Real GDP

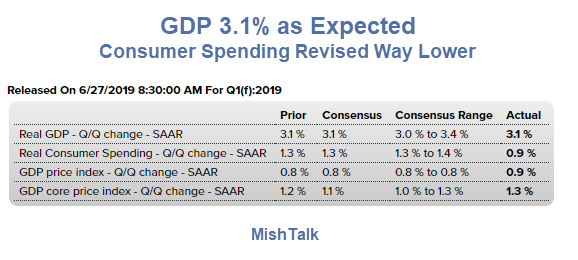

Real Gross Domestic Product (GDP) increased at an annual rate of 3.1 percent in the first quarter of 2019 according to the “third” estimate released by the Bureau of Economic Analysis. In the fourth quarter of 2018, real GDP increased 2.2 percent.

Real Income

Real gross domestic income (GDI) increased 1.0 percent in the first quarter, compared with an increase of 0.5 percent in the fourth quarter. The average of real GDP and real GDI, a supplemental measure of U.S. economic activity that equally weights GDP and GDI, increased 2.1 percent in the first quarter, compared with an increase of 1.3 percent in the fourth quarter.

How?

Econoday has a good synopsis.

- The outcome was expected but not the mix. The third estimate of first-quarter GDP rose 3.1 percent and is unchanged from the second estimate. But consumer spending did not live up to expectations, at only a 0.9 percent growth rate in the quarter vs 1.3 percent in the prior estimate and expectations for 1.3 percent.

- Making up the difference is an upgrade to nonresidential fixed investment, now at a 4.4 percent growth rate vs 2.3 percent in the second estimate, and also an upgrade to residential investment which is now at 2.0 percent contraction vs the second estimate’s 3.5 percent contraction. Government purchases are also upgraded, by 3 tenths to plus 2.8 percent.

- Stepping back and looking at the quarter as a whole, inventory growth (contributing 0.55 percentage points to the 3.1 percent overall rate) and especially net exports (contributing 0.94 points) skewed the quarter higher. Sharp inventory growth made up for thin levels in prior quarters but with inventories still rising so far in the second quarter raise the question, given the slowing in consumer spending, whether inventories will begin to slow and pull down GDP. Net exports so far in the second quarter are clearly negative as imports are widening vs exports. Excluding both inventories and net exports, GDP on this basis (final sales to domestic purchasers) rose only 1.6 percent in the first quarter for a 5 tenths decline from the fourth quarter.

- The first quarter was a headline success but didn’t include strength from the economy’s dominant force — consumer spending. Inventories and net exports aside, whether consumer spending improves will be the biggest issue for the second quarter. Price data in today’s report are moderate but slightly higher than expected with the overall GDP price index at a 0.9 percent growth rate and the core at 1.3 percent.

Contributions to GDP

Rick Davis at the Consumer Metrics Institute has more details.

- The contribution to the headline from consumer spending on services was halved from +0.96% to +0.48%, down -0.64pp from the prior quarter. The combined consumer contribution to the headline number was reported to be down -1.03pp from the prior quarter, confirming a third consecutive quarter of weakening growth in consumer spending.

- The headline contribution for commercial/private fixed investments was reported to be +0.53%, up +0.35pp from the previous report and now essentially flat relative to the prior quarter.

- First-quarter imports added +0.30% annualized “growth” to the headline number (after subtracting -0.30% annualized “growth” during the prior quarter). This amounts to economic “growth” by virtue of fewer dollars spent on imported goods.

- The contribution from exports was reported to be +0.65%, now up +0.43pp from the prior quarter.

GDP Deflator

- For this estimate the BEA assumed an effective annualized deflator of 0.63%.

- During the same quarter (January 2019 through March 2019) the inflation recorded by the Bureau of Labor Statistics (BLS) in their CPI-U index was materially higher at 2.27%.

- If the BEA incorporated CPI-U inflation to finalize the number, GDP would have been halved to a +1.51% annualized growth rate.

GDP?

Grossly Distorted Procedures

Mike “Mish” Shedlock

Guaranteed cut in July – well, call it 99%

So no cut in July?

Allow me to point out that consumer spending is NOT the “dominant force in the economy” – it is only the dominant force in GDP accounting, which leaves out almost the entire production structure.

Yes, Grossly Distorted

Things could be arranged such that spending literally do become the dominant force. For a while. By printing money, regulations and counterproductive dictats at a rate that renders the ability to spend, almost entirely independent of production. Late stage Weimar style: Nothing is any longer produced. All that is left is eating, squabbling, suing and “voting” over what’s left of ones; or more accurately others’, seedcorn…….