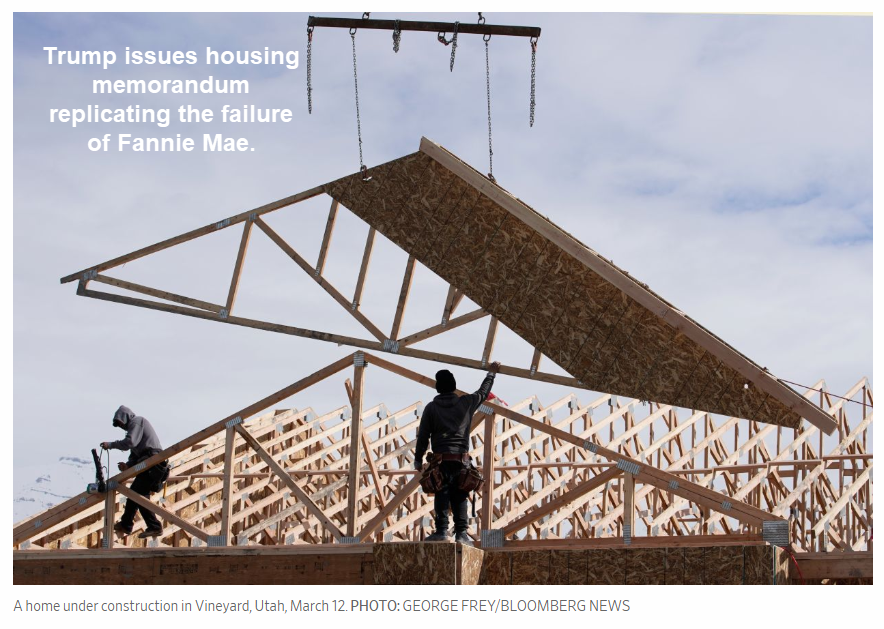

If you thought Trump would deregulate Fannie Mae and Freddie Mac you thought wrong. Instead of deregulating, he replicates the old rules and prepares another bust.

Please consider The Coming Trump Housing Crisis.

The Trump administration has finally turned its attention to housing policy. Unfortunately, the president’s Memorandum on Housing Finance Reform, issued last week, is a major disappointment. It will keep taxpayers on the hook for more than $7 trillion in mortgage debt. And it is likely to induce another housing-market bust, for which President Trump will take the blame.

The memo directs the Treasury to produce a government housing-finance system that roughly replicates what existed before 2008: government backing for the obligations of the government-sponsored enterprises Fannie Mae and Freddie Mac , and affordable-housing mandates requiring the GSEs to encourage and engage in risky mortgage lending.

An administration that believes in deregulation should do better. The Trump administration could have used its control over the Federal Housing Finance Agency—the regulator and conservator of Fannie Mae and Freddie Mac—to shrink their footprint dramatically over five to 10 years. This would be done through administrative action, reducing the size and types of the mortgages that GSEs could buy and opening larger portions of the housing-finance market to the private sector, which offers 30-year fixed-rate loans at rates competitive with the GSEs’.

Since 1992, this government intervention has been guided by the misconception that low down payments and high debt-to-income ratios will help low- and middle-income families buy homes. The resulting policies produced a highly volatile U.S. housing market, subject to enormous booms and busts. Its culmination was the 2008 financial crisis, in which a massive housing-price boom—driven by the credit leverage associated with low down payments—led to millions of mortgage defaults when housing prices regressed to the long-term mean.

Another Vote-Buying Monstrosity

These kinds of programs are popular with builders, political hacks, and economic illiterates who believe such programs help create affordable home.

The builders and hacks benefit but the public gets screwed.

Mike “Mish” Shedlock

“Another Vote-Buying Monstrosity”

There is the Big Money in politics. The democrats are always clamoring to get the money out of politics, but using the tax payers as a cash cow vote buying mechanism, won’t go away by curtailing campaign contributions by corporations and the wealthy.

RonJ: FYI Trump is a Republican…not a Democrat. From news article, I would be very surprised if he’s talked to a Democrate in a few months. House builders are NOT Democrats

Trump is now concerned with his re-election. Nothing else matters. The voters want peace but hate Russia. Since Trump turned warmonger without really starting new a war, his poll numbers have shot up. He can get away with violating international law in Palestine. Don’t know what will happen with Venezuela. Trump may save Korea for his re-election campaign.

But Trump has claimed the stock market so it’s his to lose.

