury inversion. Negative rates driving up demand for UST and thus driving up prices.

Soaring deficits combined with collapsing tax revenue force US into full blown (Zimbabwian)monetization,gov’t deficits along with soaring costs at hyperinflationary levels will force the fed’s to print like tomorrow never dies sending the country (world)into a hyperinflationary tailspin it won’t get out off!

You and Mish miss the critical move that comes first – the sovereign debt crisis that drives the only-game-in-town dollar much higher. How do you get hyperinflation when there is still demand for US dollars?

Wrong. Bernanke swore that central bankers have tamed inflation for good!

If Bonkers Bernanke said it, it must be true 😉