Cash Out Refis Exploding Once Again

Please note Cash-Out Refinancings Hit Highest Level Since Financial Crisis

Americans extracted more cash from their homes through cash-out refinancings in 2020 than in any year since the financial crisis.

U.S. homeowners cashed out $152.7 billion in home equity last year, a 42% increase from 2019 and the most since 2007, according to mortgage-finance giant Freddie Mac. It was a blockbuster year for mortgage originations in general as well: Lenders churned out more mortgages than ever in 2020, fueled by about $2.8 trillion in refis, according to mortgage-data firm Black Knight Inc.

“The support coming from home equity is unparalleled in helping smooth out the degradations from Covid,” said Susan Wachter, an economist and professor at the University of Pennsylvania. “For those who are in the position to refinance, it’s a major source of support.”

Cash-out refis got a bad rap after they exploded in the run-up to the 2008 financial crisis. Borrowers tapped their homes like they were ATMs. When home prices plunged, they were left owing more than their homes were worth. Now, in 2021, many economists expect home prices to keep growing.

Still Room!

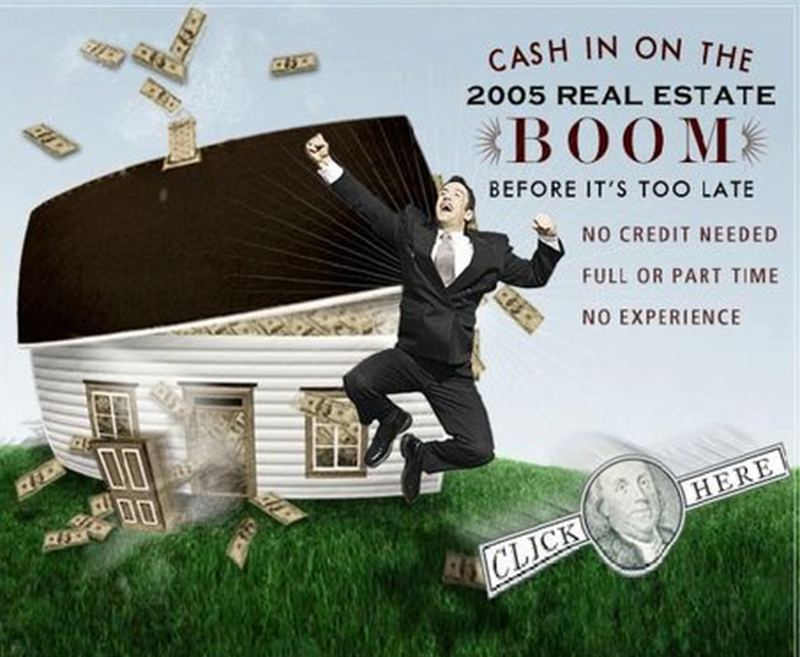

This reminds me of a post I did in 2005 (Yes, I have been blogging that long, even longer).

It’s Too Late

Flashback December 13, 2005: It’s Too Late.

It was a very short post. Here is my 2005 post in entirety.

I think it’s too late.

In fact I know it’s too late.

How do I know?

The following Email I received tonight should explain it nicely.

When you see stuff like this, not only is it too late, it’s way too late.

The Email I referred to was the image itself.

At the time, I was also commenting on cash-out refis, housing speculation, and numerous other aspects of the housing bubble.

I was early. Depending on the section of the country, there was at least one more year left of the bubble before things started to implode.

Fed Chair Ben Bernanke dissed all discussion of bubbles even after the bubble already burst.

Choice Bernanke Comments

- May 17, 2007: Chairman Bernanke said: “We do not expect significant spillovers from the subprime market to the rest of the economy or to the financial system.”

- February 27, 2008: Chairman Bernanke said: “By later this year, housing will stop being such a big drag directly on GDP … I am satisfied with the general approach that we’re currently taking.”

For five additional choice Bernanke comments, please see Ben Bernanke Just Won’t Stop Making a Fool Out of Himself

Powell Fed Comments

This time, it’s the Powell Fed dissing bubbles.

For discussion, please see Fed Hubris: Housing Prices Show the Fed is Making the Same Inflation Mistake

I have many housing charts in the above link.

The Bad Rap is Different This Time

Fortunately, “It’s Different This Timetm” because just like last time “many economists expect home prices to keep growing.”

So realistically, what can possibly go wrong?

Mish

I too saw the 2008 housing crash and I too was early. My problem as an honest realtor was that I warned about a growing housing bubble in 2003 because of the government’s housing market interference with the creation of such masterpieces as the No-Doc Loan (liar loans). By 2005 I remember turning a young couple away. “Don’t buy”, I pleaded. “Rent until this housing bubble is over. Housing will crash.”

It was agonizing for me. How could people not see, I wondered. I know now that most people are simply not thinking about such things. They go to work and there’s traffic. The neighborhoods look the same. Everything is just fine, they think. But it wasn’t fine. And this time it’s so damn bad that I’ve lost faith in our government. America is being set up to fail. By our loving government, and the stinking FED.

Crypto won’t save you.

The market for US Treasuries is not what is was 10 years ago. 2012 or so the Chinese shifted to buying mines and such instead of investing in US treasuries during the monetization of the GFC spending. Perhaps interest rates rising will be the trigger event? Although the the Fed controlled the last interest rate move up recently..

