Magnify Money asks How Much Does the Average American Have in Savings?

The question is irrelevant. The story is how unprepared the median person is prepared for retirement. On that score, the article does explain.

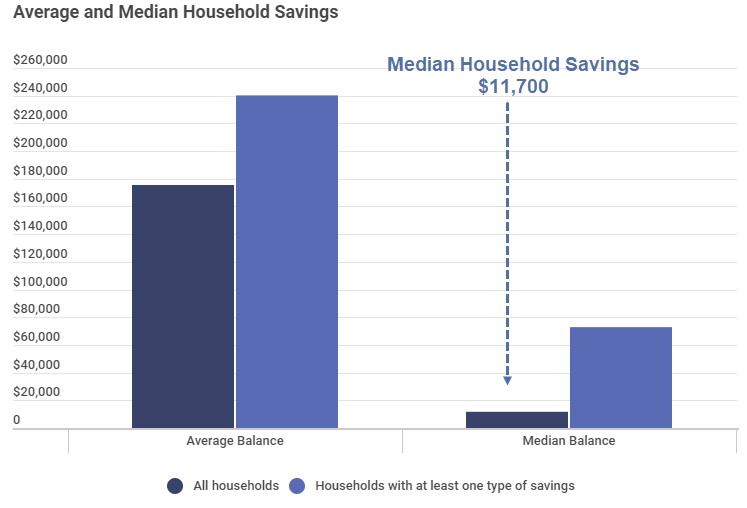

Stats

- The average American household has $175,510 worth of savings in bank accounts and retirement savings accounts as of June 2018.

- The median American household currently holds about $11,700 across these same types of accounts.

- The top 1% of households (as measured by income) have an average of $2,495,930 in these various saving accounts. The bottom 20% have an average of $8,720.

- Roughly 83% of savings are in located in retirement accounts like IRAs and workplace-sponsored retirement savings plans like 401(k)s.

- Millennials, who have just started their savings journey, have currently socked away an average of $24,820. Gen Xers have $125,560 in retirement savings. Baby boomers and those born before 1946 have an average of $274,910.

- 29% of households have less than $1,000 in savings.

Point number 2 is the most relevant point. 50% of household have less than $11,700 in savings.

Averages Lie

What’s wrong with averages? The Skew!

Average and Median Savings by Income Level

The top 1% of income earners have an average savings of $2.53 million and a median savings of $1.16 million.

That average affects people with no savings.

The median savings for 40% of households is zero. The “average” varies by income group but it is much higher.

The “middle” (40-60% of wage earners) median savings is $34,020 but the average is $65,830.

Age Level

This is where the stats get truly depressing.

The average “boomer” headed into or in retirement has $274,910 in savings.

What’s wrong with that?

Well, 50% of boomers have less than $24,280 saved up.

Averages lie.

Mike “Mish” Shedlock

The current system is doomed. It’s predicated on asset inflation while we are experience massive job deflation..

Are you in the bleeding heart camp or honestly the reality — most people have “little savings” especially young people (marketwatch.com & WBZ 1030 Boston have this bleeding heart obsession with millenials now) because they waste their money & blow it on frivolous crap because of the attitude of YOLO or “FOMO”. I mean anyone in Boston now see these college kids? some of the most entitled, coddled individuals who have the latest Macbook Pro, latest Iphone and of course Canadian Goose coats (at $1200 each) for the Winter. Ever see the parents — most are the same interchangeable, WASPY late Gen X or Boomer consumer drones who always have this look of shock when you give them the old school New York attitude to keep them in check.

I mean people spend now over $200 a month on cable & internet and another $150 a month to keep that latest Iphone X in service, $250 a month for gym membership (plus of course the dorky spandex outfits), $150 for “running shoes” (with the dorky spandex of course)… Marketwatch & WBZ 1030 still have this bleeding heart “wages trailing inflation” but practically everyone I know spends $2000 on rent alone and eats dinner out every night or spends $50 per person on Seamless web or Uber eats

Interesting about Millenials (that everyone seems to have this pathological obsession with).. They think people in their 40s are “old”, won’t hire anyone over 35, are only concerned with “fit” and only can think in terms of “groupthink” or “team”, and of course won’t associate with anyone who doesn’t have the latest Iphone, and most of the women are extremely cold, never smile with their hair tied up in a bun.

