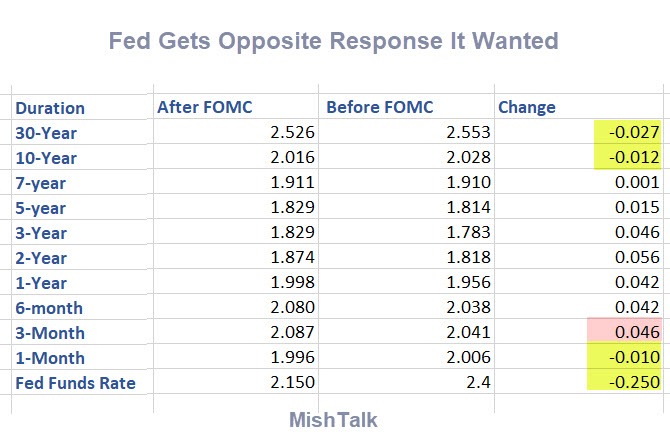

In its policy decision today, the Fed was hoping to steepen the long end of the yield curve. The opposite happened as rates at the long end fell.

Note: The Effective Fed Funds rate will not be available until tomorrow. I estimate it to be 2.15 % down from 2.40% yesterday.

Interest Rate Spreads After the FOMC Announcement

Arrows indicate inversions.

In the following chart, I pay particular attention to the inversion between the 10-year note and the 3-month note.

Interest Rate Spreads Prior to FOMC Announcement

The spread between the 10-year note and the 3-month bill was a mere -1.3 basis points ahead of the announcement. It is now -7.1 basis points.

So much for the notion a rate cut would steepen the curve.

Yield Curve Following Decision

Following the decision the Rate Cut Odds Shrank Dramatically.

I don’t buy it. This is a recessionary reaction.

Expect more cuts than are priced in.

The bond market does not believe Powell’s “Mid-Cycle” Adjustment speech following the announcement and neither do I.

Mike “Mish” Shedlock

Since February, Powell had been draining the Fed balance sheet by $120 billion per month. He casually mentioned that he’s going to stop doing that two months earlier than he’d planned.

If he now puts that quarter Trillion dollar swing to buying down the short end of the curve, it may end the inversion. It’s a significant loosening in any case, but does nothing to deal with the currency race to the bottom now underway.

I think he’s afraid to talk publicly about his real problem, that his hopes of getting the Fed’s balance sheet back in order before the next financial markets debacle has been dashed on populist political rocks as central banks rush to under-run the dollar.

All signs point to the world being in a big fat capital destruction phase. Disappearing interest rates simply reflect that reality. No one can force them to go up, short of destroying the underlying currency. Interest rates will go up when there is real growth again … good luck with that being any decade soon. Too many people want to consume existing wealth (usually someone else’s) before it can be replaced. So that is exactly what is happening.

World economy slows down which prompts large scale buying of ‘safe’ bonds

demand for bonds is such that yield drop, then turn negative

Negative rate bonds become more common place, so that even junk rated bonds start to have a negative yield

Many of the purchases are by ‘forced’ buyers, such as pension funds, who have a mandate to buy ‘safe’ bonds

BUT, negative yielding bonds means over time, the principal is reduced (or in the case of junk probably lost entirely), so pension funds gradually have less and less money to pay out what was promised.

Either you are forced to raise more from new investors (hiking insurance premiums, more taxation) or you reduce pay-outs for existing pensioners/investors

this is deflationary as it takes money out of circulation

this forces central banks to ease even more in order to create inflation, but lack of good investments takes you back to point 1

Have I got this right? If we are in a vicious cycle of central banks attempting to force inflation vs the behaviour or markets, what is the outcome here? If gold is being priced in tandem with negative yields, what will happen if yields ever revert to ‘normal’? What will it take for yields to go back to normal?

What does a sane investor do in this insane environment?

The markets were expecting a 0.5 cut, so when they only got 0.25, it was viewed as a 0.25 hike. Forward guidance didn’t help either.

