Here are three viewpoints, one is correct.

Is China Selling US Treasuries?

That’s what I typed into Google Chrome. Here’s the AI overview that came back.

China has been consistently reducing its U.S. Treasury holdings, with a 9-month selling streak as of early 2026, lowering its holdings to around billion, the lowest level since 2008. Key motivations include diversifying reserves away from the U.S. dollar, geopolitical risk management, and strengthening its currency. Atlantic Council +4 [AC + 4 others]

Key Details on China’s Treasury Sell-off:

- Reduced Exposure: China, once the largest foreign holder, is now the third-largest holder of U.S. debt, behind Japan and the UK.

- Long-Term Trend: Holdings have dropped from roughly

trillion a decade ago to around

billion, a decline of over 50%.

- Recent Actions: Reports indicate that Chinese regulators have advised local financial institutions to limit or reduce their holdings of U.S. debt due to market volatility and “concentration risks,” though this directive reportedly does not apply to state-level holdings.

- Market Impact: Despite concerns, the U.S. bond market has largely absorbed the selling due to robust demand from other nations, meaning this has not yet caused a major market crisis.

- Diversification Strategy: China is diversifying into other assets, including gold and other foreign currencies, reducing its reliance on the U.S. dollar-based system. Atlantic Council +9 [AC + 9 others]

Why They Are Selling:

- Geopolitical Risk: Concerns about the security of holding massive amounts of U.S. debt amid escalating tensions, especially after sanctions placed on Russia’s reserves.

- Currency Management: To support the yuan and shift away from a dollar-centric reserve portfolio.

- Market Volatility: Concerns regarding the rising interest rate environment and the stability of U.S. debt prices. Atlantic Council +4 [AC+ 4 others]

The Atlantic Council

On February 10, 2026 the Atlantic Council commented China’s warning on US Treasuries—and why its timing matters

Financial market turbulence

Markets have been unsettled by US President Donald Trump’s pursuit of Greenland, the unpredictability of US tariffs coupled with the Supreme Court’s impending ruling on their legality, and uncertainty over the administration’s dollar policy. Over the past month, the so-called debasement trade—selling or hedging dollar assets and buying precious metals—has gained momentum. Trump’s own comments seemingly endorsing a weaker dollar have added to the volatility.

Beijing has likely been watching closely how these developments fit into its long-term strategy. Over the past several years, China has been reported to be reducing its holdings of US Treasuries, falling from the largest sovereign holder to the third largest, behind Japan and the United Kingdom, although some of those sales may simply reflect assets transferred to other Chinese financial institutions and custodians in countries like Belgium. Other governments—including India and Brazil—have also been selling Treasuries.

At the same time, China is actively pursuing the internationalization of its own currency—a strategy aimed at reducing over time the US dollar’s central role as the primary global reserve currency. In a speech this summer, the Governor of the People’s Bank of China, Pan Gongsheng, explicitly stated that multipolarity was the government’s goal, with the dollar no longer playing such an outsized role in both the global economy and the use of financial sanctions. His deputy, Lu Lei, went a step further in December when he doubled down on China’s new cross-border payment systems, which are designed to operate outside Western networks.

A pointed message to Washington

Against this backdrop, how should one read the Chinese policy shift and its recent leak? Amid financial market turbulence, the Chinese government’s outreach to private financial institutions may have been primarily a reminder of the need to hedge at a moment of heightened uncertainty. It may also have been aimed at reinforcing policy guidance as Chinese exporters seek to invest the dollars they have amassed from the country’s massive export surge.

But it’s also possible the leak was intended as a message to Washington—or, more precisely, to Treasury Secretary Scott Bessent—in the wake of his recent comments about China. At a February 5 congressional hearing, Bessent spoke about “rumors of Chinese digital assets,” possibly backed by gold, that could be used to “build an alternative to American financial leadership.” Then, in a February 8 appearance on Fox News, he appeared to blame the current gold price volatility on China. “The gold move thing—things have gotten a little unruly in China,” he said.

