What’s Japan to Do?

The Wall Street Journal reports The World Should Watch Japan’s Attempts to Save Its Struggling Banks.

After 30 years of falling and even negative interest rates, many of Japan’s regional lenders have share prices of 0.2 to 0.3 times their book value—levels that would have been considered catastrophically low even a few years ago.

The Bank of Japan is offering commercial lenders an extra 0.1 percentage point in interest on their deposits with the central bank if they reduce their overhead ratio by certain benchmarks, or merge or integrate their businesses.

A marginal shift in interest rates on accounts held with the central bank might not sound like much, but Moody’s Investors Service rightly notes that given regional banks had an average return on assets of just 0.14% in the last fiscal year, an extra 0.1 percentage point return on large cash balances is nothing to sniff at.

Any institution that relies on interest income is going to be squeezed continually if rates remain low for an extended period, as bond market prices clearly expect them to. With less fee income, similar issues are likely to present themselves in regional lenders around the world.

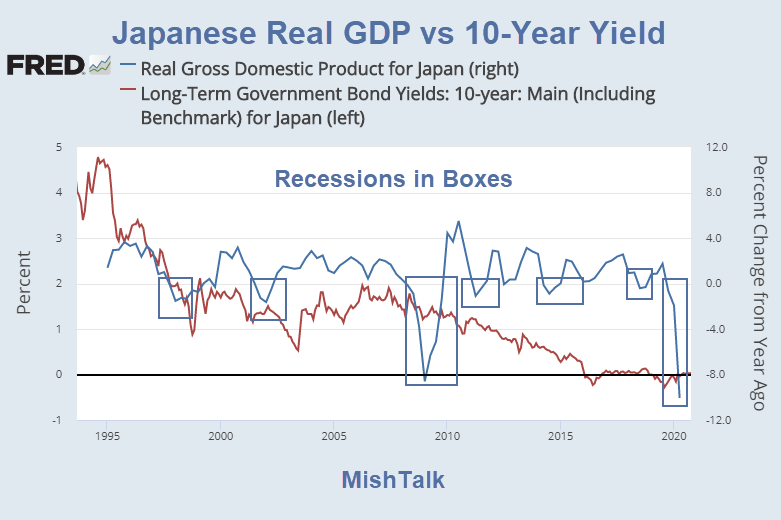

Low Interest Rates Did Not Promote Grown

Neither low interest rates, nor QE, nor wasted fiscal stimulus promote growth over the long haul.

Japan tried all three for decades. The results speak for themselves, recession after recession.

Zombification

Instead of promoting growth, artificially low interest rates promote zombification.

Unproductive companies are artificially kept alive at the expense of more productive companies.

- December 16, 2017: Zombie Corporations: 10% of Companies Depend on Cheap Fed Money

- July 19, 2019: Zombification Perfected: Negative Yield Junk Bonds Take Hold in Europe

- November 18, 2019: China, like Japan in the 1990s, Will Be Dominated by Huge Zombie Banks

Fundamental Strength of Capitalism

A fundamental strength of capitalism is that failed companies go out of business making way for new ideas and better models.

Yet, here we are. The Fed, ECB, Bank of China, etc., all strive to keep failed companies alive. Zombification is still on the rise.

Self-Inflicted Pain

I have been preaching this message for years. Low interest rates are a huge problem.

The ECB faces a worse setup than Japan with hugely negative rates.

Think of it this way: Negative-yield bonds imply it is better to have 99 cents ten years from now than a dollar today.

That is of course illogical, and in fact impossible in a free market. We see these things only because of failed manipulation by central banks.

Fed vs ECB

Whereas the Fed pays interest on excess reserves, the ECB charges interest.

The process slowly bailed out US banks over time in the US but further crippled European banks.

Purposeful Destruction of European Banks?

Policy at the ECB was so questionable, especially given years of study of failed Japanese policy, that I often wonder if it was intentional.

Here’s the setup:

- Mario Draghi, head of the Italian Central Bank replaced Jean Claude Trichet as head of the ECB.

