The meme of the day is wage growth is accelerating.

I disputed that notion on February 7 in Acceleration in Wage Growth is a Statistical Mirage.

On February 16, I reported Congratulations Workers! You Make One Penny More Than a Year Ago.

That penny more a year is by hour, in “real” inflation-adjusted terms. The calculation is from the BLS.

Nonetheless, the Fed is not happy with wage destruction. Various Fed presidents seek still higher inflation.

Inflation Targeting

Instead of using an inflation target of 2%, San Francisco Fed President John Williams proposes the Fed use a price-level target, that would allow inflation to run higher during expansions to make up for prior shortfalls.

We need that discussion, but in the opposite sense, because the Fed’s insistence inflation in a disinflationary world has seriously harmed median and average wage earners.

Occupational Employment Statistics (OES) from the BLS supports this view.

The following charts are from OES data downloads at the state and national level coupled with additional CPI data from the BLS.

Data for these charts are from May 2005 through May 2016. Those are not arbitrary dates.

The latest OES data is from May of 2016 and prior to May of 2005, the OES used varying months. Having all yearly data from May allows easy comparison of wages vs. year-over-year CPI measurements.

National Hourly Wages

Wage Differentials Mean vs. Median Hourly Wages by State

Every month, analysts track the monthly jobs report for “average” wage increases. Such analysis is misleading because most of the benefits go to the top tier groups.

This behavior is not unexpected, but it makes it very difficult for the bottom half of wage earners, who do not own a house, to buy a house.

Who Can Afford a Home?

The median wage rose from $14.15 in 2005 to $17.81 in 2016, a percentage increase of 25.9%.

The median new home price rose from $228,300 in 2005 to $335,400 in 2016, a percentage increase of 46.9%.

Rising Tide Lifts All Boats?

Some claim that a rising tide lifts all boats but, the median wage earner is falling further and further behind. This contributes to asset price chasing and “better buy now” philosophies as happened in the housing bubble years.

Inflation-adjusted charts show the situation is even worse.

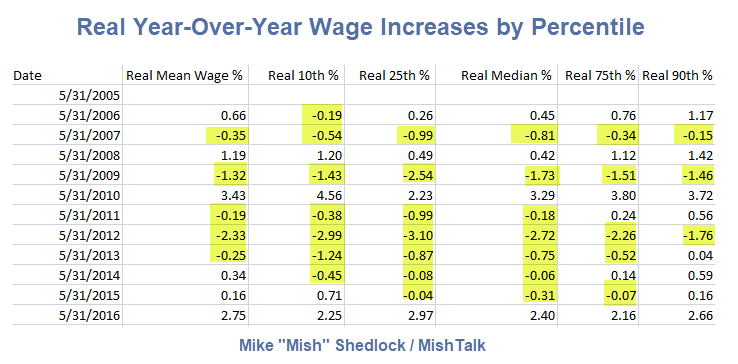

“Real” Year-Over-Year Percentage Increases

The chart shows “real” inflation-adjusted median wages declined in 2007, 2009, 2011, 2012, 2013, 2014, and 2015.

Mean inflation-adjusted wages declined “only” in 2007, 2009, 2011, 2012, and 2013.

Disturbing Results

Congratulations to the top ten percent whose real wages rose 8 times in 11 years. At the 75th percentile level, the score is 6-5.

It’s simply too bad for the median and bottom twenty-five percent whose real wages fell seven times in 11 years.

Don’t Blame Corporations

Many blame “greedy” corporations for wage stagnation.

Corporations have a responsibility to do what is best for shareholders, not employees. Sometimes those interests align and sometimes they don’t.

Don’t Blame Minimum Wage Laws

Minimum wages are also not the problem.

There is no reason to expect minimum wages to keep up with home prices. Home prices are not even in the CPI.

The Fed ignored rising home prices from 2003-2006, and they did it again recently. Central banks fail to learn from past mistakes.

Asset prices are in another massive bubble with plenty of blame to share.

