The Fed’s Dilemma

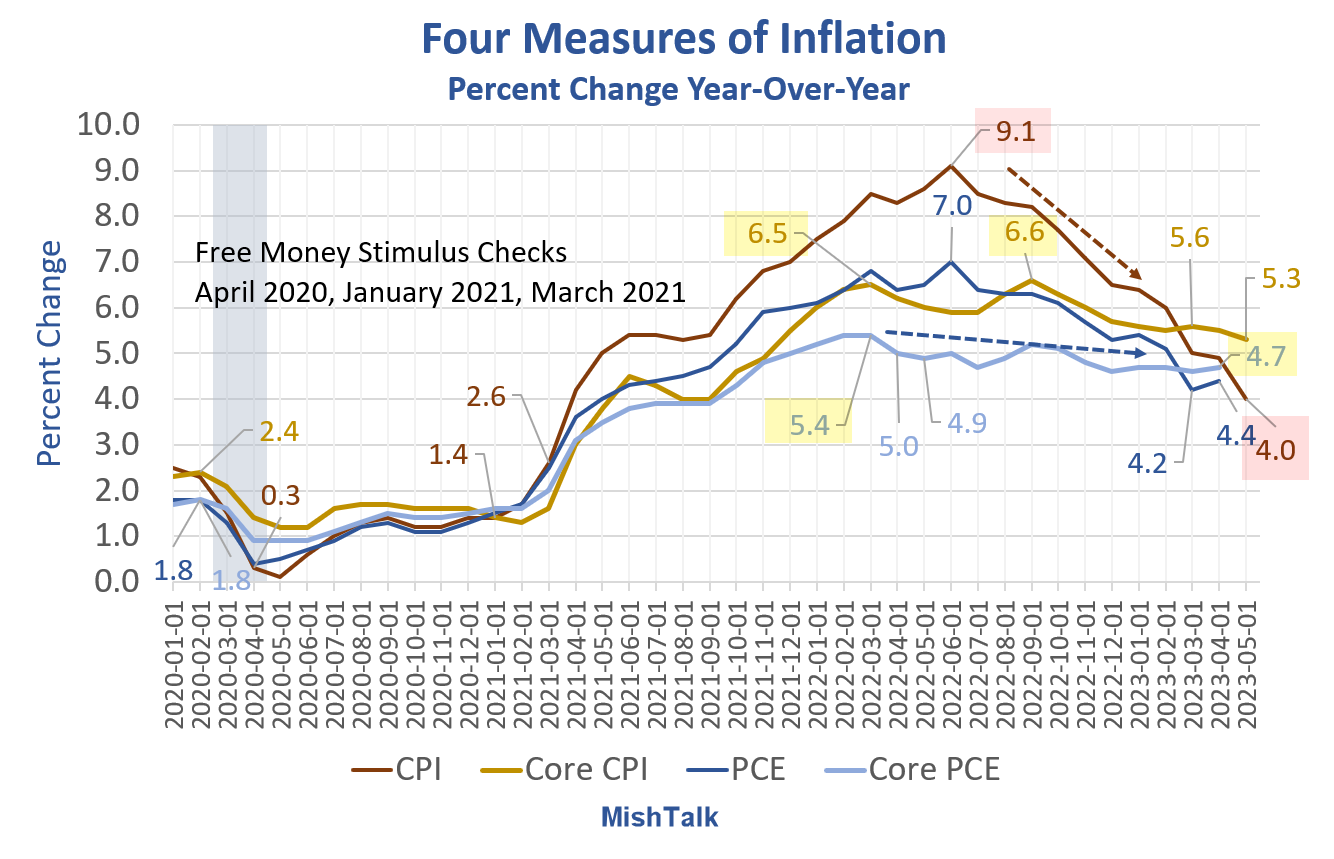

The lead chart shows CPI inflation cooled from 9.1 percent to 4.0 percent. Core CPI inflation, excluding food and energy only decline modestly, from 6.6 percent to 5.3 percent. The Fed’s preferred measure if inflation, PCE, declined only from 5.4 percent to 4.7 percent.

The Fed says it will get PCE inflation down to 2.0 percent. When? How?

Powell’s Post-FOMC Press Conference Statements

Powell: “The risks of overdoing it and underdoing it are getting closer in balance. I still think, and my colleagues agree that the risks to inflation are to the upside. We don’t think we are there. We would like to see credible evidence that inflation is topping out and beginning to come down.”

