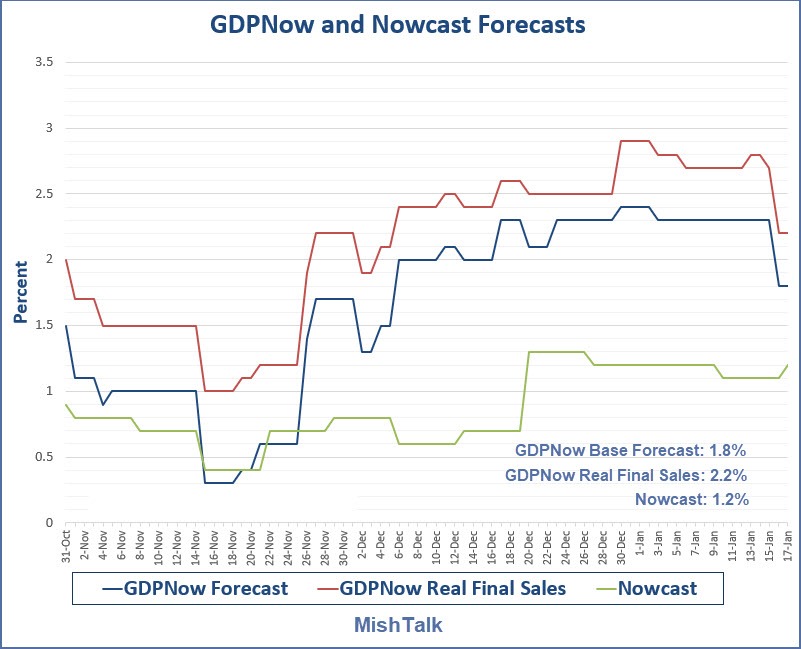

The Atlanta Fed GDPNow Model forecast for the 4th quarter fell a half a point this week whereas the New York Fed Nowcast Model rose a tenth of a point .

GDPNow Tracking

The yellow highlight shows the half-point drop on January 16.

Analysts, including me, generally concluded sales were solid, rising 0.3% in December, yet the GDPNow forecast fell.

I commented Retail Sales Mostly Solid But Department Stores Hit Again.

Q. Why the forecast decline?

A. The model expected better.

It’s not the report that matters to these forecasts, but rather how well the forecast dose vs. what the model expected.

Housing and Industrial Production Balance Out

On January 17, I noted housing starts rose to a 13-year high.

I would have expected the GDPNow model to surge but nothing happened because Industrial Production balanced things out.

I commented Industrial Production Numbers Confirm Bias of Housing Report.

Weather Impact

“The drop for utilities resulted from a large decrease in demand for heating, as unseasonably warm weather in December followed unseasonably cold weather in November,” according to the report.

It was that unseasonably warm weather in December that totally skewed the Housing report.

For example:

In the Midwest region, not-adjusted single-family housing starts rose from 9,200 to 9,600. This was reported at a seasonally-adjusted annualized rate of 180,000 and a whopping rise of 56.5%from November.

For more details, please see Housing Starts Surge to a 13-Year High Thanks to Massive Seasonal Adjustments

Word About Models

Models do not take weather or any other one-time issues into consideration.

Looking ahead, the GDPNow model is likely going to make some housing forecast assumptions that will not happen. Thus, from where things stand now, the model is likely on the high side.

Mike “Mish” Shedlock

Decade of printing hundreds of trillion to drive (pretend)growth bought some time, this decade will usher in the big Q…quadrillions to get the same (fake) 1-2 GDP.The fed will print over half a quadrillion dollars this year …an all time single season record to hopefully keep the scam propped up and buy time till the election.

Between Halloween (31-Oct) and now, a two month period, the GDP prediction averaged 1.5%, but was as low as 0.5 and as high as 2.5%

The error term (1%) was almost as big as the average value (1.5%), and this is without annualizing the error term.

“It’s not the report that matters to these forecasts, but rather how well the forecast dose vs. what the model expected.”

The same for analysts’ expectations for individual stocks – always need to look underneath the top lines.

Thus, total stock market capitalization continues to grow FIFTEEN+ TIMES faster than GDP. This is highly abnormal and should be scaring the hell out of people.

This is all about bailing out anyone holding stocks. The Fed has been buying stocks since 2012.

Yes, it is the hangover from the GFC, where do people think all that worthless paper went to? Nowhere. It is all still out there waiting to mature at face value. The face values were upheld when the FASB changed the mark to market rule to mark to make believe. And they do not have to be recognized till the maturity dates when the banksters go to cash in those financial jokes. Once they started maturing (now ten years on which was the maturity a majority of them were written for) the banksters are being forced to write down those losses. So, the Fed has quietly pumped in those trillions over the years to cover the losses, and it is why we now have QE4.

They never waved a magic wand and ~POOF~ no more highly leveraged and fraudulent CDO’s and mortgage backed securities. They still exist and are still legal instruments no matter that the issuers no longer exist, they are links in a fiduciary chain that is broken, but cannot kill banks till they are forced to recognize that the chain is broken, and that day is the day the instruments mature and there is nobody to pay. It is what we were asking back then, what happens when those frauds mature? This is what happens.