Blame the Fed, Congress, Nixon

- Blame Nixon for closing the gold window in 1972; that allowed Congressional deficit spending at will.

- Blame the Fed for insisting on 2% inflation in a technological price-deflationary world.

- Blame Congress for massive fiscal deficits every year.

- Blame fractional reserve lending for being the enabler of trillions of dollars worth of mortgage and other loans, constituting money borrowed into existence chasing rising asset prices.

- Blame the media and academics for parroting the ridiculous notion that there is a benefit to rising prices. In the real world, standards of living improve when goods are cheaper.

Price Deflation Not a Problem

The Fed desperately seeks more inflation, but a BIS Study on the Historical Costs of Deflation shows routine price deflation is not a problem.

According to the BIS, “Deflation may actually boost output. Lower prices increase real incomes and wealth. And they may also make export goods more competitive.”

Counterproductive Fed Policy

The Fed’s policies are extremely counterproductive. To produce 2% inflation in a price-deflationary world, the Fed helped inflate asset prices to the extremes seen in 2007, 2000, and 1929.

Another Fed-induced asset-price bust is baked in the economic cake.

Meanwhile, a debate is taking place why economic growth is so low.

Secular Stagnation Thesis

In 2014 economist Larry Summers proposed Secular Stagnation is what ails the economy. Summers proposed “It may be very difficult for investment to absorb all saving.”

In 2017, Summers doubled down on his secular stagnation thesis. He blames austerity for the lack of inflation. His purported cure is more public investment.

Savings Glut Thesis

In 2005, former Fed chairman Ben Bernanke proposed economic growth was slow because of a Savings Glut.

Bernanke defines the glut as an imbalance between savings in China and consumption in the US.

Quick Rebuttal of Bernanke, Summers

To Larry Summers, I suggest that deficit spending is out of control globally. If more public spending was the answer, Japan would be the shining beacon of global excellence.

To Ben Bernanke I say, “Let’s not confuse “savings” with monetary printing. In the classic sense, savings = production minus consumption.”

The bulk of what’s been “produced” is dollars out of thin air, yuan out of thin air, euros out of thin air, and yen out of thin air.

In their analysis of “savings” both Summers and Bernanke ignore the massive buildup of debt that has occurred.

To the extent there is an imbalance between the wealthy and not wealthy, Fed policy exacerbated the problem.

History Lesson

The Fed bailed out the banks in 2000. At that time banks were troubled by soured dotcom bubble loans and loans to foreign countries like Argentina.

The result was a housing bubble, as Greenspan kept interest rates too low, too long.

In 2009, the Fed bailed out the banks when the housing bubble burst.

Since then, the Fed’s inflationary policies benefited the asset holders, the banks, and the top 10% of wage earners at the expense of everyone else.

Current Account Balance

Credit Explosion

Here is an excellent article on President Nixon: The Man Who Sold the World Fiat Money.

Prior to Nixon’s closing the gold window, countries could not run massive fiscal deficits for years on end without hiking interest rates.

Summers believes we need still more public spending stimulus. Japan provides convincing evidence that Summers’ thesis is false.

Discussion Needed

The Fed’s inflation policies are contrary to BIS findings, contrary to common sense, and contrary to the real-life results of median-wage earners falling further and further behind.

Please, let’s have a genuine discussion regarding the Fed’s inflation policies.

That discussion needs to incorporate ideas outside the Fed’s “group-think” box of more inflation, secular stagnation, and savings glut theories, all of which are easily proven wrong.

Discussion Rejected

The Wall Street Journal rejected this Op-Ed submission via a robot or a non-thinking person imitating a robot.

I know this because I sent in an inquiry to Editorial Features Editor, James Taranto, asking to speak with him about the rejection, and guess what.

My short Email request to speak to Taranto, not a submission, received the identical rejection notice. Thank you WSJ!