Chris Rugaber AP: Why signal additional rate hikes? Why not give it more time? It’s surprising to see so much hawkishness in the dots.

Powell: “We are two and a half years into this. Forecasters, including Fed forecasters, have consistently thought inflation was about to turn down, and have been wrong. If you look at core PCE inflation, overall, over the last 6 months, you’re not seeing a lot of progress. It’s running at a level over four-and-a-half percent, far above our target.”

Fed Pencils in Two More Interest Rate Hikes in 2023

The press conference notes are why the Fed Pencils in Two More Interest Rate Hikes in 2023

Regarding Rent

Powell: Rent disinflation is “coming slower than we would have expected.”

Not in this corner.

Rent may easily determine what happens to core inflation.

If rent does not come down significantly and quickly, then the Fed is going to struggle with core inflation. Perhaps rents will stabilize, and a record supply of homes under construction may help the cause, but it is by no means a given.

For discussion, please see Tame CPI Inflation? Not With Shelter Up Another 0.6 Percent

This is not just a US problem.

Why Inflation Around the World Just Won’t Go Away

The Wall Street Journal reports Why Inflation Around the World Just Won’t Go Away

The impact of the past year’s aggressive interest-rate increases seems to be ebbing in places, with signs that housing markets are stabilizing and unemployment is resuming its decline. Growth softened in the eurozone, which has entered a technical recession, but the economic bloc still added nearly a million new jobs in the first three months of the year, while the U.S. economy has recently added some 300,000 jobs a month. Canada, Sweden, Japan and the U.K skirted recessions after growth unexpectedly rebounded. Business surveys suggest a relatively buoyant outlook.

“It’s not an enviable situation that central banks are in,” said Stefan Gerlach, a former deputy governor of Ireland’s central bank. “You could make a major mistake either way.”

That is the Fed’s dilemma. And even if the Fed does get it correct, staying correct will be harder. When recession hits the Fed will be very worried about stoking inflation by cutting rates too soon, too fast.

The Fed has made policy error after policy error, creating a big class of winners (those who owned a home and refinanced near three percent), and a big class of losers (Zoomers and Millennials) looking to buy their first home. Importantly, The Starter Home Is No More, Even in Second Tier Markets

Meanwhile, the stock market bubble continues on in an extremely unbalanced economy.

This post originated on MishTalk.Com.

Thanks for Tuning In!

Note: The migration back to WordPress happened today. There were 5 or 6 days of missing posts. Adding them triggered a slew of emails. Apologies offered.

Mish

[…] Core Inflation is Much Stickier Than the Fed Expected, Now What? […]

[…] Source link […]

I would have thought to get it over and raise .25 at the last meeting. Core numbers were talked about often this spring. Take a pause and if food and energy spike up again, then what? Greedflation going on with business.

Mish – keep up the great reporting.

Christoball – good point – prices are up substantially and will be so regardless of what next month’s increase is. For example, I noted an article that was talking about the large decrease in gasoline prices and therefore the lower inflation over the past 9 months, isn’t this wonderful. . . . But if we look back over three years gasoline prices are up and going higher. This idea that the impact of inflation will disapear is simply not how prices are affecting consumer pocketbooks. So far businesses have been able to increase prices to offset or even more than their costs. That won’t continue.

The Fed will have a difficult time controlling inflation if the Biden administration is going to keep borrowing Trillions for programs like the Inflation Reduction Act and the American Recovery Act. Multi-trillion dollar annual deficits are a real problem, and I would think, unsustainable. But they will still fuel inflation.

Greenspan got rid of the transaction’s concept of money velocity in September 1996 (the G.6 Debit and Deposit Turnover release). Then, the FED’s longest running time series.

https://fraser.stlouisfed.org/files/docs/releases/g6comm/g6_19961023.pdf

Powell destroyed deposit classifications when he eliminated the 6 withdrawal restrictions on savings accounts in April 2020. This didn’t have the same impact as the “time bomb” in 1981 (the widespread introduction of NOW accounts), which propelled N-gDp to 19.9% in the 1st qtr.

But this now allows the smallest savers to hold any temporary surplus cash in an interest-bearing account which can be shifted at little or no cost, and no loss of accumulated income into demand deposits or currency.