They priced in a 0.5 cut, but they had to know they were not getting that, many even thought the Fed would refuse to cut at all at this point. But, Powell caved and will cave again, he has no choice, there will be a liquidity crisis before Halloween if they do not go NIRP (well more NIRP than we already are).

and neither did the stock markets…

If the economy can’t run on ± 2.5% interest rates, the problem is not the interest rates. But looking for short-term “juice” is easier than peering into underlying problems in the real economy.

Nominal interest rates are meaningless, real interest rates are all that count. Because business cannot function (their function is to profit) doing their normal production when you have negative rates in real terms, and if you count any measure of REAL inflation we are and have been in contraction with negative rates.

HA HA!!

The Fed’s new mandate is to keep interest rates as low as possible to allow Congress to keep spending money it will never pay back, while keeping rates high enough to attract suckers… I mean patriotic suckers… to keep playing along for awhile.

Everything turned out EXACTLY as planned.

Unfortunately, the money center banks are still zombies, still have no profitable business model, and will not be able to prop up Congressional spending.

Ditto Deutche Bank propping up Germany and the EU…

Ditto Sumitomo propping up Japan…

Pretty much the story all over the G7, we are seeing the same thing. Piles of empty political promises that were never funded and cannot be paid — ergo they won’t be paid.

Actually, the Fed’s one mandate till recent years was a stable currency. Congress and other politicians slowly evolved a second and usually incomparable unofficial mandate of maximum employment. Now, since 2008 they have a mandate that overrides the first two, keeping your debit/credit cards working and the investor class owning 80+ percent of all assets.

HA HA!!!

Saying the Fed has a new mandate was a joke. Poking fun at the failure of central planning. I thought I indicated it was a joke when I wrote “HA HA!!!” in capital letters.

But the stench of central planning failure is all over the G7, not just the USA. That is not a joke, and really not funny

No argument there. I just wonder what will replace it when it all goes up in flames. If it is to be a crypto type credit scheme it will be even more vulnerable to manipulation and unfairness to the masses. Easier to skim than even current fiat. At least dollars (FRNs) are legal tender and do on some level represent a claim on assets, somewhere, even if that claim is a filmy illusion. Crypto is not even that much. Billions of people can’t survive no less thrive in a barter economy, PMs are just too rare to be divided that many ways, they would have to be held in a central place and some scrip representing part value would have to be used as money, that would be a disaster for people/nations that have no ability to mine PMs. We can’t run the world economy based upon shares of mining stocks. Just thinking out loud here.

At least we agree though that the current paradigm is reaching the failure point to such a degree that it cannot simply hold a jubilee and start over identically from scratch.

technical question: if gold is rising in tandem with negative yielding bonds, what happens if bonds start to behave more normally and yields normalise?

Japan has been limping along for 30 years now. Every year, a Wall Street analyst tells us to invest, this is gonna be Japan’s year! But Japan’s economy remains stuck. At one point, they had a nuclear reactor meltdown. But otherwise, its been like the movie ground hog day — over and over and over again.

Japan is broke, and they started QE/ZIRP with a lot more savings than the US or Europe.

Uncle Sam is broke, and cannot afford to normalize interest rates. We won’t have normal interest rates again until after Congress cancels social security “benefits” for at least 70% of the population (30% is what they can afford to pay, so that is what they will pay. politics just decides which 30% gets to keep theirs and which 70% does not).

Gold is heavy and tough to lug around when one is 70+ years old

When bankers refuse to measure or report or recognize inflation because it tampers with their monetary policies does that mean there is no inflation for the people living there?