Chinese investors have indeed been buying gold aggressively as they seek alternatives to the country’s decimated property market and rock-bottom interest rates. At the same time, the Chinese government has been a net purchaser of gold for the past fifteen months as it diversifies away from dollar-based assets. But China has hardly been alone in stocking up on bullion: JP Morgan estimates that global demand by central banks and investors for gold will average 585 tons per quarter this year.

Bessent’s decision to single out China may not have landed well in Beijing—especially coming so soon after meetings in Davos with his Chinese counterpart, He Lifeng, which reportedly went well. On February 9, Bessent announced “continued constructive engagement between both sides.” If this includes further talks with He Lifeng, they would likely take place ahead of the Trump-Xi summit in April.

But wherever the dust settles in the near term, the longer-term trajectory seems clearer. China’s ambitions to reduce reliance on the dollar will continue, and the Chinese government will keep finding ways to make life a little more difficult for the United States—and the dollar—wherever it can.

Rotation Theory

The Visual Capitalist

The Visual Capitalist comments Ranked: The Biggest Buyers and Sellers of U.S. Debt (2025)

Visual Capitalist Key Takeaways

- The UK, Belgium, and Japan were the three largest buyers of U.S. debt from November 2024 to November 2025, each increasing holdings by more than $115 billion.

- China reduced its U.S. debt holdings by $86 billion over the same period, leading all countries in net selling.

- Despite major shifts among individual countries, total foreign holdings of U.S. Treasuries rose to a record $9.4 trillion.

Are Foreign Investors Really “Dumping” US Treasury Bonds?

State Street Investment Management Asks Are Foreign Investors Really “Dumping” US Treasury Bonds?

While much has been written about the recent “dumping” of US Treasury bonds (USTs) by foreign investors, a reduction of UST holdings by foreign investors has been under way for more than two decades. The rise in the Treasury term premium has temporarily interrupted Treasuries’ ability to serve as a risk-off hedge, but the outlook for Treasury duration risk is nuanced.

Key Points

- The recent “Sell America” sentiment has triggered broad-based market volatility, but the key question remains: Does this reflect a temporary sentiment shift, or a longer-term reallocation of global capital?

- Despite rising concerns, US Treasuries remain the medium-term safe-haven, with limited near-term scope for foreign divestment.

- The tariff-driven sudden selloff appears technical, though amplified by fiscal worries, inflation pressures, and political uncertainties. These factors contributed to a higher term premium.

- While the term premium ebbs and flows, often influenced by tactical flows, a true structural “diversification but not divestment” reallocation flow out of US Treasuries would be a gradual, multi-year process.

- Our message to investors is that there is no need to panic on foreign “dumping” of Treasuries—many foreign holders are already underweight. Attractive carry and improving technicals could help restore long bonds’ safe-haven appeal.

- That said, if US fiscal issues remain unresolved, the term premium could widen further, posing a tail risk to the long end and weakening its role as a duration hedge (not our core scenario, but key tail risk to note).

Foreign Holdings of US Treasuries

Trading Economics: Foreign Treasury Holdings in the United States increased to 9487.10 USD Billion in February from 9289.40 USD Billion in January of 2026. Foreign Treasury Holdings in the United States averaged 6812.21 USD Billion from 2011 until 2026, reaching an all time high of 9487.10 USD Billion in February of 2026 and a record low of 4912.10 USD Billion in September of 2011. source: U.S. Department of the Treasury

Dumping Treasuries

Allegedly, dumping “a reduction of UST holdings by foreign investors has been under way for more than two decades,” even though holding have increased from 4912.10 Billion in September of 2011 to “an all time high of 9487.10 Billion in February of 2026” according to actual Treasury Data.

I would say that’s quite an achievement.

The AI view and the consensus view are essentially the same.

Consensus Nonsense

China Continues Dumping?

China will not continue dumping because it is not dumping at all. Rather, it’s masking what it is doing.