So 9 of us poor folk are sitting in a bar and in walks Jeff Bezos who today is worth $100 Billion. On average, all 10 of us are worth $10 Billion but the median net worth is still very close to zero.

thats why people are poor, they spend $100 at the bar, another $50 on Uber, have the latest Iphone, and of course the only ‘art’ they know is from that extremely ugly tattoo ink people have (that is inversely correlated with intellence and intellect but of course costs tens of thousands of dollars).

correct

Statistics certainly can be misleading, and are widely misunderstood. Definitions are important too. As Blurtman mentions, the definition of savings used here seems to exclude home equity. It also seems to exclude pensions — which have a large Present Value, and are much more significant for people at the lower end of the savings scale. And it ignores the functional value of social safety net programs which are tapped by those with no cash savings (eg Disability Payments, SNAP, etc). All things considered, the data is worrying but does not give a complete picture.

Of course, we all understand that most pensions are not going to be paid. Most government bonds are not going to be redeemed in real terms at anything like their nominal face values, thanks to inflation. Real estate and stocks are likely to decline in real value as the selling pressure from retired Boomers mounts. The true economic underpinning for individuals lives would be a booming economy with lots of opportunities to earn. Unfortunately, misguided trade policies have exported millions of jobs.

“Of course, we all understand that most pensions are not going to be paid. Most government bonds are not going to be redeemed in real terms at anything like their nominal face values, thanks to inflation.”

Let’s think this through. What is inflation? An expansion in the quantity of money (including credit.) More money rushes into the marketplace and bids up prices (rising prices are a symptom, right?) So what happens when the bond market and pension systems collapse? What are they but promises of future cash flows, i.e., they are expected to contribute (mightily) to the quantity of money (in the future.) But if they collapse (as seems inevitable) won’t that be deflationary, as in “deflationary collapse?” If there’s way less money in the system, shouldn’t prices collapse? (That doesn’t mean things are more affordable, BTW, it means people will be desperate for money, unlike now when “fog a mirror” credit is available.)

It certainly is misleading to talk about averages when income and savings inequality are as astronomical as they are in the US. It’s misleading and not a useful statistic. Making hay out of whether it’s a lie or not seems like a way to avoid addressing the topic. Most Americans do not have enough savings to retire or even to deal with a personal crisis.

The reason why its ‘astronomical’ is because everyone is conditioned to spend every penney they earn (plus any available credit) on consumer crap and designer clothing that they then post on Instagram or Facebook as a way of bragging about this conspicuous consumption gone made.

I take exception to the statement ‘averages lie’.

The numbers used calculate the average is accurate and true, Yes? Thus, the average is not a ‘lie’. False data was not used to make the calculations. The large discrepancy between the median and mean in savings is exactly why we have a mathematical way to describe median and mean. They are tools to help better understand groupings of number and you must know when and how to use them.

You take exception? LOL. Good for you! Never mind that you completely missed the point, which is that it is reported in a way that suggests all is well and which most people just take at face value. That said, your basic comprehension of statistics is impressive. If I could give you a gold star, I would.

If 50% of boomers have less than 24,300, 274,000 isn’t really average.

…but $274,000 is the average. It’s not a made-up number to mislead. If anyone is misled, it’s because they don’t understand the difference between median and mean. The fact that there is a magnitude of 10x between mean and median savings shouts the fact that we have a society of a few extremely wealthy people. Simple as.

It seems this is all part of the illusion. It seems many of us are drawn to a good illusion and this proves true for most people in their daily life as well. In some ways, it could be said that our culture has become obsessed with avoiding what is real.

We must remember that politicians and those in power tend to throw people under the bus rather than rise up and take responsibility for the problems they create. The article below looks at how we have grown to believe things are fine.

