New Home Sales Defy Expectations and Retreat in October

Mortgage News Daily comments New Home Sales Defy Expectations and Retreat in October.

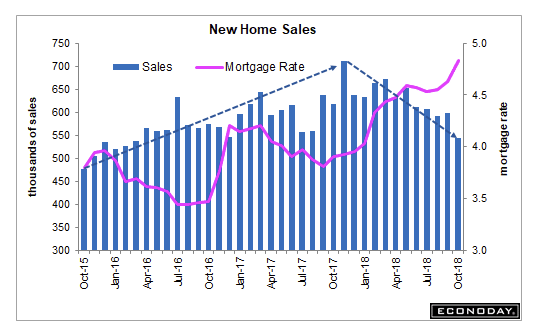

New home sales were expected to make a strong showing in October; the consensus of analysts polled by Econoday was for a sharp increase from the September level of 553,000 to 575,000 units. Instead, there was a steep decline, amplified by a major upward revision to the September estimate.

The U.S. Census Bureau and the Department of Housing and Urban Development estimate that October sales of newly constructed homes were at a seasonally adjusted annual rate of 544,000 units, falling well below the lowest of analysts’ projections. The result was a decline of 8.9 percent from the restated September rate, an upward revision to 597,000 units.

The September revision gave new home sales their first uptick since May. With that single exception sales have declined steadily from the 653,000 estimate for that month and the October number lags the 618,000 sales pace in October 2017 by 12 percent.

By Region

- Northeast: Down 18.5 percent for the month and 46.3 percent compared to a year ago.

- Midwest: Down 22.1 percent for the month and 16.7 percent compared to a year ago.

- South: Down 7.7 percent for the month and 11.6 percent compared to a year ago.

- West Down 3.2 percent for the month and 1.3 percent compared to a year ago

Peak

New home sales peaked at 712,000 units in November of 2017 on a hurricane rebuilding surge.

Sales have trended lower for most of 2018. The year-over-year numbers next month will be grim

Supply

At the end of the reporting period there were an estimated 336,000 homes for sale, an increase of 17.5 percent in the inventory year-over-year. This is an estimated 7.4-month supply at the current rate, almost a month more than was estimated for the September inventory. Only 74,000 of the available homes were ready for occupancy.

Oops. It appears builders were more than a bit too optimistic in building homes that no one wants or can afford.

Mike “Mish” Shedlock

You make a valid point.

DEFLATION

I don’t know whether to commend the shrewdness of the Republican Party or condemn the ignorance of the “analysts.” One of the stealth impacts of this year’s tax bill was the fact that in essentially eliminated all the tax benefits associated with home purchases by the middle-class. Tax benefits have always been a major incentive for home purchases; yet nowhere is it mentioned in the citations (or anywhere else, for that matter).

Correct. It is also an overlooked reason for the shellacking the Republicans took in the House races. Suburban, Republican congressman in California and the Northeast were almost entirely eliminated.

Three things have led to unaffordable home prices. Artifically low interest rates, the tax deduction on interest and govt backed mortgage insurance. It has been shown that the tax incentive was only a gift to builders as it allowed them to raise home prices. No other country allow interest deductions and we should not either. Also there should be no govt backed mortgage guarantees. This is not free market capitalism at work its govt giving gifts to a favored cause. In reality it just screws things up more and undeniable caused homes to be unaffordable. It also doesn’t help that we now are deporting the illegals who fill the jobs in the building trades that are so short on laborers.

And this is obviously bullish for the stock “market”. Bad news is good news once again, as the Fed will raise interest rates no more than another 25 bps before pausing and probably marking the end of this cycle.

Thats part of the problem if we can’t function economically with interest rates below what is normal, the economic expansion is built on quicksand. My first home purchase was at a 9% interest rate.

When interest rates go up faster than prices go down for a heavily leveraged purchase, this is what happens.

And if you were buying a home this year with an FHA loan or zero-down financing, there’s a good chance you joined the nation’s new crop of underwater borrowers.