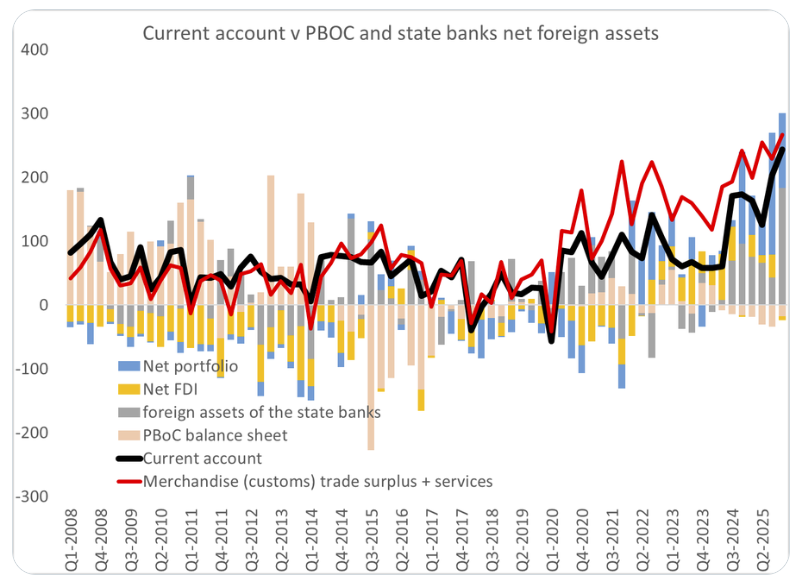

Brad Setser’s View

Brad Setser’s View

Brad Setser: Gonna keep repeating this until it registers — The PBOC may or may not be reducing its real Treasury holdings; it could just be moving out of US custodians .

But the state banks are clearly adding to their dollar portfolios, and thus indirectly funding the global accumulation of US assets.

Kathleen Tyson: These Chinese state banks? Are they buying through Caymans too?

Brad Setser: Have heard they prefer the British Virgin Islands … seriously read the aiddata paper on offshore Chinese lending to advanced economies and remember that the Chinese banking data shows rising claims from Chinese banks on other financial institutions and think a bit about global equilibrium conditions when China’s surplus is big and intermediated through ten state banks.

My view is essentially the same but with a bit more emphasis.

China is (not could be) masking treasuries in State Owned Enterprises (SOEs) and further masking in places like the Caymans, British Virgin Islands, and Belguim.

Pettis and Kathleen Tyson

Mish View

- China is masking Treasury holdings in State Owned Enterprises (SOEs)

- China is further masking its holdings in the Cayman Islands, British Virgin Islands, Belgium, Bermuda, etc.

- As long as the US keeps running trade deficits, foreigners will accumulate US dollars. They recycle those dollars somewhere, usually US treasuries or agencies.

- Dumping is impossible in aggregate because someone must hold every treasury issued 100 percent of that time.

Points three and four get to the heart of the matter, not mentioned above.

Mathematically, without dispute, someone must hold every treasury issued 100 percent of that time.

Who is that someone and how can anyone possibly dump them?

China could dump treasuries for gold. But who is the buyer of the treasuries. China could sell buy oil but what does the Mideast do with the dollars?

Every Month, Another Deficit

Meanwhile the US runs a trade deficit with China every month. In doing so, China receives US dollars. What does it do with them?

If China does do something with them, then what does the receiving entity do with them?

This key understanding is why foreign holdings of US treasuries are at a record.

Yet, the consensus view is countries are dumping US treasuries.

Conclusion

- There is no Treasury dumping (and mathematically cannot be in aggregate)

- The yuan is not about to replace the dollar as a reserve currency

- The petrodollar theory makes no sense (and never really did)

Points two and three are discussed in the related posts below.

Related Posts

April 20, 2026: What Does CFR’s Brad Setser Say About Petrodollar Myth and Reality?

“The glory days of the petrodollar are over,” says Brad Setser CFR fellow.

April 25, 2026: Mideast Dollar Funding Panic, Bessent Portrays it as Strength

I was asked to comment on US dollar swap lines to Mideast oil producers.

Sideline Cash Addendum

You cannot get rid of Treasuries or Sideline Cash by buying or selling.

Mish, it doesn’t matter that every bond has to be held by someone at all times. Every Argentinean Peso bond and stock has to be held by someone 100% of the time, when it is said that investors would “dump” them it means sell them at mass which will cause their value to plummet. The US is able to run trade deficits because foreigners are willing to buy its debt at reasonable yields, not because they have to.