- Troubled Italian banks were widely understood as crippled and unable to lend because of capital restraints and nonperforming loans.

- Draghi forced more excess reserves into the system via QE.

- Draghi the went down the rabbit hole of negative rates charging crippled banks interest on excess reserves, further weakening the banks, and not just Italian banks. Look at Deutsche Bank for example.

- Why?

- By any chance was it to so destroy the European banks so that Germany would be forced to commingle debts and bail out Southern Europe?

That’s plausible but against Occam’s Razor that suggests simpler explanation are more likely to be correct.

The simple explanation is that Mario Draghi was just plain stupid.

Will the Fed Go Down the Rabbit Hole?

Many believe so, but I don’t (as least not that rabbit hole).

The Fed is beholden to the banks. It does not give a damn about consumers as long as it keeps the banks alive.

Short-term, zombification and QE allows companies who could otherwise not pay back loans to do so. But negative rates that punish banks are another matter.

The Fed understands this and it can see the problems facing the ECB and BOJ so it is unlikely to go there.

Bond Bull Lacy Hunt Warns of a Huge Monetary Risk

I commented on the US setup twice. Both are worth a review.

- Aug 18, 2020:

Bond Bull Lacy Hunt Warns of a Huge Monetary Risk - October 22, 2020: Two Inflationary Tail Risks For US Investors

Those links contain observations by Lacy Hunt and me on what the Fed has done and what it might do.

Although the Fed is unlikely to go down the negative rate rabbit hole, there are other rabbit holes the Fed might try.

One of them is direct printing, making the Fed’s liabilities legal tender or a medium of exchange.

Hunt suggests huge inflation risk if the Fed pursues that path.

See the above two links for further discussion.

Mish

“Think of it this way: Negative-yield bonds imply it is better to have 99 cents ten years from now than a dollar today.”

Not exactly. What they imply is the market thinks rates will go more negative. It make no sense to buy something for a dollar, hold it to maturity, and end up with 99 cents. What makes sense is to buy something for a dollar and then sell it for $1.01 to the FED who doesn’t care about the -2% yield.

Maybe the reason that they have low interest rates and slow growth is that they have had a stagnant population for 35 years. There is no growth there! And, there is a free market for interest bearing instruments. If the free market deems that these instruments shouldn’t pay interest, how is the central bank going to make it different?

Zero inerest rates are a Robbery of seniors life’s work of savings. Negative rates empties the banks accounts of what’s left over from the Zero rates .

It’s not just seniors, but that is the most terrible aspect of this “policy.” We’re just animals at the end of the day.

When all you have is a hammer, everything looks like a nail.

Back in the day I was taught that among other things a currency needs to be a store of value. Who honestly believes that anymore?

Actually the US dollar has been a very stable store of value for a long time now with low inflation. If you want a return on this value, then store it in other assets – real estate, stock market, etc., but also accept the increased risk. If there is risk of asset deflation, then storing value in currency with a negative interest rate might be the best store of value available.

“Some are worried about inflation, I would worry more about deflation.”

Me too, as I just said in another comment.

That’s because you have assets..

Inflation steals from the poor and pays down the debt…..a hidden tax on working people and the elderly.

People with substantial assets fear deflation more….people with NOTHING fear inflation more.

If the Fed does something that sets inflation on fire…….poor people can’t eat or pay rent.

But if the Fed allows a credit lock-up to lead to a depression (another name for rapid uncontrolled deflation) then investors lose much of the nominal value of their tangible assets…..and (much worse) perhaps ALL the value of their intangible assets.

The Fed works for their member banks best interest….and they are people who DO have lots of assets……so you can see how the game gets slanted to make it work for them.

The BIG PROBLEM…..how do you get inflation in a low growth/no growth world with a whole laundry list of strong deflationary factors that you can’t control?

And more importantly, very modest inflation that people can adapt to…..because people can adapt to anything if the change is slow enough…..but when inflation, especially food and rent, is bad…they have difficulty adapting.