“Ben Bernanke Just Won’t Stop Making a Fool Out of Himself”

In Ben Bernanke’s it is not a question of won’t, it is a question of can’t. A cock-sure crackpot if ever there was one.

It is relay when it comes to crackpots. Bernanke to Yellen to Powell.

In a new trading account I started at the start of the month, I looked at my rate of return so far and I’m up 5% in 10 days buying boring equities. Made me think, maybe I should pull that heloc and go all in. Not that I would be that crazy of course but I found serendipitous that Mish had this article today. I would guess a lot of people will do things like that.

If we hadn’t received PPP and EIDL money it’s possible that a cash-out refi would have been the only way for me to stay in business and survive financially in 2020…so I do understand how the pandemic might make it necessary to tap home equity.

At this stage of my career, however, it’s the very last thing I want to do. I’d like to see all my mortgages get burned within seven years. I doubt I’ll live to see the EIDL paid off. I’ll probably just have to sell my practice with debt still outstanding, if I can. I don’t expect that would be a problem if we can get back to something like normal this year.

I wouldn’t buy stock in this market with ANY money, much less borrowed money. I’ve thought about taking equity out to buy more real estate, but I think I’ll wait and see if prices tank at some point….and then do it. I took out money to buy property in 2009, and it worked out fine.

The RE market would have to get far worse than it’s ever been for me to be upside down. I have some degree of safety at this point. It would take a perfect storm to wipe me out. I suppose it could happen. I never say never, and I try to prepare for the worst, as best I can.

98% of Katrina EIDLs were forgiven within 6 years.

I can’t imagine it taking that long for COVID EIDLs. Especially after repayments are supposed to start this summer, but instead we’re likely to see record defaults.

Join any SBA/EIDL/PPP group on Facebook and it’s clear those people won’t be able to pay back their EIDLs. 1/2 didn’t even realize it was a loan.

No personal guarantee, tied to just one owner of the company (I’m a decade older than my wife, so we put it in my name)… forgiving them faster than the defaults will be like a game of whack-a-mole.

Make sure you pay back your EIDL at the minimum pace… maximize that forgiveness.

Hope you’re correct. Good info, thank you for sharing that. I am now making payments….glad they’re reasonably small. I can pay it according to the terms, but at my age it threatens to be a burden when I cash out of my business, which I will no doubt have to do at some point, whether I want to or not. In the short run, it is an incentive to keep working. The business has always been healthy and can carry the debt, as long as the terms are decent. But who wants to be 80 and still paying an EIDL?

Search on “SBA Extends Deferment Period for all COVID-19 EIDL and Other Disaster Loans until 2022.” Decision announced today.

Odds are we’ll never need to make a payment on our EIDL.

Thank you very much for that. I had not heard.

My payments don’t start until summer. Think that’s the case for most the EIDLs.

I’ll pay minimum, because I think it’s inevitable that all the non-fraudulent ones are forgiven, and when they are, I want the largest possible amount forgiven. The low interest is worth the price on that lottery ticket. A decade from now, if it turns out that I’m wrong and I’m still paying it, and I’m healthy, I’ll just pay it off. If I’m on death’s door, I’ll just die with the debt. No personal guarantee so they can’t chase my estate. I’m only 50 and healthy, so I think the high-probability events are 1) they forgive it, 2) I pay it off in about a decade.

Mish, did you address this issue with unions getting bailout money? https://www.nytimes.com/2021/03/07/business/dealbook/bailout-pensions-stimulus.html

I know that would normally be the sort of thing you may have opinions on.

“This time, it’s the Powell Fed dissing bubbles.”

Wash, rinse, repeat.

Don’t get soap in your eyes.

The new housing bubble has only just begun to inflate, there are many more good years ahead for residential real estate.

If one has a reasonable income ya gotta live somewhere. in many parts of the country (mostly rural and red states) homes are still reasonably priced.

The price to rent ration is back where it was right before the crash. As a result in many parts of the country renting is significantly cheaper than buying.

what if that ratio continues to go up? it’s the same as high p/e stocks being supported by low bond rates.

it is definitely different this time. there are no ninja loans and people aren’t levering up waiting in line to buy houses. builders aren’t building as fast as they can. it’s just that the pandemic has caused supply to be very tight. real estate is definitely not a problem right now, at least not residential.

Big time inflation is here if you look. Wife is reprising up again after prices were increased just last week at the hardware store. To many $ chasing constantly emptying shelves, thanks to the FEDs free money policy.

Framing packages are up 30% from Jan 2021/ , $250,000 lots are being snapped up at $425,000 with little to no inventory left.

It is bad when you aren’t sure if you need to prepare for the bubble bursting (deflation) or the bubble growing multiple times bigger (inflation). One makes cash more valuable and the other makes cash less valuable. I think that we will find out how it feels to live in Argentina which has about 45% inflation per year. They don’t even price real estate in local currency.

In 2008, we still had some tiny semblance of sanity. If the monetary policies and stimulus of today were in place back in 2008, that bubble never would have burst. This time the “buy now or be priced out forever” crowd is 100% correct. Soon, 40 year mortgages will be the norm, just like 84 month auto loans, and home prices will rise even further. A significant correction in asset prices will never be allowed again.