Trump will be indicted when he leaves the WH so he has strong incentive to be President for life

That remains to be seen.

exactly!

When the “cost” of housing becomes unaffordable, it’s great when market-oriented governments come out to “help” prospective home-owners by giving them money, guaranteeing their loans, tax deductions for mortgage interest … anything other than the thought that house prices might drop if people can’t afford them and that financing is actually driving the price.

the Trumpster is the only ‘real’ Democrat in the whole bunch. I’ve been fruitlessly telling that to all from day one.

Has any of you viewed his mom in interviews? Ans: nope. He’s also a true mountain man from N Scotland. Very tough.

I’m fine with it, as long as we get access to his bankruptcy lawyers.

I should mentioned that as bad as Trump’s actions/beliefs are, they pales in comparison to what ANY establishment politician would do. It’s analogous to why foreign capital continues to flow into the US, no matter how anemic the economy and fraudulent the establishment, it’s still the healthiest horse in the blue factory. There is no perfect person or policy. Everything is relative, and this fact is understood by capital and the invisible hand.

Back to picking favorites among turds in a sewer….

I have said for a long time that trump is no conservative. He’s just a little less rabid than prior liberals. WE cannot go from peak liberalism to peak conservatism in one fell swoop. The herd simply cannot pivot that fast.

The Iranians did.

Iran under Pahlavi, was ran pretty much the way the West is today. Everything was done to prop up, enrich and insulate Tehran “society;” while regular people, traditional customs and morals were poopooed by shallow quips about how “we are more sophisticated now.” No different from current Western progressive ruling castes.

Over time, people got more and more fed up with the corruption, favoritism, privilege peddling and encroachment. Until, one day, they swung in a very decidedly conservative direction.

You need to remember Conservative in the context of a traditionally (at least for the past 1000 years) Islamic society, is very different from Conservative in the American context. If Americans could only double down on Jefferson to the extent the Iranians did on Muhammad, we may just start to be getting somewhere…..

The pertinent analogy to Iran, is that people didn’t just start woodshedding on the Koran out of the blue. But rather that they, slowly but steadily, came to see that the entire hairball of contrived lies they had been sold, about how “modernity” was supposed to be some giant leap forward from what had worked for centuries past; in reality was nothing more than a license for the rulers and their closest hangers-on, to rob and self deal to their hearts’ content. Again, no different from Western progressivism.

So, they went back to what had worked for their ancestors before. Or at least, something closer to it, than what the Pahlavi regime represented. And, once the ball got rolling, the ship was turned pretty darned quickly.

The US flywheel is much bigger than Iran and that is more than just a statement about US population of 330 mn being several time larger than iran 80mn ppl. In Iran, too few had anything to lose by rapid change. In the US, too many have too much to lose to agree with it. Remember, the debt has been incurred and now all we are trying to do is figure out who the Patsy is. Who can we pin it on, who can we burden it with. Someone is going to have to pay it, either creditors or debtors. But it will take time to figure out who that is going to be.

No one is going to pay it off, as the debts are too big. Govts never intend to pay off their debt, which is why they have always defaulted. The only other choice is debt-equity swaps, but govt is too stupid and self-absorbed to even entertain the idea.

As a matter of pure economics, someone will pay it. Either the creditor or the debtor. But all debts get paid by someone in the end. Just not always by the debtor. In a default, the creditor pays.

Yes, creditors will get a haircut, and since depositors are also lenders to the bank, with due diligence responsibility, they too will be groomed in the bail-in process.

Trump’s impact is debatable. While he may not have started as an establishment politician, he’s done his best to become one in a short time.

If Hillary had presided over these fiscally insane policies or tried to drum up new wars overseas, conservatives would be up in arms, rallying for change. Instead, when Trump won, many either went to sleep or dedicated themselves to defending him no matter what, just like people did with W until they couldn’t stand it anymore. There are still lots of Q-tards waxing philosophical about the finer points of Trump’s 4D chess game.

As we go forward, the promises of candidate Trump will become an increasingly distant memory.

The answer is very simple. He is running for reelection. He need s votes.