The other thing I’d try to point out…..is that we shouldn’t confuse the “explanations” for the Fed gives to the public and the dumb journalists…..for their policies….with their real motivations…..because the two are often different. Maybe always different, at this point.

I doubt anybody at the Fed is fooled into thinking that perpetual low interest will create new growth …….n a world with real limits to growth……that have little to do with monetary policy….

What it does is to keep the debt bubble from collapsing today or this week…and hopefully this month and this year. I’d say this is one objective.

“Stimulating the economy” is a smokescreen….a convenient one…for doing anything and everything necessary to keep this late stage Ponzi afloat.

Which is financial repression of all non-elite taxpayers……and punishing savers of cash. In pursuit of inflation…..needed to inflate away the massive debt. That is the Fed’s other unstated goal.

Reform…whether it be by means of gold-backed money…or just more prudent interest rate policies that reward savings…..would seem to me to be an unlikely outcome for this road we’re on.

I don’t fear inflation….as an investor I am set up to profit from inflation…..but I do fear deflationary events….that negatively impact asset prices in a rapid and chaotic way…….because it can make anyone, or at least most of us, very poor, and very quickly.

“What it does is to keep the debt bubble from collapsing today or this week…and hopefully this month and this year. I’d say this is one objective.”

Maybe. I’ve just read about a AAA Chinese Bond that’s just defaulted which should be a wake up call for people who think the government will be a permanent backstop.

Yes, I noticed that as well. We should not forget that China is the most indebted nation of all. Nobody else is even close…and they are the poster child for malinvestment.

Controlled demolition or inability to manage reality, is the question maybe. It is almost impossible to judge what is purposeful or not when most of the cards are held by one player.

I think it would be helpful to differentiate rising asset prices from rising prices of goods and services. Forgetting about Mish’s arcane definition of inflation which had to do with money supply and Mises mumbo jumbo, using the common definition of inflation which is rising prices, to increase the price of any good or service, increase demand relative to supply. To cause deflation, increase supply relative to demand.

How to increase the demand for goods and services?

1. Put more money in people’s pockets, via tax cuts, or direct deposits of dollars into everyone’s bank accounts. The various COVID unemployment payment schemes are an example, but imagine such schemes during a period of low unemployment.

2. Increase the population of consumers by opening the immigration floodgates, as one example, or by putting Spanish Fly in the water supply.

3. Destroy supply.

Under such scenarios, one could have goods and services inflation under low interest rate conditions, which would enable stable or rising asset prices.

Also – this is not a monetary policy issue the fed can solve by itself. Fiscal policy needs to do the heavy lifting – tax and spend (or print and spend) combined with right government led initiatives, but only a remote chance of this happening in a sufficient and appropriate manner given state of politics and disagreement in the US.

Isn’t this just a suppy-demand issue? – too much money sloshing around chasing limited investment opportunities, driving down yield and driving up asset prices? There is a tremendous amount of wealth out there that is not being productively invested. Is this a failure of the capitalist/small governement model? Private enterprise is not creating sufficient investment opportunities? Some blame government regulation for this, but I don’t buy into this. Negative yields is a powerful tool to get people to invest the cash, the problem is they would just invest in real estate or stocks, and increase those bubbles. What investmentments would make sense? Maybe government infrastructure projects, further investing in education, investing in social welbeing programs – all of this gets the money back out into the community working. some form of weath or other higher taxes might be necessary, or maybe MMT is the mechanism to get the money working again. Some are woried about inflation, I would worry more about deflation.

Low interest rates ultimately reduce profits. If the rate at which a company can borrow falls, they can afford to operate on lower margins. This forces other businesses to reduce their margins or become uncompetitive. Companies then have to use leverage to compensate for the fall in the absolute return. It’s a vicious circle encouraging more debt for less return.

I don’t think your simple analysis is correct, as there are many interrelated factors that determine profit. If low interest rates encourage more entrepreneurs to start businesses, then this might increase competition and work to lower profits, but the low interest rates also stimulate borrowing and spending, that increases demand and profits.

This is a good read. It’s quite long, but interesting if you have the time.