Tokyo apartments:

The average size for a brand new apartment in 2017 was 63.24 sqm (680 sq.ft), and 60.11 sqm (647 sq.ft) for an existing apartment. The average price of a new apartment across greater Tokyo was 877,000 Yen/sqm, up 5.7% from 2016 and up 43.4% from the bottom in 2010. Mar 14, 2018

I know that my own experience in Oregon is that inflation since 2013/14 lease period is double digit, though I do recognize some of that is regional, and all such reports are anecdotal. That does not make them untrue, for all I know it could be even worse elsewhere. For example, rents here are double what they were just 5-6 years ago, food is up at least 40% and I think a lot of that increase is because they used to post their prices and then you paid really a lot less using your rewards cards, but those sale prices are now mostly gone, the overall impact is a far higher grocery bill, the difference is we pay more than we did and that is inflation. The reason this has happened was that the idea of a major club card reduction was a marketing tool, they were still making a profit, but because prices have risen so much that marketing tool is no longer valid, they no longer make enough profit to use it. My auto insurance is up in the 200-300% range though it would take hedonic adjustments to say really how much because I insured a 2013 BMW worth $57,000 then for $60 per month, and now the same car is worth about $15k so I am insuring a lot less vehicle and the monthly cost in January was $202. Same driving record (clear) now over 60 as of 2018. So much for your rate going down when you get older.

Even the much touted deflation in electronics is mostly hype, I paid $400 for my iPhone 6 and a new iPhone X is over $1,000. The BLS has backed out all of that increase and then some as a hedonic adjustment but the fact is a new phone is still more than double what it was just 5 years ago.

By the way, my cost of living adjustments since 2010 have totaled 8.6% on my fixed income, so less than a compounded 0.08% I am gifted to battle this inflation. The result is that if we do not get a reasonable raise soon I will be living in that old BMW even though my total income is very near median.

And Bernanke / Yellen are the central economic planners who observed the mess of QE / ZIRP made of Japan, and opted to emulate it here.

Time magazine claimed Bernanke man of the year and savior of all the things he screwed up in the first place.

… It wasn’t me !

I do not blame the banksters, though they are a large part of why the BLS has abandoned honest measuring and reporting of the CPI.

The Fed does not even use that weakened watered down version of inflation data anyway. The use the PCE, or did till that also failed to justify their monetary insanity, then they switched to core PCE.

The Fed is fully capable of ordering the federal government (BLS) to deliver a moderate to low headline inflation stat so they can get away with the trillions and trillions in QE and NIRP (REAL INTEREST rates are still negative). The federal government could choose to tell the Fed to go to hell, but that would not support their fiscal policy, not to mention the towering $22 trillion in debt they have to service based upon the Fed’s interest rate policy decisions. Negative real rates means the federal government is making money by borrowing just as corporations do. If the Fed wanted to they could blackmail the government simply by threatening to raise rates that would A) slaughter the employment numbers and B) create a debt service emergency that would mean the government could not borrow just as stimulus is needed most.

In this manner a lot of the most important decisions in government are actually dictates of the Federal Reserve. The ECB runs Europe from bureaucratic offices in Frankfurt and we all know it, it is just a polite fiction that our government is not in the same boat. But, as long as the Fed policy dovetails with fiscal policy of insane spending while not raising taxes trust me, the pigs in DC will be all for it.

False. The Clinton appointed “Boskin Commission” (named for Mike Boskin, Clinton’s appointee) was the government committee formed to water CPI down to meaningless dribble.

Go ahead and blame bankers for what bankers did, but you make a fool of yourself when you blame them for what government did

As Bernanke said several years ago, there will be no “normalization” in our lifetimes. There is just WAY too much debt out there.

Deflation may well be just around the corner (like prosperity was in the 30’s) but for the last several years there has been wild money/debt printing and that is inflation… the expansion of the monetary base is one important definition of inflation. The fact that they get away with discounting this is that the USA as reserve currency has been able to export inflation. That does not mean that we mere peons have not seen prices for goods and services rise, albeit unevenly over regions, and fluctuating up and down with the trend lines being more up than down.

