Congrats to Jim Bianco for outright predicting this headline: Federal Reserve Cuts Rates by Half Percentage Point

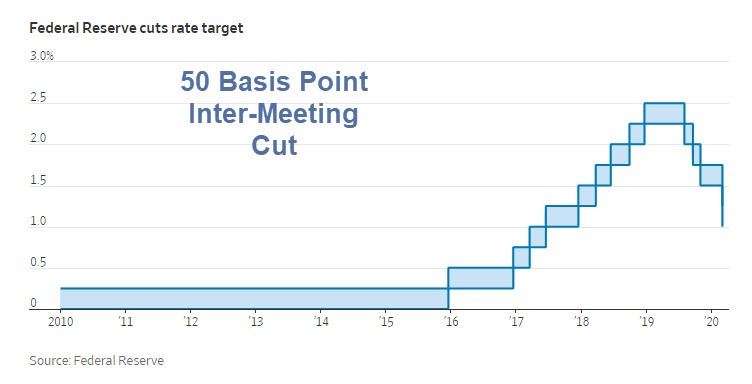

The Federal Reserve cut its benchmark rate by a half percentage point on Tuesday morning, delivering a booster shot to stem potential economic disruptions from the spreading coronavirus epidemic with its first between-meeting move since the financial crisis.

Tuesday’s cut lowered the federal-funds rate to a range between 1% and 1.25%.

Fed Chairman Jerome Powell at a press conference following the rate cut said the central bank “judged that the risks to the U.S. outlook have changed materially” and that the Fed “can and will do our part, however, to keep the U.S. economy strong as we meet this challenge.”

“We do recognize a rate cut will not reduce the rate of infection, it won’t fix a broken supply chain. We get that,” Mr. Powell said. “But we do believe that our action will provide a meaningful boost to the economy. More specifically, it will support accommodative financial conditions and avoid a tightening of financial conditions which can weigh on activity and will help boost household and business confidence.”

Trump Complaining

On Sunday, I commented Market Expects Emergency Rate Cut by the Fed on Monday Morning

Apologies offered. It was Tuesday morning.

Congrats to Jim Bianco who outright predicted this.

I few weeks ago I suggested the Fed was likely to do this but Bianco confidently predicted they would.

As noted yesterday, a Global Recession Now Baked in the Cake

Mike “Mish” Shedlock

12 years ago loose fiscal policy rotted out the middle class and popped the feds bubble….This year the fed met sharper needle.

This doesn’t leave much room for further rate-cutting before it becomes negative; what would the effects be if the interest rate became negative?

People can’t run up their credit cards buying crap that China hasn’t produced. Good for the fat cats though… they can borrow for free and scoop up assets.

Why this is worrisome to markets–if you read SA or other sites there are a significant number of people who still think that CV is nothing to worry about.

A 1/2 point cut with a call for more says”something to really worry about”.

No reassurance in this action, and way too soon.

Shooting the big guns when everyone knows we are using one of the few remaining shells–a big sign of trouble ahead.

And the cut today just alerted the people who think lower rates reflexively goose the market that that isn’t necessarily so.

Proof that from the point of view of a hammer, everything looks like a nail.

I remember Powell’s comments from Fed meeting minutes during Zirp-infinitum. His position was that the Fed should get out of the business of being Wall St.’s lapdog, “It’ll never be enough for Wall. St.; “Even 4.3 Trillion won’t be enough.”

He was obviously right, and to see him now cave this quickly and ‘go for two’ two weeks early is ominous, I think.

Well I guess you can take comfort in the fact that it’ll probably take 500bp+ to “save” the economy from this mess, but the Fed now only has 100bp to work with before they effectively lose authority.

And this clearly wasn’t leaked to anyone yesterday.

Probably leaked Friday to the insiders who bought at the end of the day. Monday was a Fed travel day (and reason Mish’s timing was off by a day). Insiders sold Monday when 2nd tier insiders were alerted to the upcoming rate cut and started buying while smart insiders were selling. Slow pokes today who were kicking themselves yesterday for not buying last week are now saying “will maybe I ain’t so dumb after all!”

Get ready for $2 TRILLION deficits and unlimited debt monetization.

That is the Keynesian “endgame”, and we are now in it.

The global currency crisis that Mish has said “is on deck”, is now walking to the batter’s box.

Don’t look at me; I did not vote for the guy that thought a trade war was going to make America great again. Nice to see his definition of greeat again is America circa 1934.

Lebanon has been in difficulty for a while, but decided to default today on Eurobonds.

50 bps will help housing

That’s great. While I’m coughing up blood, I’ll be re-assured that my home value is holding up.