Next month, we’ll have FedNow; payment and settlement outside business hours and on holidays, at all participating institutions, speeding up cash flows, and at lower transaction’s costs.

you can pretend inflation in 21st century is different than it has always been in history of currencies and kingdoms, but it’s not. coin clipping in siracusa, sicily during greek empire is no different from the high tech computer generated currency today. the proof is quite simple. is your sawbuck worth what it was 5 or 10 or 100 years ago. the fancy talk and idiocy of deflation is pure poppycock. good for mocking and LOL. and let’s not forget our empire has outsourced the currency creation to the FEDRESNY which is a private company owned by nyc bankers. a real great scam. but no different from ancient scams. in her affect on the people’s purchasing power.

Hi Spencer. The 6 withdrawal restrictions on savings accounts were predatory and parasitic. It affected mostly those with the least reserves. It only applied to online transfers. Anyone could always go into a bank and deplete their savings account in person with no penalty. It was almost like an excessive slumlord late penalty written into a lease. Powell did the right thing.

Money should be defined exclusively in terms of its means-of-payment attributes. The present array of interest-bearing checking accounts has confused the distinction between means-of-payment accounts (the primary money supply) and saving-investment accounts and created a dilemma as to what portion, if any, of these interest-bearing accounts should be considered as savings.

Obviously, no money supply figure standing alone is adequate as a “guidepost” to monetary policy.

Powell was wrong about the money supply. But he was right about M2’s correlation to prices. M2 contains a lot of “gated” deposits. It is not “means-of-payment” money. Money has no significant impact on prices unless it is being exchanged.

But velocity is a problem. The ratio of our transaction deposits to total deposits is rising. I.e., the “demand for money” is falling (velocity rising). People are spending their savings (dis-saving). And credit card debt, as an offset to declining real wages, is still increasing.

Government policy is inflationary and the Fed can’t stop this. Expect Stagflation

Monetary policy is dis-inflationary. Fiscal policy is inflationary. Seems like Powell ought to comment on the ridiculous government spending if he was truly interested in getting inflation under control.

I suspect no matter how high the FED hikes, we’re going to have inflation over their target. US interest rates can isn’t going to have much effect on many imports, food, and other every day necessities. People don’t borrow money for those things. Maybe they put things on a credit card, but, people who can’t pay it off every month won’t care if they’re charged 25% instead of 22%. It impacts housing and auto the most.

I think the FED should just hold steady for a while and see where things go. What will actually happen is once things start going bad in the economy, they’ll start cutting. The FED, like the federal government, is heavily democratic. They want to keep their preferred party in power.

The solution is obvious: change the target inflation rate.

They did pick this one out of thin air.

Why not 7% instead of 2%.

Then they could again complain about not enough inflation.

Of course that would not help improve their credibility.

But their credibility is pretty much shot anyway.

And next year is a Presidential election with a big spike in federal spending to influence the vote. It will be especially large given that the massive foriegn policy debacle (the Ukraine war) that is unfolding. Fiscal policy is pushing inflation and will continue to do so. It’s like a replay of the 70s only worst; with no industrial base a massive $32 Trillion debt and unfunded liabilities out the wazoo.

Biden’s brain trust of Sullivan, Blinken and Nuland have really stepped into it, starting a war with Russia. Beside the tremendous loss of human life and human suffering caused by these evil neoliberal, neocon jerks, this has ended up turning half the world against the US and before it’s all over Europe and the US will want a divorce. The dollars might reign is coming to an end along with the US empire. I wonder what that will do for inflation.

I think two more hikes are necessary to get inflation back to pre-Covid levels. The Fed wasn’t the one that overshot to the downside so much. It was also all the stimulus as many have pointed out. The Fed is kind of trapped here because there is going to be no soft landing where you get the economic growth you want and the inflation you want. We would lucky to get 2% inflation and 1% growth with rates where they are now. A couple of more hikes will be necessary. They also need to crack down on black money which is causing a lot of inflation in all kinds of markets.

I would agree with you, provided those two hikes totaled 7% and the EFFR is held there for a minimum of two years. But the Fed is never going to get there (even by *many* smaller hikes), by design, as that would be too impacting on the Fed member banks profitability and possibly viability as ongoing interests.

