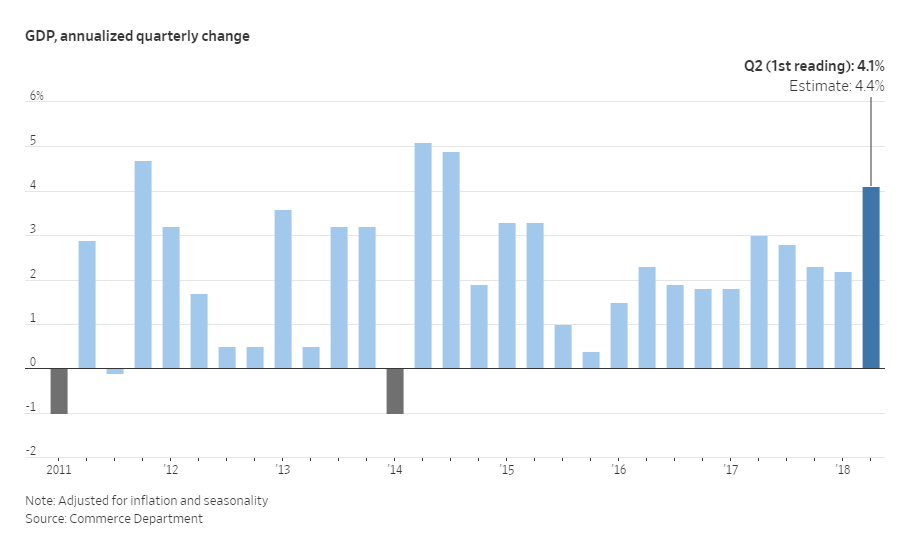

The Second Quarter 2018 (Advance Estimate) show real GDP rose 4.1%, the strongest showing since the third quarter of 2014.

Highlights

- Real GDP: 4.1%

- GDP Price Index: 3.0%

- Real Consumer Spending: 4.0%

- Real Final Sales: 5.1%

Percentage Point Contributions

- Consumer Spending: 2.69 PP (Goods 1.24 + Services 1.46)

- Net Exports: 1.06 PP

- Inventories: -1.00 PP

- Non-Residential Investment: 0.98 PP

- Residential Investment: -0.04 PP

- Government: 0.37 PP

Revisions

The BEA revised first-quarter GDP from 2.0% to 2.2%.

The savings rate for 2017 had a massive adjustment to 6.7% from 3.4%.

Historical Adjustments

From the first quarter of 2012 through the fourth quarter of 2017, the average revision (without regard to sign) in the percent change in real GDP was 0.4 percentage point.

Talk of Overheating, Soybeans, Other Comments

The Wall Street Journal has some other interesting details in its GDP report.

The robust report makes it highly likely the Federal Reserve will continue gradually raising short-term interest rates to prevent the economy from overheating. Central bank officials have raised rates twice this year, and penciled in two further increases this year and three in 2019.

Earlier this month, the Commerce Department said U.S. soybean exports surged in the second quarter, delivering an outsize boon to economic growth even as China shifted much of its sourcing to Brazil in response to its worsening trade relations with the U.S. The export rally likely reflected efforts by buyers to get their soybeans before China’s 25% retaliatory tariffs on U.S. soybeans, which hit in July.

The current expansion, which began in mid-2009, became the second longest on record in July, trailing only the 10-year expansion that ended in early 2001.

Growth has been lackluster during the current expansion: from the second quarter of 2009 to the end of last year, GDP increased at an average annual rate of 2.2%, below the 2.9% rate during the 2001-2007 expansion and the 3.6% rate from early 1991-2001.

Overheating?

This was no doubt a very strong report but it will also be hard to match.

Soybeans and net exports are unlikely to repeat. Housing appears as if it’s ready to roll over, and rate hikes won’t help any.

On the plus side, inventory replenishment will likely give a boost to the third quarter.

Consumer spending has been kept afloat by the stock market and the wealth effect of housing.

And what about that tax cut?

Because of inventories, Rosie may be off by a quarter.

Investment

On the whole, this was a very long and very weak expansion. Things look rosy when they are as good as it gets.

Recall that Alan Greenspan was very worried about the economy overheating in June of 2000 right before the DotCom crash.

Mike “Mish” Shedlock

With the 10 and 30 year bonds still sitting near 50-year highs the bond market isn’t buying this growth story, at least not in the long run. At the end of the day there is no better bellweather for long-term US growth than the bond market.

This expansion is long but has been historically slow until 2017 and 2018. We now live in the age of credit cycles not economic cycles. Speculative bubbles will result in another credit crash. Many millenials have never seen a crash or boom. They were told to settle for low growth by Obama.

At this point a range is fine. The tax cut is now built in to GDP and will add 1%. This is what we are seeing. Prices should flatten out a bit with demand come fall. The Fed will cook this economy too much by raising rates. Instead of letting it adjust to a new equilibrium.

Why aren’t bond yields following this news? Why are their still worries about tepid inflation? Overheating? Nope

Mish way off on his GDP forecast again? Wow, I’m shocked…not.

How much credence can be put in figures that are continuously revised? From your included chart, they could not even get government spending right?