My submission title was “Fed’s Inflation Policy Destroys the Median Wage Earner“. It started with the discussion of inflation targeting. The wage acceleration mirage and the BLS penny admission happened after my op-ed submission.

At least the WSJ responded. The Financial Times, which claims to get get back within three days, didn’t bother.

Mainstream media does not want to discuss what’s happening and why. They already “know”. Nearly everyone but the Austrians believes “secular stagnation” is caused by “savings gluts”.

Besides, criticisms of the Fed, Larry Summers, or Ben Bernanke would ruffle too many feathers to be published.

Mike “Mish” Shedlock

http://pasutri-makassar.com/jual-hammer-of-thor-asli-di-jogja/

http://vimaxmedan.xyz

http://vimaxmedan.xyz/obat-hercules-di-medan.html

http://vimaxmedan.xyz/obat-pelangsing-di-medan.html

http://vimaxmedan.xyz/obat-erogan-medan.html

http://vimaxmedan.xyz/celana-vokoou-medan.html

http://vimaxmedan.xyz/obat-testo-ultra-medan.html

http://vimaxmedan.xyz/develope-sex-medan.html

http://vimaxmedan.xyz/obat-hermuno-di-medan.html

http://vimaxmedan.xyz/titan-gel-medan.html

http://vimaxmedan.xyz/anabolic-rx24-di-medan.html

http://vimaxmedan.xyz/obat-kuat-forex-di-medan.html

http://vimaxmedan.xyz/obat-vimax-di-medan.html

http://vimaxmedan.xyz/obat-viagra-di-medan.html

http://vimaxmedan.xyz/obat-kuat-asli-di-medan.html

http://vimaxmedan.xyz/obat-perangsang-wanita-di-medan.html

http://vimaxmedan.xyz/obat-perangsang-asli-di-medan.html

http://vimaxmedan.xyz/jual-semenax-obat-penyubur-sperma-di-medan.html

http://vimaxmedan.xyz/tattonox-obat-penghilang-tatto-di-medan.html

http://vimaxmedan.xyz/jual-selaput-dara-buatan-asli-di-medan.html

http://vimaxmedan.xyz/alat-bantu-vagina-center-flashlight-di-medan.html

http://vimaxmedan.xyz/jual-vagina-getar-suara-silicon-di-medan.html

http://vimaxmedan.xyz/boneka-cantik-full-body-silikon-asli-di-medan.html

http://vimaxmedan.xyz/jual-penis-getar-goyang-elektrik-di-medan.html

http://vimaxmedan.xyz/jual-penis-mutiara-getar-putar-di-medan.html

http://vimaxmedan.xyz/jual-penis-ikat-pinggang-silicon-di-medan.html

http://vimaxmedan.xyz/toko-penis-tempel-jumbo-silicon-di-medan.html

http://vimaxmedan.xyz/distributor-kondom-sambung-jumbo-di-medan.html

http://vimaxmedan.xyz/distributor-kondom-duri-silicon-bergerigi-di-medan.html

http://vimaxmedan.xyz/jual-kondom-getar-silikon-di-medan.html

http://vimaxmedan.xyz/distributor-vakum-pembesar-penis-di-medan.html

http://vimaxmedan.xyz/toko-pro-extender-alat-pembesar-penis-di-medan.html

http://vimaxmedan.xyz/alamat-viagra-100mg-asli-usa-di-medan.html

http://vimaxmedan.xyz/toko-kianpi-pill-penggemuk-badan-di-medan.html

http://vimaxmedan.xyz/alamat-jual-grow-up-asli-di-medan.html

http://vimaxmedan.xyz/alamat-obat-forex-asli-di-batam.html

http://vimaxmedan.xyz/toko-hammer-of-thor-di-banjarmasin.html

http://vimaxmedan.xyz/jual-titan-gel-asli-di-bekasi.html

http://vimaxmedan.xyz/jual-titan-gel-asli-di-jakarta.html

http://vimaxmedan.xyz/alamat-hammer-of-thor-di-medan.html

http://vimaxmedan.xyz/blog/obat-kuat-di-palembang

http://vimaxmedan.xyz/blog/alat-bantu-sex

http://vimaxmedan.xyz/blog/pusat-obat-pembesar-penis-di-palembang

http://vimaxmedan.xyz/agen-vimax-asli-di-medan

http://vimaxmedan.xyz/alamat-hammer-of-thor-di-bogor

http://vimaxmedan.xyz/hammer-of-thor-asli-di-cibinong

http://vimaxmedan.xyz/obat-hammer-of-thor

http://vimaxmedan.xyz/obat-kuat

http://vimaxmedan.xyz/jual-anabolic-rx24

http://vimaxmedan.xyz/toko-hammer-of-thor-di-batam

http://vimaxmedan.xyz/toko-hammer-of-thor-di-cikarang

