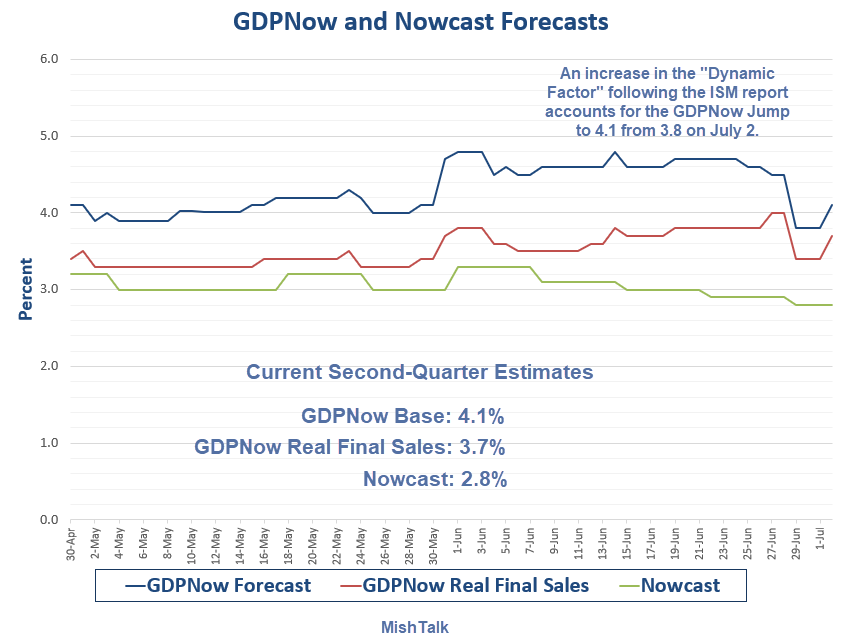

GDPNow Latest Forecast: 4.1% – July 2, 2018

The July 2, GDPNow Release contains these statements.

- After this morning’s construction spending report from the U.S. Census Bureau, the nowcast of second-quarter real government spending growth increased from 0.8 percent to 1.6 percent, while the nowcast of second-quarter real nonresidential structures investment growth decreased from 7.6 percent to 5.3 percent.

- The nowcasts of second-quarter real consumer spending growth and second-quarter real nonresidential equipment investment growth increased from 2.7 percent and 4.0 percent, respectively, to 2.9 percent and 4.8 percent, respectively, after this morning’s Manufacturing ISM Report On Business from the Institute for Supply Management.

- The model’s estimate of the dynamic factor for June—normalized to have mean 0 and standard deviation 1 and used to forecast the yet-to-be released monthly GDP source data—increased from 0.15 to 0.77 after the ISM report this morning.

It is unclear if construction spending added or subtracted from the model. the government forecast rose but nonresidential investment component sank.

I read the construction report as decidedly negative. The statements on ISM and the dynamic factor caught my eye.

Email Exchange

Mish: Hi Pat, Did the dynamic factor increase today’s jump?

Pat: Hi Mish, If the GDPNow program just uses data before July 2, including June data from releases before July 2 [e.g. topline series from the Consumer Sentiment, Consumer Confidence and Philadelphia Fed Business Outlook surveys] the June value of the factor is only revised up from 0.15 to 0.30 as opposed to the upward revision from 0.15 to 0.77 used for the published upward revision to GDPNow on July 2. So it’s fair to say that data from the ISM Manufacturing played an important role in yesterday’s upward revision to the June value of GDPNow’s dynamic factor.

Mish: Thanks Pat, Is there a general description of what makes the dynamic factor rise or fall?

Pat: Hi Mish, there isn’t a description. Since the dynamic factor is estimated with the Kalman filter+smoother, the dynamic factor is revised in the same way an unknown state variable is revised in a state-space system estimated with the Kalman filter+smoother. Just before the time of the release of a particular data series, the current value of the factor is used to forecast the value of the particular series. If the series comes in stronger (weaker) than the state space system expected, the factor is revised up (down). The magnitude of the revision to the dynamic factor depends on the size of the forecast error and how important the series is [measured by the “Kalman gain”]. The situation is more complicated if multiple observed data series are released simultaneously, but the same idea can be generalized.

I cannot claim that I understand that entirely. I suggest this synopsis: The ISM report came in stronger than expected, thereby boosting the prediction of what the GDPNow model expects will happen in hard data reports to come.

There you have it. ISM, a soft data factor, boosted the GDPNow forecast. Whether hard data follows is unknown.

Economic Assessment

What we do understand, from anecdotes, is industries are scrambling to avoid Trump tariffs.

Such a boost, if it happens, will be taken back in the third quarter. The bond market is not at all concerned over the alleged inflationary impacts of the tariffs.

For discussion, please see Bond Market Disagrees With Fed Economic Assessment: So Do I.

Mike “Mish” Shedlock

I suspect “The Realist” will be shaking his head in amazement.

“The situation is more complicated if multiple observed data series are released simultaneously, but the same idea can be generalized.” This more complicated situation happened on July 2 – with two economic reports at once.

Holly cow! After seasonal adjustments, dynamic factoring and the Kalman filter+smoother(???), what the hell does this number tell us anyway.