You are 100% confusing “repricing” with dumping.

You also compare a reserve currency to a currency in hyperinflation many times

And you don’t seem to understand that Argentina had a lot of debt priced in US dollars.

And fourth you need to understand that it is impossible to dump anything anywhere because for every seller there is a buyer.

Grade F, F, F, and F

I respectfully disagree Mish. If you will be highly pedantic then yes, the dollar (or Peso for that matter) cannot be dumped. Doesn’t mean there will demand for it simply by this fact alone.

Dumping of Treasuries would be possible if the Fed was increasing its balance sheet. It could also be accomplished by the Exchange Stabilization Fund. I don’t think either is occurring at the moment.

Foreign holdings of Treasuries are going up because total issuance of Treasuries is up. The United States doesn’t have enough savings to buy all the issued Treasuries.

Brad Setser is very knowledgeable. See this interview. https://youtu.be/HEY4Z_T1nTc?si=ZrpwoQJrLzAtc5ng

What Mish is correctly describing is Econ 102. It’s shocking how the bar has been lowered by personality hires and girl bosses who are consistently secure in their uneducated opinions. This is a symptom of decay, among others.

Excellent analysis, Mish. Thanks

China is not de-coupling from USD.

Just de-risking and hold both treasury and gold.

logic and common sense – Every country wants to trade with US happily and keep USD and treasury as long as US keeps running trade deficit.

“Dumping is impossible in aggregate because someone must hold every treasury issued 100 percent of that time.”

But what if that “someone” is the Fed?

Depends on what it bought (ie what was the rate) and the price it paid.

If you can buy back your own debt at 50 cents on the dollar that effectively means you got your debt paid off at half price.

The Fed pays interest to itself and makes money on its circular investment.

Our banking system is a thing of beauty. Without it, we would be sucking mud.

Like a shill at an auction

It’s interesting that the bottom 3 (or top 3) depending on your perspective “dumpers” of treasuries are Brazil, India & China. Isn’t that 3 out of 4 BRICS? Russia not included because I guess they’re done buying altogether?

In any event and more important news, Jun Brent at $107 as I type this 🙂

Oh and this little gem of news.

https://www.cnbc.com/2026/04/27/china-industrial-profits-march-iran-war-oil-shock.html

China industrial profits jump 15.8% in March despite Iran war oil disruption.

Wasn’t this whole Iran war thing a way to cripple/starve China? How about them tariffs? Lol.

I think the key is looking at the TBill auctions. If the auctions are taken up on a reasonable basis (ie. lots of bidders bidding up the prices) then there is little to be concerned about. Who really cares who is buying as long as someone is buying and it appears that the auctions are functioning normally at this point. I do expect things to get difficult someday. It is likely pretty difficult to keep $39T balloons in the air at the same time (even if some of the debt is internal). Theoretically you can’t keep increasing the debt for ever.

Maybe this is getting above my intelligence level, but to my mind there seems to be a degree of discrepancy between the way this article is pointing and the way the article “Mideast Dollar Funding Panic…” is pointing. I do realize that in markets, and in other things, different indicators can point different ways. But do you have a summary: can you say which indicator is most important?

The mid east funding panic is because those middle eastern countries are not selling any oil due to the war. No oil sales, no revenue. Yet those countries still have to make payments (the article correctly notes those middle east countries are not running large surplus’s anymore) for things they import (food, cars, medicine etc). So they are getting swap lines (money to pay for those imports rather than selling assets and those loans will be backed by illiquid assets like QE was here a few years ago). This is a short term issue assuming the war wraps up in a short time frame.

That’s totally different than who owns US treasuries (debt).

Yes, correct answer.

Yeah, try looking into tri-party repo where some would conjecture that Treasuries are not only “held by someone”, but “that someone” might just happen to lend the same Treasuries out multiple times…which works until it doesn’t.

“The U.S. tri-party repo market averaged about $3.1 trillion in daily exposures as of Q3 2025. This market plays a crucial role in providing short-term funding for securities dealers and banks.”

The Central banks of the West Asian nations attacked by Iran have been selling Gold.