I really enjoy all the comments. All wandering why would he do that and what other country does that. I tell you the why: It is to get votes next election by giving a house to anyone with a pulse. The who: Socialist and populist countries. Now, I do not care about “Well Hillary would had been so much worst answers”. You all elected a Chavez deal with it

Trump’s BELIEF that this move is actually good for the economy is consistent with his BELIEF that more QE is needed. What he, and quite frankly, the majority of so-called economist, pundits, and CB’s fail to understand is it’s all about confidence. CB’s can hand over all the fabricated money they want to banks, but if banks can’t find enough qualified borrowers and borrowers are not confident to borrow, well, you get exactly what Japan, Europe, and the US have gotten – anemic to declining growth. And since govt largess (fraud, corruption, career politicians, taxes, fees, civil asset forfeitures, etc.) will only get worse as pension and interest expenses grow, confidence will continue to decline until the “reset” occurs.

Maybe, the Fed should go back to it’s original intent – provide capital to the real economy, by buying corporate debt during recessions, instead of funding the federal govt by buying treasury bonds. Maybe, the judiciary should equally enforce the rule of law, and CONgress install term limits. Who doesn’t think these actions will improve confidence and trust?

They desperately need more credit growth, because without it the economy implodes. The problem is that they are encouraging the growth of mortgage ownership, not home ownership.

As this cycle gets closer to the tail end, we’re already seeing more people at the margins overleveraging to keep up with rampant home price inflation. Easy to become an underwater homeowner in this environment, particularly if you don’t understand the game that is being played…

“..they are encouraging the growth of mortgage ownership, not home ownership.”

Probably the most concise, accurate and descriptive way of putting it, I have seen so far!

To any MSM hack reading Mish comments: Here’s your opportunity to be associated with originating/popularizing a snappy viral meme….

This story is complete BULL$HIT! Government should not be in control of these companies. They should be regulated at best. The government doesn’t own GM and all the other car companies that needed a bailout?

No company “need” a bailout.

Which, come to think of it, is just anther special case of nobody needs a government at all. Certainly not one with enough power and resources under command, to enable it to bail out anything.

Your delusional, do you have any idea what America would be without our government? Any country really. What are you a 14 year old basement dweller?

I am sure we don’t need banks and homeowners association as well?

It would be like the country half of Europe fled to, to escape governments similar to what is currently “our government.” IOW, it would be a free country.

You are actually more like 12. America was settled escape religious persecution. NOT to escape from government.

And who provided the muscle for that prosecution again? As well as the bans preventing people from defending themselves?

And wagon train who ever headed West, did so in search of a Pelosi they could be blessed to pay taxes to…..

What is your background? Are you typing this from a computer a in rubber room you are not allowed to leave?

Bubbles of increasing frequency approximate a straight line.

This is part of a long term “milking” plan of the treasury, leaving gigantic debt when he leaves office

They can’t possibly believe this is sustainable in the long term, especially given the similarity between this and what led to 2008. This means that Trump aims to intentionally blow a bubble that would ideally last just long enough to outlive his administration.

And to think people wonder why so many are bearish on the long-term outlook of the US!

The goal is to bail out idle, zero–value-add banksters and asset owners. Off the backs of taxpayers and others stuck doing something productive in exchange for paper which is then debased away from them.

Artificially keep housing scarce and expensive enough that the niggas have no choice but to keep picking cotton in exchange for a leaky roof over their heads. While excusing it, by claiming “they” “are responsible for” “their” debt…..

This has to be incorrect news it is that stupid. The govt should not be involved in housing at all. I am not sure what they do in other countries but I don’ t think they have 30 year fixed rate mortgages. I think in other countries Canada for one, the rate gets reset every five years. I don’t know if they have a Fannie Mae equivalent but I am thinking not. Still they have a housing bubble over there to.

If you have a central bank, and/or any zoning/land use laws restricting house building, and/or activity taxes (sale, income….) rather than property ones paying for the courts and police which protects real property rights, you already have a housing bubble. From there on out, you’re only talking matters of degree.

Yall ain’t seen nothin yet,come election time get ready for Stimulus checks 2.0 i,then massive stimulus package, free trump phones then some form of student loan forgivenessand wait for it…………across the board amnesty for illegals….no question asked.Don pullin out all the stops cause losing is not an option.

…And trump gets paid.

Remember folks, the lesser of two evils is still evil.

Zardoz = Genius

Housing lending has always been a problem, and it will continue to be a problem in the future because no one has ever come up with something that works, and I don’t think anyone ever will. When a bank issues the loan, they loan long (30 years) and borrow short (demand deposit). That crashed in the 1930s (remember “It’s a wonderful life”?) when bank runs couldn’t be covered since the money had been lent long term.

