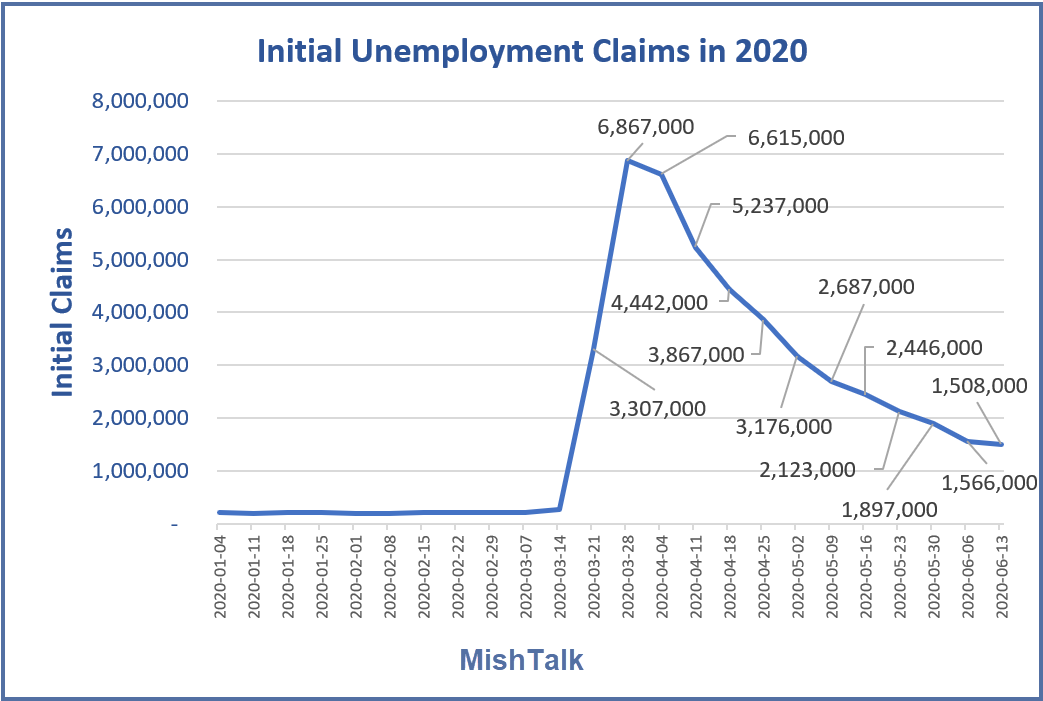

For the 13th consecutive week initial unemployment claims topped the 1.5 million mark.

Initial Claims 1980-Present

To put things into proper perspective, initial unemployment claims never topped the 1 million mark before Covid-19.

Now we have had 13 consecutive weeks in which claims topped 1.5 million.

Econoday Consensus

The econoday consensus estimate for claims was 1.22 million.

For many weeks the number of claims have topped the Econoday consensus.

Things are improving, but much slower than expected.

Mish

I can only speak to the shifts I’m seeing in the demands for our masonry service. While unemployment is high, we’re seeing an increased demand for home improvement projects. Many homeowners are foregoing costly vacations and it seems they’re putting their money into improving their home living experience. The demand has actually spiked quite a bit moving into summer and our bottleneck has been finding quality (and skilled) employees. With the big shifts we’re witnessing in the economy and the way business is done, it could make sense for people who’ve lost their jobs to look into getting trained to work in the home service industry – where the demand is still high and should hopefully remain high. https://www.toledomasonry.com/

Well to me Mish it looks like the big layoffs early on were Covid closure for non economic reasons, they were for health reasons. Then as those that were directly impacted in businesses like restaurants and airlines and bars and theaters were laid off immediately as what you may call the low hanging fruit of vulnerable jobs, as they were quickly unemployed and the Cares act kicked in and they were staying at home but not fired or laid off the number of new claims went down sharply to under 2 million per week.

I think the reason it is stubbornly high at more than a million and a half per week is that some businesses took the loan/grant money and paid their employees to stay home till the money ran out. Now they are being forced to let them go so that the employees can collect all that juicy Cadillac unemployment which in most cases is more than they could make on the job anyway. In fact I bet that is why there is $100 billion in unclaimed funds left in that loan/grant program, employees were probably begging their bosses to let them go so that they could claim UI for a lot more money per week, I know I would have.

ANd as this grinds on we have arrived at a point where the layoffs are not due directly to Covid/health reasons but these new economic realities. The big Covid firings were February and March, then started the ECONOMIC terminations. As many as a third of all small businesses are gone and not ever coming back. They employed a lot of people. And even among medium to large businesses economic conditions, loss of revenue, operating at a loss, there is a lot of cutting back, and much of that is going to end up being permanent. They are going back to core business basics, and trimming what they can even from that.

