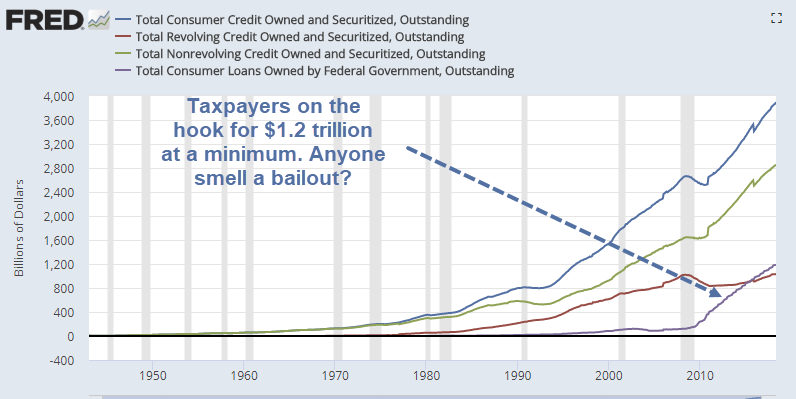

The Fed’s Consumer Credit Report for May shines a bright spotlight on a huge problem.

In May, consumer credit increased at a seasonally adjusted annual rate of 7-1/2 percent. Revolving credit increased at an annual rate of 11-1/2 percent, while non-revolving credit increased at an annual rate of 6-1/4 percent.

To keep consumption up, consumers must borrow more and more. And rates keep going up.

New Auto Loan Rates

Credit Card Rates

What can possibly go wrong here?

Mike “Mish” Shedlock

Mish – you really should go back and look at the total credit outstanding on either a continuously compounded annual basis or log scale. No where near as frightening and if anything, this past decade is less volatile and at the low end of growth.

Consumer sentiment seems to lag reality by about 1/4 or more of the real economic cycle. It takes a while for and expansion to penetrate the general consciousness, but once it does, it takes as long for the realization that the party is over to really hit. We saw this last time round where property peaked in 2006 but the realization came in 2008 when the headlines made reality inescapable.

I suspect we are leveling off at the moment and are in danger of tipping into the next recession, however I always remember Barry Ritholtz (Mish’s favorite, not) admonition that “nobody knows nothing” (I know he didn’t coin this, but the one time I shared a stage with him at an event in NYC in 2010, he reminded us all of it).

Maybe this is related to the low unemployment rate. People get a job and the first thing they do is borrow against future earnings.