What I have been saying is that for many years now the most basic monthly expenses in my household budget have been on a near hyperinflationary tear, we are not talking about opera tickets or yacht maintenance here, but all four of the four largest monthly expenses in my household budget are easily at double digits and have been since about 2013/14. Rent most notably has risen from about 700 bucks then to 1,300 now. That is a 600 dollar increase for a guy on a fixed income that has had to cut that much out of other spending, even as I have had 8.6% COLA increases sine 2010.

As you can see this just is not sustainable, we can only spend what we are paid or can borrow and I say unless the Fed starts mailing out checks to tens of millions of us we are over our limit as it is. Fortunately for me I am almost debt free, but how angry will I get when they announce a jubilee and wipe away some or all debts? The responsible people are going to realize they should have been spending like everyone else, as if they were drunk online at Amazon with someone else’s unlimited credit cards.

The problem is that Mish is right, deflation must come, even if it is disguised as inflation, because an economy can be made to look like there is inflation via money printing and lying about GDP, unemployment and other metrics of economics. But even as the price of some things appear to rise all they really do is slaughter the real economy by killing sales. See? I mean that if you have Z number of home sales, or car sales or whatever and the total dollar value of those sales divided by the number will equal the average. Price rises and rises and rises even as sales fall because there is a steady or falling amount of cash/credit by the public to buy. On paper they present this as a healthy marketplace because dollar revenue from business is growing. Even though the number of customers is falling. But eventually the day comes when the number of people to keep the consumer economy afloat will arrive that will be too small to keep expanding. I believe that day came in 2007/08/09. They have papered over the crisis with towering new debt channeled into Wall Street and investor class hands so the headlines look great. But in reality every day more people are going without, homes, or food, or luxuries, vacations, insurance. The prices will have to drop or we will have a socialist revolution when that number becomes large enough and it is getting close. Businesses might be able to issue earnings beats but only by lowering their estimates of earnings in advance and by cutting jobs as well as raising prices. And with negative real rates they borrow heavily to do stock buybacks that keep their share prices up even though their balance sheets are a nightmare. In the meantime the number of sales declines. They will eventually go out of business, or be bought and cannibalized, another way of saying the same thing. Example, Linens and Things gone from our malls replaced by Bed Bath and Beyond, now also rumored to be skating very close to bankruptcy. Sears gone, now JC Penney is serious trouble. Toys R Us gone, with no replacement. Walden Books history with Barnes and Noble in deep caca. The money we used to spend there is now going for what used to cost us hundreds per month less than today. Meaning we have been inflated out of those items and had to reduce our own personal economies. Multiply that by more than half the households in the country and you have a very serious problem that will eventually mean either they mail out stimulus checks to the population (devalue the dollar) or they will have to lower prices by extinguishing money, meaning debt defaults. They have made clear that they will not allow deflationary defaults. That means they will try devaluation and stimulus, though they will give to the wider public as little as they can get away with.

But no matter how you look at it we are deflating in the long run, just that one way they can lie and distort the headlines to their benefit, even as the economy in reality is shrinking fast, as long as GDP keeps rising they will claim victory. Even as YOU are out of a job and lowering your standards of living to near starvation.

Think about it, $20.50 trillion was the final number for 2018. Divide by the population and see that per capita GDP rose even though our standards of living are falling and there are firms going out of business. By the way, to save you math time that is well over $62k per person, a household of 3 would be over $186,000 per year if it were divided equally. Median household income is 61k. So the financialized world is scalping labor for 2/3 of their production. And then you pay tax on the remainder.

The only way a shrinking real economy can look like it is growing is through inflation that is not being reported honestly, the GDP is supposed to use a deflator to overcome the inflation that gives a false GDP reading. If we are constantly looking for ways to pay our bills by cutting out more and more items and yet we are still seeing 100% of income going to just staying alive then (Inability to save) even as business fails on a massive scale, then we are being lied to. Inequality has reached the point of no return, we will have deflation AND business failures on a scale never seen before. I am not a prepper, I can barely afford to survive today no less prep for tomorrow. But, it is worth considering for those that can do it.