http://vimaxmedan.xyz/toko-hammer-of-thor-malang

http://vimaxmedan.xyz/toko-hammer-of-thor-di-pekanbaru

http://vimaxmedan.xyz/toko-hammer-of-thor-di-surabaya

http://vimaxmedan.xyz/toko-jual-vimax-asli-pekanbaru

Don’t see a return to gold-based currency any time soon – the world is too far into the “fiat money backed by nothing” experiment to go back… In feudal times, we had 3 classes: Rulers, their Advisors/Soldiers and Serfs. After a temporary period driven by rapid innovation, we’re slowly but inevitably moving back towards the same system… At least that’s what’s Fed’s policies will accomplish… The only objective of the Rulers in the new world would be to pay the serfs just enough to keep them from revolting!

I’d also add these to the “blame list”:

1) Democrats for passing Obamacare

2) Republicans for not repealing it.

Every single bit of my raises (and more!) since 2012 has been eaten up by health insurance costs. Between premiums and deductibles, I’m out $20,000 per year for family health care before I see any benefit.

The solution to “difficulty in selling a home” is lowering the price. Anything will sell if its priced right and the “right price” should be dictated by the same mechanism which is used to determine one’s wage in the unsubsidized private sector: the free market. Of course, free market would mean lenders are competing with each other for good customers and they take the loss if the loan goes bad. Such a lender will ensure that the home is affordable because they want to get their money back with interest. However, today our country essentially has just one big bank known as the Federal Reserve and this thing has vacuumed up 1.8 trillion in mortgage backed securities. Does the little feeder bank have a bunch of goody two shoe borrowers dutifully making their monthly payments (dare we call them “suckers”?). “Nice job little bank! Keep the profits!” “What, you have some selfish borrowers who are walking away from their home after not paying the mortgage for 4 years?! Well, give the bad paper to us! The important thing is to capture more suckers!”

“~I’m being yelled at sorry can’t pull all this” – Tell whoever is yelling at you to stop!

@Carl_R

All things that follow from a reduction in systemic theft, are good things. Fractional reserve lending, when, as today, ultimately underwritten by third parties (via the Fed), is nothing but systemic transfer of wealth. To those engaged in lending, borrowing and speculation, from everyone else.

Lessened access to mortgages, in markets where supply is artificially constrained as is almost all housing markets today, would result in lower prices for the same house. Or more house for the same price. More for less is quite obviously a good.

As for ease of resale, lower prices would make up for lessened access to mortgages. Resale may well end up easier, as there is less possibility of being trapped “upside down.”

Thanks for that link, thimk. I added a link to it in the article.

It’s certainly true that in the absence of fractional reserve lending, mortgages, as we know them, would not exist. People would have to rent until they could save up enough to pay cash. It would also be much more difficult to sell a home, so they would tend to stay in the same families for generations. Are these good things, or bad?

I added two more points, one snow-dog mentioned and I have discussed many times before. 1. Blame fractional reserve lending for being the enabler of trillions of dollars worth of mortgage and other loans, constituting money borrowed into existence chasing rising asset prices. 2.