Housing is in severe overcapacity after being severely pumped for the past 20-30 years. Asset classes in severe overcapacity cannot be helped by rate cuts. The ratio of housing to the population has never been higher. Just because rates are cut does not mean that lenders will actually have access to low-cost credit to make loans with, especially in an environment in which equity financing will become increasingly expensive.

What’s going on here is classic 1930s; interest rates were low, but hardly anybody was credit-worthy.

The dollars looking very wobbly!

Lots of demand for the dollar, there’s gotta be at least $50T of USD$ obligations that have to be repaid with USD$.

As I said in my previous post, the 1930s is the model here, and if you look at what the USD$ did then…

There’s a lot of dollar assets that could be sold as well.

Wasn’t the dollar backed by gold in the 1930s. Today it’s printed at will.

I don’t know.

I think we’re entering the “crisis takes forever … and a day to arrive. Then all at once” phase.

The system is (imo) very fragile / brittle and “events” will swamp policy maneuvers leading to a cascade of (negative) outcomes.

This will not translate to a 1:1 reduction in rates, and we are close to the bottom of how low the mortgage routes will go.

Increasing bankruptcy will decrease the price of houses from now on, the fed rate effect is having its last hurrah.

Yes, 50bp will help housing, but it’s only one of many things affecting housing. If everyone is staying home to avoid exposure, they won’t be buying housing. If the death rate from Coronavirus becomes significant, that will free up some existing housing to be sold. If people are laid off because their company has no demand, or has a problem where they need intermediate parts, that decreases the pool of people interested in buying housing. It remains to be seen which of these factors are the most significant.

If lower rates “helped” housing, there wouldn’t be homeless people around, given the rates which has prevailed over the past decade.

The notion that arbitrary mispricing of things help anything real at all, aside from helping idle beneficiaries of crass theft to steal more, is too silly to even give the time of day.

What “helps” every single facet of every single economy; on earth, in the universe, and in any theoretically possible other universe; is proper price discovery. Not arbitrary theft.

So there’s potentially 2 arguments here; raising rates might liberate some of that hoarded supply. Or collapsing prices due to oversupply may cause dishoarding of excess RE as owners seek to unload before their losses are even more severe.

I’m not sure which one prevails, but I know that policy that has pumped housing investment to the exclusion of most other kinds of investment has been extremely destructive to the “real” economy. And has unduly enriched the “Wall Street” lending community. Factories replaced with mortgage brokerage cube farms. Absolutely disgusting!

As I pointed out previously, this is the classic “you can’t push on a string” example from the 1930’s. When primary demand is destroyed, you can’t make it re-appear with rate cuts. Yes, now you can get lower rate deals on car loans, appliances, and homes, but will those make you more apt to buy when what you really would like to buy is an N95 mask?

This won’t significantly increase primary demand, but it does make is clear that this is a major inflection point.

Yup. Rates were very low in the 1930s, but because asset prices had collapsed, nobody was creditworthy. The only asset class that really saw appreciation was gold (and its miners). The owners of the gold miners enjoying 100X gains relative to the stock market.

In 1977, Nasdaq and the XAU (gold miners) index were both 100.

The Nasdaq peaked out at what, 10k or so? XAU is still 100 43 years later.

Could be an interesting reversion….

It will also drive the prices of those items up but it won’t count as inflation. This makes it unaffordable to those on the bottom of the food chain and hence the popularity of communiism.

Actually, no, the example I gave is the prime scenario for spiraling deflation. Stores have no customers, so they cut prices. Some fail, and default on leases. Landlords, who are leveraged, go broke, too. Banks end up with the property, but worth a fraction of what they lent on it, so they, too are broke.

The strong survive, and cash is king. It purges the excesses out of the capitalist economy. People learn to save, not borrow. businesses don’t leverage. Capitalism emerges stronger, and healthy again, and the stage it set for a long expansion, but only after a lot of pain.

Thats the way the free capitalist market would reconcile things but I suspect helicopter money or some derivative thereof to be used as a stimulus when the short lived viral pandemic subsides.

Trump is making a fool of himself with his ridiculous criticism of the fed. I wish he would just stfu.

So, will the Fed cut rates again on the 18th?

Should’ve never raised from 0%. The economy simply wasn’t strong enough, Trump’s delusion aside.

How does lower rates strengthen the economy?

Lowering the rate at which companies can borrow money and then buy back their own stocks thus pumping up the stock market is not “strengthening the economy”.

Its ridiculous that the government or the central bank ‘guarantee’ any rate of return to anyone in such a state.

this big move from the FED may scare people away from spending and may well reinforce the downward momentum initiated by the coronavirus..

I can assure you, most people have no clue about monetary policy. It pays to be stupid.