What do you mean by “throwing people under the bus”? Do you mean people screwing over others to get ahead?? Isn’t this completely normal now in the USA especially in any white collar corporate job and just in everyday life??

Clickbait story fails to mention home equity, the traditonal “savings acount” for the middle class.

Property taxes, inflation and the managed care industry are going to rob you (and me) of our home equity as we age. I see it very clearly. My property taxes went up 25% year over year as the youngsters float and pass bond issue after bond issue for new schools, football stadiums and waterparks. Future generations will look back on the era that is rapidly passing somewhat wistfully in that regard.

Your story shows why distribution curves are better than averages or medians.

Why should we assume, the statistics is to portray the true picture. In all probability not. Essentially use the statistics to paint the picture you want. When fraud is the business model to peddle something ( in this case to paint a picture of an economy with great savings) then simply twist the facts to tell your tale.

Mish, this is such a great point you make here.

We had a thread on another posting about graphs and how they can mislead. This is an example of how a good graph can be far, far better than a simple number.

The curves that describe income, wealth, and savings distributions (and other things of this sort) are exponential-ish curves. Think, 80-20 rule. A very few entities with very high numbers, lots of low numbers. Smooth transition from beginning to end. Average higher than the median.

With curves like these, even *thinking” about the average will send your mind off the rails. No graph? Use median. Cut people who use averages out of your reading list. You really want the graph. Watch out for various bar-charts and quin-tiles and such. They can be kludges grinding axes. Watch out for fancy analysis that, when you spend a few hours with it, you find someone secretly switched from an exponential/log view to a linear view and, in doing so, did the mental slight-of-hand equivalent of dividing by zero. Just get the raw data in a simple curve.

If you don’t have the graph, dollars to doughnuts you’ll end up in some kind of fantasy land.

I see those numbers are from the FDIC and the Federal Reserve. Do they consider ownership of businesses which have productive assets to be ‘savings’? Or is their definition of ‘savings’ merely cash deposits in so-called “savings accounts”?

Excellent Question!

Let me start with what I know: The definition of “saving” to the Fed is income minus expenses. Stock market gains and losses do not play into the alleged average “savings rate”.

For the purp[oses of the article, it’s different. And I do not know if they subtracted out credit card balances or mortgages. It may be in the article but I do not see it. And if not, the numbers are far worse than reported. I will contact them If possible.

But as I understand it the Fed does count monetary value sitting in stock accounts as “savings” (not affecting the rate, I understand.) If so, and if the Wilshire 5000 is a surrogate for total stock market cap, has “American’s Stock Savings Account” really gone from $8T to $30T in nine years?! This metric is utterly bizarre.

Yes. It is important to know the difference between average and median, especially in sample sets where extreme outliers skew the whole sample. You know the saying: “There are three kinds of lies: lies, damned lies, and statistics.”

Speaking of misused statistics, I have lost count of the news reports that roughly state, “Trump’s tariffs will cause higher prices (inflation) and that may force the Fed to tighten more than expected.” What sort of craziness is that? Tariffs are a type of tax that extract money from the economy and economic activity would likely be depressed by tariffs, not stimulated. Higher taxes are in no way the similar to higher prices caused by monetary injections. How can anyone say with a straight face that Fed will tighten more in response to tariffs? Surely the Fed’s economic models are not that broken? I would like to know your view.

I have stated my view: Short-term, tariffs will raise prices, Long-term tariffs will collapse trade: Net deflationary

What I meant was, what is your view on how the Fed will interpret the short-term increase in prices due to the effect of tariffs? Wouldn’t they understand that increased prices due to tariffs are not the same as increased prices due to easy money?

So far it hasn’t depressed economic activity. Retail sales and overall consumer spending is red hot with retail sales to soon hit 10% year over year. Wages especially at the bottom have risen significantly in the past few years. Ex. Someone making $8 in retail in 2012 would likely be making $15 per hour now in retail. Jobs paying $60,000 in 2012 would likely be paying someone $85,000 in Accounting, Finance etc. at the entry level now