Blame the media and academics for parroting the ridiculous notion that there is a benefit to rising prices. In the real world, standards of living improve when goods are cheaper.

One thing thats not clear, when you speak of wages you assume the employer employee relationship, but very much more work is now independent contractors. City bus drivers are forced into being contractors, does this affect wages or something else, and also when a person draws a wage, there is the employers cost of the “package” of benefits, which is always lower with contractors. Contractors may get paid a bit more but they have no “package”. So are we stuck here counting last centuries wage employees and ignoring the change to workplace personnel?

FASB was told by congress to allow banks to LIE about the value of their assets, or else.

“Blame the Financial Accounting Standards Board (FASB) for their preposterous Ruling 157 which created the mark-to-model dystopia we’ve been mired in ever since.”

“How the Fed’s Inflation Policies Crucify Workers in Pictures” A group of congressmen representing farming districts, went to speak to Paul Volker about how Volker’s FED policy was hurting them. Volker’s response- they’re not my constituents. When savers were crushed under ZIRP, Janet Yellen said savers wear many hats, in order to rationalize not caring about people who were not her constituents.

You left one out Mish. How it is all hidden. Accounting. For corporations it is the valuing pensions on static 7% expected returns, non-GAAP write-offs, and much more. For banks, it was mark-to-wishes and interest on excess reserves. For the economy it is CPI modifications in the 90s that knocked close to 1% off OER, eliminated car price inflation, and added technology that tells us that you are really only paying $450 in 2006 dollars for that $850 iphone in 2018. Over time, it adds up.

As long as simply printing George Washington’s head on a sheet of paper, does not create any real value on its own, The Fed cannot create wealth.

As long as the above money printing increases the value of assets, it makes owners of assets wealthier.

Combine the two, and try figuring out what that necessarily must do, to the wealth of those who does not own assets.

Things aren’t any more complicated than that. The rest is just obfuscation. Whether willful or out of ignorance.

Excellent points. Agree with your overall thesis, but I certainly wouldn’t let corporations off the hook as a culprit in this race to the bottom, winner-take-all setup. Many of those corporations are pathological in their pursuit of the exploitation of labor for the sake of profit and padding executives’ absurd compensation structures, compensation structures that often resemble elegant accounting control frauds. Nonetheless ,the Fed is a primary culprit/enabler of this system, a system built on predatory capitalism, perpetual inflation and the lies that are continuously floated to justify it.

“To find out who rules over you, simply find out who you are not allowed to criticize.” Voltaire Wouldn’t that be the Fed Res.?

I respectfully disagree with you about the cause. First of all, you let corporations off the hook, saying that they owe a duty to their shareholders, not their employees, which I agree with, by the way. Then you blame the Fed, and treat them as if they owe a duty to the employees of America. The Fed is not even a branch of the government! They are a part of the banking system, and they have a core responsibility to do what is best for the banks. Yes, the Chairman of the Fed is a Presidential appointee, but that doesn’t make the Fed a part of the government.

Even more seriously, you treat this as a problem that the Fed can solve. They can’t solve it because the problem is unsound Fiscal policy, and an economy burdened with regulations. When the government is totally fiscally imprudent, there is no policy that the Fed can adopt that will not lead to disaster. The fact that the Fed has been able to keep things from total destruction is a credit to them. They can’t keep it up forever, but I do sit back and marvel sometimes at the fact that they’ve been able to keep things going for so long, and wonder how much longer they can keep it up. I’m guessing 20 more years at the max, by which time a combination of events will bring this chapter of history to a close.

Surely the Fed’s policies since Bernanke addressed the GFC have been about saving banks (and with them the financial system) and of course it could only do so by inflating asset values, thereby to avoid obliging banks to suffer material write-downs and insolvency. Workers’ wages are just the collateral damage – and a price well worth paying, I am sure the Fed and its friends would say. The obsession with inflation is surely just the means of continuing to justify what increasingly looks like a reckless course of action.