Do producer prices eventually feed into consumer prices? If so, what’s the lead or lag time?

The Wall Street Journal article Why the Inflation Picture Looks Starkly Different for Businesses and Consumers got me thinking about these questions, and I do not believe they came up with the correct answer.

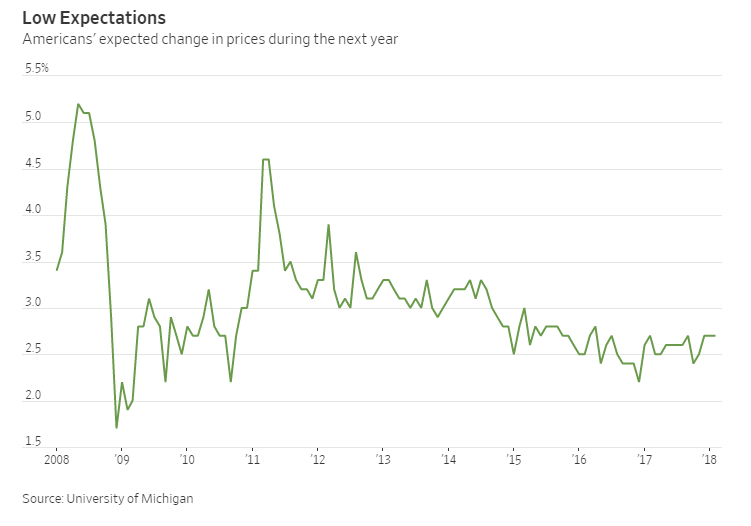

This month consumers said they expected a 2.7% rise in inflation over the next year, a level unchanged since December, according to the University of Michigan’s latest sentiment survey.

Other survey data indicate businesses are feeling inflationary pressures. Take, for instance, the rising percentage of executives in the Institute for Supply Management’s manufacturing survey who say they’re paying higher prices for materials: In January, 46.6% reported higher prices, up from 42% a year earlier.

Households’ inflation expectations tend to lag behind the behavior of inflation itself, which means as consumer prices rise, inflation expectations for this group should rise, too, said Michael Pearce, economist at Capital Economics.

“We’ve seen pickups in producer-price inflation before that haven’t really fed through to higher consumer prices, but there are good reasons to expect that the story this time around could be a bit different,” Mr. Pearce said. This, he said, is because a whole slew of factors are converging to put pressure on business prices and ultimately consumer inflation, a divergence from some past patterns when oil was the main driver.

Lagging the Leader or Noise?

The above chart is easily creatable in Fred. Here is a longer term view.

Cope PPI vs Core CPI

The overall correlation seems easy to spot, but it was far stronger prior to 1988. Since then, movement seems somewhat random.

I expected the divergences to be oil-related, but they do not all seem to be.

Random Fluctuations in Core CPI

The above chart compares four measures of inflation: Core CPI, Core PPI, All PPI, All CPI.

If there is a lead-lag effect on core cpi vs core PPI, I sure do not see it. Core CPI has been remarkably steady.

Highs and Lows

There were four instances in which core CPI was the highest measure of inflation and four instances in which it was the lowest.

The one pattern that holds is that core CPI was at the lowest when overall PPI was the highest, and vice versa.

However, the trends do not alternate.

Three of the four instances where core CPI was the lowest followed the great recession, and three of the four instances where core CPI what the highest were prior to the great recession.

Regarding Inflation

The above discussion pertains to inflation as the Fed and BLS sees it, not as the average guy on the street attempting to buy a house or pay off student loans sees it.

Inflation is rampant in asset prices, and the Fed cannot see it.

My definition of inflation is as follows “Inflation is an increase in money supply and credit, with credit marked to market“.

This is how the real world works in a fiat credit-based system.

My definition is not easily measurable, but neither is the CPI.

There is no such thing as an average basket that makes any sense, especially when the basket excludes home prices and assets.

Based on my definition, inflation is high and rising even if we cannot put a specific value on it.

It’s been rising since March of 2009 when the FASB suspended mark-to-market rules.

Why marked-to-market?

Even if it is not directly measurable, banks know if they are capital impaired. In such cases they will not lend. If they do not lend, the credit bubble dies and deflation ensues.

Looking Ahead

When the next recession hits, asset prices will collapse and loans based on those assets will sink, if not collapse. Consumer prices will likely follow.

Once again, this is how the real world works in a fiat credit-based system.

The Austrians, in general (not this one) made a huge mistake in believing the expansion of money and credit would lead to higher consumer prices.

However, the Austrians are correct in that the seeds of demise have been planted.

Meanwhile, the monetarists at the Fed and the Keynesians who seek still more stimulus are oblivious to the entire discussion.

Debt Deflation Coming Up

I expect another round of asset-based deflation with consumer prices and US treasury yields to follow.

Mike “Mish” Shedlock

http://pasutri-makassar.com/jual-hammer-of-thor-asli-di-jogja/

Hi Mish,

Thank you for an outstanding blog that I have read in several years. Do you think US followed by Europe will end I something like Japan, with zero interest and falling asset(house)prices for 10-20 years. Is another round of QE possible (and how should more of the same change anything). I don’t see any “easy way out”, do you? – or what is your base scenario? (We have plenty of asset inflation I Denmark too)

For decades now more credit has been added to the system than has been removed, and the result is a cheapening, a steady drop in rates. Credit is money. Those who are betting on inflation are assuming a dramatic turn in policy.

+1. The over-riding forces may be deflationary but the response to a severe downdraft in asset prices is going to be money-printing on another scale entirely. Orders of magnitude larger than anything in the recent past.

Mish, I know this is off topic but what do you think of Jeremy Rifkin?

Does the suspension of mark-to-market also apply to new apartment buildings? Seems wherever I go in this country (USA), there are brand new “luxury” apartments that are very expensive and only partially filled. I’m thinking somebody must be taking a bath with their investment gamble, but if it’s a bank that gets to say “Well, we are only generating XX amount now, but “our financial model” shows that in 10 years, we’ll be making YY, so our bank is still solvent!”, then they will always just charge what they want.

100 years ago, anarchists bombed banks. Now the banks are the anarchists (i.e., entities who don’t play by set rules – or change them so they always win).

the longer the period of time the more randomness kicks in – short time frames more likely to not be random

LT Debt/nominal GDP + the CPI can explain. The US treasury never failed paying interest, but rarely cut the the principle. The growth of GDP + inflation clipped the principle. When there is no/ little inflation or growth, it’s becoming difficult to block the growth of the principle and interest. Debt/ GDP is rising since 2000. It’s no longer in a TR and lately popping up > 100%. Next recession, when the GDP will fall, while debt rise, this ratio will get worse. The Fed have clue, but have no ammunition to fight it. The options are : higher debt or higher taxes. But there is another option…

If u start your first chart in 2008, u get a different result. Random is not random, it’s a typical back to a trading range after a bubble and a bubble collapse. The most important thing is the ==> length. Extend it and u will see why. 2008/09 are not the real bubble.

“However, the Austrians are correct in that the seeds of demise have been planted.” The bubble sows the seeds for the bubble to burst.