“Think of it this way: Negative-yield bonds imply it is better to have 99 cents ten years from now than a dollar today.”

Respectfully, think of it (just for a moment) in another way:

It is better to have 99 cents ten years from now than to risk having 0 .99 cents in ten days or ten weeks.

The logic being……that it is temporary safety that is of utmost importance…..in a time when deflation could occur ANY DAY in the form of a chain reaction that locks up the credit markets…which would result in a chaotic price restructuring of just about every asset you can name, including gold..but in this case more importantly….the Euro.

“The simple explanation is that Mario Draghi was just plain stupid.”

I’ll offer the alternative ……that it wasn’t stupidity, but fear driving Mr. Draghi….along with one other thing…..the idea that at some point he could hand off the problem to a successor, and float home on his golden parachute, with the worries of the world no longer his to worry about.

Which he did, more or less.

To understand Draghi, understand that he stood for one thing above all others…which was the preservation of the Eurozone and the Euro currency. As Draghi himself famously said, he would do “whatever it took to make that happen”…and that “it would be enough”.

None of this is in any way aimed at arguing against hard money….just an explanation of the forces that led to the bad situation we’re in.

Now they are floating these new bonds…the ones that are Eurozone Sovereign bonds by any other name….I forget what they’re calling them…..some kind of environmental “green energy bond”? Something like that.

For the Euro this is necessary….it’s been so obvious for a decade that the big problem is one currency but many sovereign nations, each in different economic circumstances, but each able to issue its own bonds. Necessary but not politically palatable.

One further thought:

“Whereas the Fed pays interest on excess reserves, the ECB charges interest. “

This is also not without consequences…..the primary one being support for the US dollar and every asset denominated in dollars. This is why the USD is so stubbornly strong in the face of our profligate spending….that and the fact that there is an awful lot of foreign debt that has to be repaid in dollars.

My thesis, right or wrong….is that we go even further down this crazy rabbit hole into negative interest rate territory….which can happen fairly easily if two small impediments are removed.

One is that cash would have to be eliminated.

The other is that all financial transactions would be completely transparent and traceable by governments….

Both these things could be done by adopting sovereign cryptocurrency and making other cryptos illegal.

Far fetched? I don’t think so.

“One is that cash would have to be eliminated.”

It’s just a matter of time before this happens in my opinion. It’s so much easier to tap a phone or card making it such an easy sell. As time passes the older people that prefer cash will become fewer and fewer.

It would have to be outlawed, mired in legislation and/or cash simply withdraw. Businesses that say “we still take cash” would do well, even if it became niche market. Look at UK history of tokens for example, or any other medium improvised for exchange that works outside whatever regime is in force. The trouble as I see it is that those wanting to install an absolute system are extremists or fanatics, and if they aren’t then those that replace them will be. We know what that means in real terms.

I think cash will just phase out. People won’t want or need to use it. There’ll be no need to ban it.

Well that is very optimistic of you 🙂 . It won’t phase out by itself though because there are a myriad of uses for it where cbdc won’t do – if it is available it will still be used, if it is withdrawn something else will take its place. What is possible is that society becomes so caught up in legitimacy and disdainful of other, or that people become drone enough that they won’t even understand free private exchange, that cash or eq. becomes not worthwhile to attempt…criminals and all that . Here is a real example, just one:

Someone has some friends in authority threaten another, they do that illegally but are capable of causing much damage and are connected. The person being threatened turns that over to authorities, who may or may not be complicit or inefficient, definitely deficient at protecting that person. So he decides to move to somewhere he doesn’t feel threatened. What does he do ? He pays cash to stay somewhere else, if he paid digitally the authorities would have his location via transfer to owner of residence . The residence he rents accepts cash, because it is legitimate, the income does not have to be declared from a particular purpose or person. Sure, this person might be traced roughly via coms, but seeing as he has done nothing illegal their use is going to get a lot of questions asked of those persecuting.

Take away cash and you, you personally that is, are made vulnerable even if you don’t realise it.