After that, the banks willingly ceded the bulk of the home lending business to Savings and Loans, who thrived until they, too, learned about the disadvantages of lending long and borrowing short. In 1980, they had many assumable loans still outstanding at 5-6% that were issued in the 1960s, but found themselves having to pay up to 15% to attract deposits, and they were quickly heading for bankruptcy. A few S&Ls manage to grow fast enough to survive, but most that tried rapid growth as a solution found it made things worse, not better, because in growing fast, they issued more bad loans.

For the next cycle, we tried the separating the originator from the lender, and packaging loans up for sale. That system crashed, too, in 2008, because the originators didn’t really care about the quality of the loans, only whether they could be sold, and buyers who were chasing yield foolishly bought poor quality loans, and even if they bought insurance against it, the insurer had no clue, and went broke, too, so the whole system imploded.

Is there a system that won’t inevitably crash? I doubt it. Maybe Austrians are right, and that the way to prevent the boom-bust cycle is to prevent credit expansion (i.e., prevent home lending).

And the raters were in on the scam, as long as they got paid.

“Is there a system that won’t inevitably crash?”

Yes, Carl, there is and its rather simple:

Step 1: Get the government COMPLETELY out of the housing market. That means no Fannie Mae, Freddie Mac, FHA, and every other direct/indirect method by which government interferes with the market. Veteran loans are acceptable for combat veterans – not guys/gals hanging out in a southern California base for ten years, counting inventory or sitting in a guard shack with an ocean view.

Step 2: Restrict lending to private lenders unconnected to a central bank which ultimately bails out its member banks when the ponzi starts to unravel. In other words, only people who stand to lose their own money can lend for a house (heck, let’s apply this to education and automobiles too!)

Common concerns:

“Well, no one would lend their own money, so no one will be able to afford a house!” – Not correct. If no one can afford a house, then house prices must fall until those lending their own money believe they will get their money back plus interest (i.e., payment for taking the risk). Those lending will ENSURE the house is affordable.

“No one will build houses if their prices are too low!” Seriously? There is nothing sophisticated about a house and mankind has been making them for each other without the help of an intrusive government for thousands of years. Prices of sophisticated electronics always fall and there is no reason for houses not to follow the same pattern.

That all sounds like a nice argument. The only problem is that housing crashed before the government got involved. It’s certainly true that government involvement hasn’t helped, so there is no reason not to discontinue it, other than the obvious one: When government involvement inevitably makes a market worse, the only solution that people can see is even more government involvement.

Prices going up and prices going down are part of the “price discovery” process of a marketplace and should be accepted as natural. Prices which trend upward only, such as seen in housing, healthcare, and higher education, are a telltale sign of industry/government collusion and intervention. The administrative state has grown and grown in practically every developed country and the citizens are ultimately, mostly to blame. Our crappy state sponsored high school educators have failed to explain how markets work (and also the nature of money, by the way) with the result being a population who clamors for more government intervention “to make it more affordable” or they just shrug their shoulders at the present intervention and say “no reason not to discontinue it”!

Most citizens just can’t see “The King, the King’s to blame!”

I would add Step 3: Make sure depositors are aware of the liabilities of the bank. Turn regulators into auditors. Codify GAAP rules into law and publish results. That way everyone can see exactly why that checking account is earning 5% interest when everyone else is only paying out 1%.

And why should a “system” not crash? Why is that some sort of problem?

To the contrary, when something has outlived it’s usefulness, the quicker and more thoroughly it crashes, the better. That way, it stops destroying capital and wasting resources. Making those resources available for better uses, including a replacement, if necessary, for the crashed system.

The only alternative, the one which have given rise to central banking, then complete uncoupling from gold, then bailouts, QE and ever more rapacious theft by debasement and regulation, is zombiefication. Keeping dead weights in permanent unearned splendor, just because well indoctrinated dupes are told “the system crashing” is some form of scary hobgoblin which must be avoided at all cost.

Instead, the only thing that is important, is to never, ever, under any circumstance, no matter what, allow those crashing from dragging any third party with them. No matter what. Then, systems can thrive and crash to their hearts content, with minimal consequence for anyone not voluntarily choosing to partake in them.

I wasn’t trying to make a qualitative statement as to whether a “crash” was good or bad. Kondratiev, for example, believed they were good, and caused the excesses to be purged out of the economy, setting the stage for a new wave of prosperity. Thus, he believed, capitalism was sustainable, and would not destroy itself.