Had the Paul Volcker led Fed been as reluctant to reign in inflation as the current bunch I shudder to think of what the cost of living would be today and I am glad to be old as the future of the young Americans today (financially) is going to be brutal.

Inflation is indeed sticky. If May 2023 CPI were calculated triennially instead of year over year it would be 18.59%, stating that prices are 18.59% higher than 3 years ago in May 2020. This represents a .21% rate increase from last months 18.38% triennial CPI rate, but also a whopping 1.69% rate increase from the March 2023 triennial CPI rate of 16.9%. The problem with inflation statistics is that they are represented as simple inflation year over year. In truth inflation is not simple inflation but is compound inflation easily demonstrated by last year being an incredibly high base year. Any current price rate increases are added onto and in addition to already existing high prices. It works in the opposite direction of compound interest which is known to build substantial wealth. Compound inflation creates substantial plunder of wealth.

this is the most important fact about inflation. anyone calling for deflation is really delusional. and greatly confused.

Is post moderation now more aggressive?

Just wondering

No much less aggressive after I approve somone

Three things missing from the new platform.

1. Upvote/downvote button

2. Any discernable threading

3. Floating Home button which helps navigation between articles

4. No comments link, coming to the post requires to scroll down to comments every time

Ads might have gone, but these are serious flaws.

i concur with those points. i’m sure mish will correct.

And no editing.

Not even 5 minutes.

looks better!!! and cleaner!

Rates are still stimulative relative to inflation.

What I find in the real economy is that lending has definitely been impacted by these rates for businesses. We are talking about >10% rates.

That is the dilemma that the FED is in. These rates will take time to affect inflation but will start killing small businesses sooner.

Ads will be back, but not that clickbait garbage at the bottom that made commenting difficult.

No pop-up ads, and hopefully no garbage.

Testing new comments

Testing from home PC

The Fed doesn’t care about 2% inflation or full employment. It serves the interests of the big banks.

If you have the power to create money but it gets debased by too much creation, who cares? You can just create more money. It’s who has the physical assets that matters.

Right now the Fed’s goals are to consolidate the banks to eliminate the small ones so they can proceed with a CBDC.

(btw new site is much much cleaner looking)

“The Fed doesn’t care about 2% inflation or full employment. It serves the interests of the big banks.”

You understand what’s going on. I read so much blather about this Fed mandate or that Fed mandate, but the Fed’s laser focus is all about the Fed member banks and the food chain of those banks. Anything the Fed does beyond that is to maintain the illusion of being a necessary entity for the US as a whole so that they don’t have their charter revoked and can no longer be the fox in charge of the hen house.

BINGO. WINNER. i’m still shocked mish doesn’t get this reality of the FED. i figured this out decades ago. some great historical books on subject. i always chuckle when i walk by the FEDRESNY each week. i hat tip them for a great scam.

Correct. Fed reserve NY is private ownership by nyc banks. Get that clear and one sees reality not the hooey. I doubt mish gets this. Most don’t

Tough position. These rates (which I do not consider very high) need to be held for a long time in order to reset the cost of capital. I think it will take two years for the current rates to work through all the corporate debt-rollover. After all this debt resets, we will know more.

Otherwise, we need more houses, apartments, immigrants and oil wells to bring inflation down.

Correct. 2 years would be fast. Try 5 or 20 years imho.

Inflation will always be a problem until we implement a 50% discount/rebate policy at retail sale and get tough on arbitrary inflationary collusion by commercial agents which is already illegal but not enforced. Libertarian delusion regarding “free” market theory needs to be replaced by a tough pragmatism. Get real.

Agree on the oversimplification problem usually on the part of Libertarians.

Note: The migration back to WordPress happened today. There were 5 or 6 days of missing posts. Adding them triggered a slew of emails.

Apologies offered.

No sweat. No ads. Much better. Any thumbs up for comments

Inflation is cumulative so prices are so high for most things. No where near end in sight

It is assumed that since the labor market is so tight, employers are giving raises that are equal to or greater than the inflation rate

I got a bunch. You’re always interesting.

Why have I suddenly received 20 (TWENTY!) MishTalk post by email within a span of minutes?

Note: The migration back to WordPress happened today. There were 5 or 6 days of missing posts. Adding them triggered a slew of emails. Apologies offered.

Mish