There are still a couple million unsold properties the banksters acquired in the collapse in 08/09/10. As long as they did not sell them they never had to reverse the stream of 360 payments they booked on closing the sales of the properties back then, now they do. It is a decent chunk of why houses are so unaffordable now, there are a lot of empty and after a decade of neglect unlivible homes.

GDP includes the public sector and small business, which are not comparable. Stock market capitalization only reflects the largest companies, which are in the best position to deploy capital and technology for earnings growth. Valuations are not that crazy in light of the interest rate environment. PE’s are high, but long term rates are low.

Both of you are right, and while inflation is FAR higher than the CPI indicates the level of faux funds into the equity markets is not causing the hyperinflation the economists should expect from such vast amounts of printing. The reason I believe is that the money is sterilized to the top 10% of households by net worth and even at that mostly to the top 1%.

The top 1% owns 50% of all stocks and the top 10% owns over 90%.

So, if nearly all new wealth is going into the market and pushing that higher and higher every day the money is limited to just 10% of the population who were already rich when the market took off, in short, they have extreme low velocity of money. Leaving few assets for the bottom 90% of us who have a very high velocity of money and which is driving the inflation we do see. But, it is also driving the deflation we see in other areas of the economy as smaller and smaller amounts are left over after immediate necessities are paid for.

The place to start looking at this I suppose is the market cap at the 2009 low of 6,469 on the Dow, to now 29,000 on the Dow and a market cap of at least $36 trillion, though finding good data about market cap in 2020 is harder than finding that famous unicorn that shits rainbow skittles. Maybe some of you with a Bloomberg terminal can answer these questions.

Whatever that gap is clearly the top 10% and mostly 1% have been the beneficiary of all that printing. It has to be in the tens of trillions. Even as the assets owned by the bottom 90% have shrunk relative to the rest of the economy so much that I am actually shocked that we have managed the political stability we have so far. That stability I think though is getting very brittle.

Redistribution I think would be mostly a disastrous policy, but they could easily collapse the equity market wiping out much of the top 10%’ers wealth, even as they institute better social nets for the rest. That would go a long way towards ending the wealth gap that is destroying the fabric of American society.

We do need to redistribute at least enough for people to live. The US is too wealthy to let so many of our citizens struggle (homeless, sick, forced to sell drugs or sex to survive, drug dependent, etc.) Check out “Dignity” by Chris Arnade for a first hand perspective. The capital markets are a critical means of allocating capital to business and technology, the best in the world. We can’t just deflate them.

On the other hand, the top 1% of earners and asset holders have been massive beneficiaries of the technology boom and will continue to benefit. Capital and technology are muscling out labor among the key inputs. A manageable tweak to the income tax code (especially capital gains) will go a long way. I like Andrew Yang’s UBI/VAT plan, but I am sure that there are other plans worth considering. Use taxes to fund a safety net for people and communities who have provided labor in the past. They will increasingly need help.

Those that ignore the wealth gap will be the ones most shocked when the nation turns to socialism and kills prosperity once and for all. The GOP (propaganda, MOST republicans do not swallow this crock ‘o shit whole) calls every social safety net “communism.” Social security for example, many still want that strangled, give the trillions in trust to Wall Street mandarins. They claim to see net worth as god’s judgement on your value as a human being, and the sum total of the quality of your actions as rewarded materially. What a load of bullshit. But it does explain their racism, since whites are better off they must be superior right? God’s favorites to be so “blessed.”

I know many of the youger debt saddled people who are new or almost new voters, they KNOW socialism is going to destroy the nation, and I mean REAL socialism not the programs designed to help people capitalism screws for profit like food stamps. They know it is going to kill prosperity but they do not care, they are already in poverty and they now just want to see a fairer life where if they have to struggle to survive in structural poverty with no opportunity for social mobility then F$%£ the rich, take them down too and see how they like it. They have lost hope for equitable society and now just want revenge and I cannot say I blame them for feeling that way. I don’t agree with it because the dislocation they seek is not merely financial, people are going to die, maybe lots of them.

By the way, that prick Yang was a loser I would never have considered voting for. Your disabled veterans (100% disabled total and permanent) get about $3,000 per month to get by on, 20 years ago that was “adequate.” It is borderline poverty in MOST of the nation today, and Yang specifically cut us out of his so called UBI plan, hint, if you cut out groups of people you don’t like then it is not Universal is it? His dipshit rationalization was we already get what amounts to free money from the government so should not need more. I resent that, my vet disability is NOT free money, I had to serve and get disabled defending that little prick’s concept of fairness. And no matter what else anyone says a UBI will trigger immense inflation, a UBI would help to address wealth inequality but is a wash as far as standards of living goes because probably dollar for dollar it will just raise prices. It is a devaluation of the money and nothing more, but, where it raises some people’s income by 50% it has practly no detectable impact on the incomes of the wealthy. A guy making a million per year gets a $1,000 per month UBI payment, that is what? 0.0001% raise? Where for a part time minimum wage employee it is possibly close to 100% increase. And the bigger the UBI the closer the two will be. The real effect is that it devalues the rich man’s dollars a lot faster than it devalues the poor. Or to put it another way, a UBI is actually nothing but another social safety net to stop people from starving in the snow when the government finally devalues the rich out of their dynastic feudal wealth.

I agree Barn_Man. Another article here warning of impending doom.