And just what the country needs right now, more f**king debt. Debt that we can never repay. The Fed just made the debt bubble even bigger.

But low rates attenuate debt expansion, as with low rates, less new debt has to be conjured into existence to repay existing debt.

Yesterday I said there would be a half point cut BEFORE the next Fed meeting. And as the economy contracts they will likely try to surprise markets with another quarter or half point mid month at their regular meeting. It is too early to see the hard data for us, but they are seeing daily reports in real time and what they are seeing is an economy that has hit a steel reinforced concrete wall. They had to do the half point cut NOW! It was the least they COULD do or the equity markets would have folded like a cheap suit all the way down to about 12k, maybe more. And this cut was already priced in so I expect it will do little to help, by mid month they are going to need to do it again.

The only way it is going to help is by the vast new injections of liquidity into the banks, but that is just going to get used to prevent hedge funds and banks from collapsing. None of this cut will translate to lower consumer interest and thus no stimulus to the real economy. In fact rate cuts like this often hurt more than helping because now consumers will put off purchases as long as they can in anticipation of the lower rates reaching Main Street. But it is not going to happen. At least not unless your FICO is over about 825. The rest of the economy (like 75% of us) are going to pay through the nose for credit, and I know this for a fact because I am buying a house now (close April 6) and the rate is 274 basis points above the 10 year treasury, NORMALLY mortgages are 100 bp above the ten year.

The FED isn’t in the business of propping up the stock market. However, with their low interest rate clown parade, herded the pension industry into the stock market, and now own it all. Couldn’t have happened to a nicer bunch of retards.

MM, first the Fed IS the banks. There are what 23 or 24 primary dealers with Fed window access, and their ONLY job at this point is to prevent the bubble from collapsing. In a serious downturn, the kind where we argue whether or not it is a recession of a depression, all those banks would go under, just as they SHOULD have in 2008. Between 2008 and today these pigs on Wall Street have soaked the population for ALL NEW PRODUCTIVE WEALTH on top of quite a lot of old retained household wealth. The Fed would not have done this cut if they had any choice, but in fact they had none, they did not do it to please Trump, they did it because they had to to prevent a total collapse. Well, it is coming anyway, the solutions are not solutions, they are just buying a tiny bit more time and every application of the printing presses they dig themselves a deeper hole. Every time they “rescue” Wall Street it costs exponentially more, and the effects last shorter and shorter amounts of time. I predict another half point cut by March 20.

Unfortunately, I have to agree. We can call it everything bubble, the domino effect… I am here just to vent my frustration. I myself was on the lookout to buy a home for retirement. Puff, it goes.

“Consumer” interest rates have been way too low. Its a historical aberration, that an individual could borrow for consumer consumption, like housing, for cheaper than businesses could borrow to legitimately expand their factories or production. You’re correct in pointing out that debt spreads are blowing out, and that Fed policy will be unable to stop that trend. At least for a while, banks will experience abnormal profitability due to the rate cuts.

Mommy!

Tax cut or stimulus in the making – by end of month unless virus slows down.

This clown parade isn’t funny any more. And the way to end it, is to get the virus and be done with it all.

Well, that’s one way of looking at it, but like the common cold or flu, this virus mutates so fast that even getting it this year and surviving it won’t guarantee you’ll not catch it again two years later (if in fact it goes global and becomes a permanent part of the human population, like the common cold or flu).

DJ-30 to 10k is my prediction.

If that’s true, the goal of quarantine would change to outlasting the crisis. There will probably be a peak of the epidemic when hospitals are overcrowded and there are no spare ventilators and you really don’t want to need medical care. If you can get past that, and catch it a year or two from now, there will be spare doctors and nurses to care for you and spare ventilators to support you if you need it.

But if that’s true, maybe it would also be acceptable to catch it early and beat the rush. If you catch it literally today, you’re near-certain to get a hospital bed; if you catch it a month from now, who knows? This is another argument against premature quarantine, although not a strong one if you expect your quarantine to work.

Some sources argue that recovered patients can get reinfected with coronavirus, ie people don’t build immunity after surviving it once. This would really suck. I don’t know exactly how to model this – surely it wouldn’t mean a perma-epidemic all the time – but at the very least it would mean it was around permanently and even good quarantines wouldn’t be very valuable.

Microbiologist Florian Krammer (link) thinks these are probably false positives. Some other people have said they might be very elderly or sick people with abnormally poor immune responses. Let’s hope.

The best idea so far I’ve heard comes from South Korea, where they apparently provide free drive-thru testing. Obviously, the result isn’t immediate, but could be available in rather short time.

Yet another unknown is what happens to those who “recover”. Can they run or just limp?

Fighting the last war…

Shortest party ever.

Bet that makes everyone feel better about the economy.