The worst thing about the Fed/fiscal stimulus combo is that they have been largely successful in overcoming the natural cyclicality of the free market. In the pre-gold standard, pre-Fed years, depressions were much worse, and much more frequent. In the wake of a depression, speculation was driven from the market, and cash was king. Since we haven’t had a true depression since the 1930’s, the excesses have not been purged out, and the result is rampant speculation.

Am I saying that depressions are good? I am saying there is a tradeoff. While they bring tremendous suffering, they also rejuvinate the economy.

It’s more correct to say that “depressions” brought tremendous suffering. When people were barely able to scramble together food, water and shelter even in comparatively “good” times, it didn’t take much of a slowdown, for things to get rather grim.

Improving technology, and improving efficiencies, lift all boats. Such that today, even quite severe depressions from the mean, wouldn’t turn into starvation, or even souplines and tent living, for almost anybody. It’s just too easy to provide food and shelter for virtually anyone, at today’s level of technological development. So, a 30s style “depression,” against the backdrop of today’s technology and productive efficiencies, is more of a nuisance than a calamity.

It’s analogous to how “back then,” an infected wound was often a death sentence. While now, it’s merely some Neosporin, or perhaps a week of antibiotics, and you’re well. Again, perhaps a nuisance, but hardly a calamity.

So, you don’t think we can ever have another depression? Cyclical depressions have existed for as long as mankind has existed, and are even described in ancient historical documents. I disagree, but until such time as we have another, we’ll never know.

I think we came precariously close in 2008. I’m no fan of government bailouts, but as a small businessman, when it appeared that the banking system was at risk, I could see the handwriting on the wall. I had a debt to a bank at the time (I no longer do – it has been paid back, and I will never take another one). Had the banking system imploded, my loan would have been called. In other words, I would have been given 30 days to pay it back. There is no way I could have paid it back in 30 days, so I would have been forced into liquidation. The same thing would have happened to thousands of other businesses across the country, and thousands would have been put out of work, with the cascading effect of a precipitous decline in consumer spending that would have closed even more businesses.

Had that happened, there would have been chaos, and yes, we would have been in the middle of a depression. From that chaos, capitalism would have been renewed and reborn, and many would have learned important lessons. Even without a depression, some of us learned some important lessons. Was it a good thing to bail out banks, and prevent a depression? Different people have different answers to that question, I guess, but there is no doubt in my mind just how close we were to one that day.

Without knowing your immediate circumstances, I very much doubt the chances of you starving to death, or standing in a soupline hoping for 1000 calories a day, on account of your bank failing, is very realistic.

You may have lost a business. Which no doubt sucks for you.

But to whom? The people your business served, would still be there. Would someone else now serve them? Otherwise, the need you filled would still be there, assuming it wasn’t all along an opportunity only existing as a direct result of artificial bubble blowing. Are there anyone else more able to fill that need than you? If so, you going under, and they taking over, is hardly a net loss. Otherwise, if you can do it better than anyone, free competition would put you right back at it. Only this time, without the debt overhang.

Bankruptcies doesn’t suddenly make corn stop growing, oil stop flowing, buildings, roads and bridges fall down, knowledge about how to build stuff to disappear etc…. All it does, is rearrange who holds claims to all of the above, along with all the rest of value that the real economy produces. Aside from frictional losses, Bankruptcies are a true zero sum game. Can’t be any other way, since the underlying, real economy which produces stuff, is not affected by rearranging who nominally “owns” it. So, for everyone who loses a viable business, someone else gains it. For a net result of no change.

Of course, the frictional losses are non zero. But minimizing those need to be the focus. Not artificially preventing the rearranging in the first place, solely to help entrench the already wealthy and connected, at the expense of everyone else. Under pretext of something as benign as a bankruptcy, or a “crash,” is some sort of singularly scary hobgoblin “we” should all bow down to the money printers in exchange for supposed protection from.

And also, as per my prior post, how far removed from suffering people are at the onset of a depression, dramatically alters how much genuine suffering will result from it. The requirements for genuine, absolute, human suffering, are pretty fixed. Lack of water, calories, shelter and enough energy to avoid freezing and avoid your food rotting is about it. Today, we can have quite the “depression,” without many dying from outright lack of calories. In the 30s, people started out much closer to that boundary, even before the depression. Hence much of the suffering back then. Going from having 3000 to 1000 calories a day, induces a lot worse suffering than from 3000 to 1000 square feet of dwelling per person, despite both depressions being relatively the same. And going from 3 Billboard one hits in a year, to a mere 1, doesn’t really indicate Bruno Mars is truly suffering much at all…..