I think we’re trending to a cashless society to the extent that it’s use ‘by mainstream society’ makes it meaningless. I’ll change my mind slightly in the light of your reply

-:) As you imply/say criminals will want to carry on using it. However I think they’ll find it increasingly more difficult to obtain the volumes they need, it will stand out too much. So I’m still not sure they’ll need to ban it. I agree criminals will find another way.

Criminal activity is a known known, in that those transacting both know that the objective is to hide the transaction, and so endless means are available for improvisation, and usually there is infrastructure to accomodate the method of payment already in place.

The ability to transact anonymously though is important at small everyday scale for people, not only because it is more personal that way (here is something of mine for something of yours, unencumbered), it’s really one of our last defences of public freedom, or of freedom of the public. I didn’t think I would ever have to write something like this, because cash did seem like such an installed and understood reality.

Anyway, there is still a lot of opposition to elimination of cash so we will see.

I agree about freedoms. That’s why I don’t think it will be banned.

I’d still like to have the option of paying in cash. I might lose my phone or cards or there might be a power cut. However most people don’t equate paying with a card etc as a reduction in their freedom or liberty. Perhaps if the option to use cash was withdrawn they might. They’d certainly recognise the impact it might have on the “black market”, but many would view that as positive. Anyway it’s not happening tomorrow so we’ll see as you say. Good talking to you.

Equally, its good to talk .

This is old now but I’m sure it would be more pronounced now.

For a more critical look at how digital currency is evolving

He theorises on how that intersects with politics and globalisation, which might come across conspiratorial, but there are some very straightforward technical articles also there that simply outline the agenda, format and mindset of those involved, which are definitely worth reading.

“Think of it this way: Negative-yield bonds imply it is better to have 99 cents ten years from now than a dollar today. “

I was going to reply the same to that.

The idea of lowering rates to oblivion is mutual, the “no exit” phrase comes to mind:

Floating rate mortgages get bailed out.

As Scoot says sovereign spending gets bailed out.

Syndicated issuance means banks make on carry trade.

Banks restructure using lower rates and still profit.

Consumer spending increases bailing out northern manufacturing and finance.

A lot more, all tied up in Target2 imbalances and false values.

The result is inbuilt political leverage across europe, and consolidation of financial control/banking , expressed ultimately by mutual issuance and government.

To think this is by mistake or stupid is extremely naive, the plan being followed is decades or more old, and well known. That it succeeds or that it is plain wrong is another question. No exit means there is no alternative allowed to be considered.

If they go the crypto way, then we are ending up with a planned economy, micromanagement of society, and a political panorama that is unimaginable at present.

At what point does it become impossible to raise rates again?

Couldn’t make it much above 2% last time (not even inflation) before the market was crying “Uncle”.

Much more debt now–it’s keeping the economy afloat.

Higher interest rates means higher repayment costs means failures of the impaired parties.

It a puzzle for the ages.

And what about JS’s free-marketeer bona fides?

“Before Trump became president, she was a longtime advocate for free trade, but after he became president, she supported his administration’s trade war with China.[6][20]”

Why it’s as if Trump can make her forget all about her silly Nancy principles!

Spin the spinner, who knows what’ll come up?

Low interest rates promote growht? maybe

But low interest rates also promotes mal-investment and causes savers to subsidize borrowers or perhaps more aptly transfers wealth from those with capital to thoe with primary access to credit

Judy Shelton and her consistent monetary views to the rescue! She apparently favors higher interest rates … wait for it … when there’s a Democrat in office! Co-inky-dink!

“During the Obama years, she criticized the Federal Reserve’s low interest rates.[29][30][31] During the Trump presidency, she advocated for the Federal Reserve to adopt lower interest rates as a form of economic stimulus. (Trump frequently criticized the Federal Reserve for not lowering interest rates.)[4][29][32] “

I suspect if Mr Market pushes US rates negative its game over for the current world financial system. I think the FED suspects this as well.

Negative rates also mean it’s cheaper for governments to borrow via the bond markets than issuing/printing money which has a higher rate, zero.

More evidence of what the real purpose of the Federal Reserve Act!