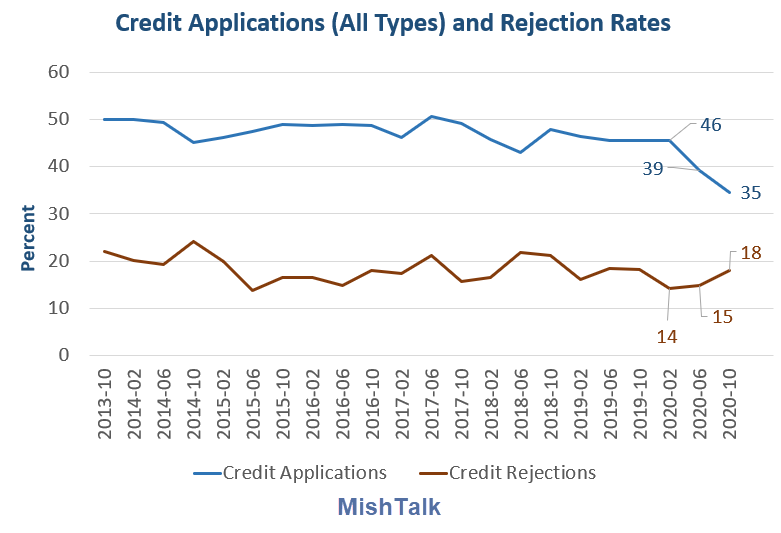

Credit Access Largely Down during the Pandemic

The New York Fed Credit Survey shows credit applications are mostly lower with rejections higher.

- The October 2020 survey shows most credit application and acceptance rates falling sharply with the onset of the coronavirus pandemic.

- Application and acceptance rates for credit cards and credit limit increases showed the largest declines since February 2020, followed by auto loans.

- However, the application rate for mortgage refinancing continued to climb through 2020, driven by demand from borrowers with high credit scores (above 760).

Credit Card Application and Rejection Rates

Credit Card Limit Increase Requests and Rejection Rates

Auto Loan Requests and Rejection Rates

Home Loan Requests and Rejection Rates

Mortgage Refi Requests and Rejection Rates

Standout Records

- The credit card application rejection rate is a record 21%.

- The credit card limit increase rejection rate is 37%. The record high level is 38% hit in June and also in 2014.

- The mortgage refinance rejection rates is a record low 6%.

If you want to pad your credit card to pay the bills, there is a very good chance you cannot do do.

But if you own a house and are current on your mortgage, hooray.

Mish

The credit card limit increase rejection rate is 37%. The record high level is 38% hit in June and also in 2014.

Max out the credit cards on Pb, Au, Ag.

Application rates were trending lower, and rejection rates higher, a year before COVID hit. All COVID did was amplify the trend.

banks always cut back on credit after they see problems with their portfolio and borrwers often mistake an LOC for a rainy day fund until they find the back cut them off due to a change in the banks risk exposue apetitte

Throughout the early part of my career bank credit for many things (especially real estate) was very difficult to get (more so for self-employed folks) and interest was pretty onerous.

That was just after the S&L crisis.

My practice equipment was originally financed at a floating NY prime plus 2 rate. The rate was only locked and the loan was only guaranteed for 180 days at a time….It went like that for several years.

I was paying in the 12.5% range on a principal of about 100K amortized (if I remember correctly) over 20 years. It cut into my lifestyle, for sure.

Every six months I had to submit a full set of new docs. In those days there were no computers and no banking apps and no online anything. No internet. I was in practice for maybe 5 years before we got our first DOS software…which still runs fine, fwiw…with no updates ever. ( I do have more modern software now, lol.)

Every time I had to meet my banker and refi, I spent hours and hours on the financial statements..I didn’t have enough money to pay an accountant to all that.

Once, a few days after such a meeting I asked for a copy of one of the docs……and they didn’t have them.

That’s the day I figured out that they went right in the trash the day of our meeting. It was all just bullshit to make me jump through hoops.

My credit score has continued to go up, just because I make my payments more or less on time (aka no 30 day lates)…..

Seems to me like the cut-off for an “excellent” credit rating has nudged higher over the past few years. . I remember when the best mortgage rates could be gotten with a 720 score, and when I checked my rating a couple of years ago…..they called it excellent above 740.

Now (on Credit Karma) they’re calling it excellent on Transunion and Equifax if it’s above 750. I see you’re calling for 760.

I need to refi everything I own…..but I sure don’t want the hassle.

But I have to do the numbers and see how much it might help and whether it’s worth it to go through the process. Hopefully I can do all the mortgages with one app process…

It has gotten somewhat easier because everything is available online…..the months of banks statements, my tax returns, the info needed for a fresh cash flow statement and statement of net worth….hopefully I can farm so me of that out to my daughter, who is much better than I am at rounding up the data.

They always, always, always ask for everything at least twice, and no matter how much info they have, the underwriter wants to justify his job by asking for a few more details.

Mine bounces around between 730 and 740. I think the only thing changing is how much I have on my credit card I pay off each month. Apparently, to Be Excellent, one must be in debt. It irritates me, and it irritates me that it irritates me.

My credit rating is over 800, but I did have one credit card issuer reduce a credit limit from $30,000 to $10,000 back in March. I rarely go over $2,000 in charges, and always pay it in full, so that’s not a problem to me, but it was obvious that the issuer was worried that small businesses would tap into credit cards to stay in business, and then be unable to pay them back. I suspect that this was fairly widespread.

I retired at 56 and have been debt free for years before. I know debt very well because it was integral to my job. When I retired I didn’t want to be bothered with it on a personal basis . It’s a distraction I didn’t want or need.

The numbers of people today that can retire that young and never have to touch the principal on their investments is a pretty small number, I would guess.

I’m guessing you still actively manage your portfolio, but if you don’t have to worry about money, ever, then you’re one of the fortunate winners in the system.

With a big enough nest egg. you can live off meager bank interest…..but most of us have to get a better return. Some people are financially very competent….no doubt you are one of those…..

Until such time as my net worth can be measured in enough cash to live out my remaining days with that 1-2% return before inflation and not deplete my nest egg…which is probably never..I can see some benefit to using modest debt leverage, at least to buy real estate.