The US would rather lend the GCC money than have them fire sale their US bonds – which would raise their yields.

Ah, thanks for that. That is the sort of motive I can understand.

I ask why the charade? Why would China need to care about such appearances?

The fact that China is changing the appearance of holding US dept is telling us that something has changed in China domestically, internationally, or both as it seems the way they are holding US debt seems to matter.

Is the Chinese government scared of it’s people’s opinion (it hasn’t been in the past)

Is there a reason for the Chinese government to try to hide it from the common person (if we can see this guise, so can the US gov.)

Does this difference in holding create a different dynamic in trading it?

Other?

This is a fascinating topic, one that speaks to geopolitical realities that every country in the world is beginning to appreciate.

The US wants to be EVERYONE’s financial intermediary, because it wants to know and control the purse strings of every country on the globe (ideally), but can’t (in reality). It’s a hard power approach that costs less than management of a colonial empire.

If you look at all of the resource acquisition invasions the US has undertaken, most notably Iraq and Venezuela, it immediately made their oil flows payable through the US Treasury. This gives the administration leverage over who runs the country and what policies are implemented. The US can cut off access to that money should any ‘un-American’ outcomes arise. It’s also the same set up the Trump administration wants with Iran.

China, Russia, Brazil, and every other country interested in maintaining sovereignty sees this. They see that any resources or assets subject to US custodianship can be seized or related payments blocked, putting those assets at RISK (in the financial sense of total loss). By moving those assets from US custodianship to neutral 3rd party custodianship (presumably with some shadow accounting to mask true ownership), they reduce that risk. It’s why those holdings are showing up in Belgian and Cayman Island accounts, banking disclosure laws.

Some de-dollarization is justified, given the US Treasury has increasingly weaponized the financial system over the past 10 years, but these countries still need to hedge, and transact, with US assets.

A corollary is that every country that desires sovereign control of assets now has an incentive to participate in a parallel system, just to avoid the RISK. How do they participate without flagging this to the US, assuming they’re not looking for a hard break?

Yup

US halts Iraq dollar cash shipment after militia strikes, sources sayhttps://www.reuters.com/world/us-blocks-iraqs-dollar-shipments-squeeze-iran-backed-militias-wsj-reports-2026-04-22/

And technically as the article points out, Iraq’s oil revenue is routed to the Federal Reserve Bank of NY and not to the US Treasury.

I have read that the Chinese turn those dollars into construction projects around the world. Why in the heck would you buy treasuries when it’s obvious the US Government is bankrupting itself? They have enough and wouldn’t be surprised to see them continue dumping. I read a book about the Weimer Republic and folks couldn’t wait to get rid of their currency before it lost value to inflation.. I shop regularly at the grocery store and online and everything is up. Inflation everywhere. You want a real scam? See the markup the American Government has on their gold and silver at USMINT.gov. Huge markup. The only good point with them is you avoid state taxes if your state taxes you on bullion and get proof coins if shiny is a big deal for you.

Interesting article. Especially with China working on some gold backed crypto and not Bitcoin or other scam coins. Please note there was a time when I thought BTC was a good idea. I like the idea of crypto that makes it difficult for governments to monitor, but I think they are just vehicles to transfer funds like Western Union, but have no inherit value. A gold backed one might encourage me to learn Chinese and find me a Chinese wife. 🙂 I’m outta here.

Gold backed yuan is ridiculous – never happen

Discussed many times. Search my blog for it.

AI crap

..China has been consistently reducing its U.S. Treasury holdings, with a 9-month selling streak as of early 2026, lowering its holdings to around billion, the lowest level since 2008.

Having to constantly refute nonsense is like having to counter folks’ continued use of the statement: “money is coming off the sidelines” when referring to equities. You ask “what did the seller get when they sold” and the discussion just goes nowhere…so frustrating.

An astute observation

Sideline cash theory is buying stocks without the money going to the seller of those stocks.

This is selling bonds without the bonds going to a new buyer.

Well, that is just short-cut for saying that buyers are more motivated to buy than sellers are willing to sell.

Most people intuitively understand what “money coming off the sidelines” essentially means. Except for the pedants and pontificators, that is.