What you describe makes an excellent, though perhaps unintentional, point about the difference between a recession and a depression. In a normal downturn aggregate demand remains, and when a marginal business fails, its customers go to a competitor, who in turn grows stronger. The strong survive, and benefit, and the economy is better off as a result because the inefficient producers are eliminated.

By contrast, in a depression, aggregate demand IS destroyed. If every business loses 30% of it’s customers, a single business failing will not be enough. You need 1/3 of the businesses in that sector to fail. Now, aggregate demand doesn’t shrink equally. My father, who did live through the depression, always told me that the business remained steady at hair salons and bars, but that everyone else took a major hit. Non-essential purchases, like clothes, and capital equipment were hurt worse than most.

Worse, in a depression, it doesn’t all just go at once, it’s a downward spiral. Each year, a few more businesses fail, and their former employees spend less, causing other businesses to scale back, and then they lay off people, who in turn spend less, and so on.

The original theory of Keynes was that, in those rare times when aggregate demand is being destroyed, and the economy is spiraling downwards, government intervention can stabilize the economy, and set the stage for it to begin to grow again. Somehow we got from there to the idea that government intervention should be continuous, which I strongly disagree with.

My personal opinion, which many disagree with, is that 2008 had the potential to be the beginning of a depression. Had large banks been pushed into liquidation, they would have called all their loans. They lend to smaller banks, which would have pushed smaller banks to also call their own loans, and a substantial number of businesses would have been unable to meet the call, and been forced into liquidation as well. That would have led to a huge crushing in aggregate demand, and the businesses that did survive the initial hit would see a drop in sales, not a rise (except hair salons and bars, per my father). Thus, while in general I oppose all market interventions by government, in my mind 2008 was different, and probably was the one intervention in my lifetime that was justified. The economy did take a hit, but it grew back, albeit slowly. It did not continue to spiral downward.

“in my mind 2008 was different”

Thiiingzz are always diiiferent. But the solution is, conveniently enough, always the same: Government robbing the productive, to hand the loot to leeches…..

In reality, things may, just may, have been different pre Big Bang. Or Genesis. And even that is debatable. And highly unlikely as far as economics is concerned. Since that day, The Law has been “thou shalt not steal.” Not “thou shalt not steal unless you can make up some contrived excuse for why doing it is a-ok thiiiz tiime.”

“Aggregate demand” is nothing more than a simple sum of individual demands. There’s no dude named “Aggregate” roaming around creating any demand on his own. When demand from some individuals abate, things get cheaper for others. Effectively making said others richer. The “downward spirals” you talk about, is no more than an artifact of these price adjustments taking time.

And the prime contributors to them taking time, is exactly the possibility of a bailout or intervention, or an excessively slow moving and convoluted legal/BK process. As long as banksters, and other asset owners, can credibly hang on to hope that the government and Fed will bail them, and “asset prices” out, they won’t firesale every asset on their books for whatever they can get this moment. Hence productive assets get tied up in limbo, while yahoos squabble over who “owns” them. Instead of the assets being chewed up and spat back out almost instantaneously, to be picked up for a song by anyone who feel they can make productive use of them.

What needs to be the policy focus, is to speed up bankruptcy, and ensuring it is incontrovertibly final. Give everyone their day in court, but no more than a day. Maybe a week for the very largest multinationals. Then go with whatever resolution looks best at the end of the day. As in all else, there is no “right.” Certainly none that can be discovered by squabbling lawyers, governments flush with third parties’ money, and some officially sanctioned counterfeiting outfit running amuck.

Instead, the important part is getting the assets back out of limbo. Out of the courts, and into the hands of people who can make use of them. As quickly as possible. Exactly who ends up nominally owning them, and for what nominal price, is merely a triviality.

Do that, and the real impact of “financial crises” is minimized. Cannot be any other way, since real output is determined by real capital. Not financial claims to it.

Sounds idiotic to finance 30-year mortgages with short term borrowing. It’s a guaranteed way to bankruptcy. Even if there wasn’t government insurance, the short term profit motive prevails; by the time the mortgage blows up, the lending officers will have soundly retired.

I am surprised this can go on. /s

On target. Thanks Mish. Our financial markets are able to deliver money on demand. They need to be watched over to make sure they don’t tilt the playing field or extract rents, but apart from that, they can handle mortgages easily and effectively. The government should only be involved during a liquidity crisis to restart the engine (not cover stupid people’s losses), and that should happen very infrequently, and should be painful to all asset holders to avoid moral hazard.