I think we will see the rate remain well over a million per week for a while, and as the second wave crests go higher. I honestly believe that people were shut in for about 90 days starting in February and that is about the length that is tolerable for lock down. Then they got squirrelly and free floating anxiety hit them, restlessness. The Floyd George thing exploded on the scene and they just rationalized that it would be better to get Covid than stand by and allow the cops to get away with murder. I think all those weeks of going out and protesting with no rules has lead to a very rapid spread of virus. Especially among those who were tear gassed and pepper sprayed. That crap leave lung tissue raw and easy for pathogens to get hold.

I think we are exiting the Covid firings and entering the real economic downturn, and that a second wave is just going to aggrevate that trend.

By election day which is now just 19 weeks away, I think we will be in a recognized depression. By some metrics we already are in a DEPRESSION though people will not yet admit it because they say those metrics are all temporary and unavoidable, but to me I see the temporary things as slowly becoming permanent, things like 31% of all mortgages are in arrears and forbearance. Ditto auto loans and credit card payments, with well over a third of the latter going unpaid. Duke Energy here has suspended power disconnects for non payment, but that is not going to last much longer. I cannot find data on the rate at which people stopped paying but it makes sense that people would stop paying power bills if they know they are not going to be disconnected for it, at least before they stop paying on the car or house payments.

I have noticed in the GFC and other recessions that people prioritize car payments I believe because they have to have a car to get to work and in a prolonged emergency will let the house go and live in their car, because without that car they can never get back to work when times get better.

This is the way I see it from the ground rather than as an analyst in some great gray tower in New York or LA, they seem to think that Covid was al there is to this and that it will just have an end date at some point at which time we will do that “V” shaped recovery right back to business as usual. That just could not be more wrong. Permanent damage is being done to the economy, and it will have knock on effects that make 1932 look like a fine little holiday. All I can really swear to at this point is no matter what they come up with for a solution I will be cut out of it as will nearly everyone else who is still paying their bills.

Golf courses where I live are almost as busy Monday thru Friday as they are on a weekend. As a retiree I have found it has suddenly become more challenging to book a mid week tee time since the onset of COVID. I guess the increased unemployment benefits are being well spent.

Maybe they can lobotomize all those errant college loan recipients. You know, just repo that education?

But lobotomizing college grads risks improving their cognitive skills that have been damaged by higher education!

Those that took on vast college debt and who were in an economics/finance/accounting discipline are doubly screwed. Being in that much debt reflects on credit scores and those are looked at closely in these fields. After a fatal house fire in 2001 in which I lost everything and had no choice but to file BK chapter 7 I found out the hard way that a finance degree means you can never file for bankruptcy if you ever expect to work in the field again. I mean who out there is going to hire someone that “can’t handle their own finances” when there are so many qualified candidates that have no BK? Circumstances of the event mean nothing, they just sound like clicks and whistles to the personnel departments, making excuses for bad management. In fact in 98% of cases you will never have the chance to explain why you had to file, you will be checked for bad credit and winnowed out without ever being asked to explain.

Welcome to capitalism. The economic system that is as threadbare and destructive to individuals as socialism/communism.

Actually, I’m surprised recent economic numbers higher … considering … payback in H2 … hope everyone enjoyed the rebound.

…

“Americans have skipped payments on more than 100 million student loans, auto loans and other forms of debt since the coronavirus hit the U.S., the latest sign of the toll the pandemic is taking on people’s finances.

The number of accounts that enrolled in deferment, forbearance or some other type of relief since March 1 and remain in such a state rose to 106 million at the end of May, triple the number at the end of April, according to credit-reporting firm TransUnion. TRU -0.10%

…

But lenders will shoulder the unpaid loans for only so long, and many are expecting delinquencies to soar later this year as the recession drags on.

The deferments are also making it difficult for lenders to decide which applicants can get new loans. There isn’t one uniform way of reporting people seeking help with their debts to the credit-reporting firms, and some lenders say they are having a difficult time determining if applicants’ credit scores and credit reports reflect their true levels of risk. Credit scores factor in missed payments such as delinquencies but aren’t supposed to reflect deferments tied to the pandemic.”

“Credit scores factor in missed payments such as delinquencies but aren’t supposed to reflect deferments tied to the pandemic.”

I actually was just reading about those Tony, about 70% of all mortgages are federally insured in one way or another, mine is a VA loan so it is federally backed. I bought the house in April and now find there is going to be a major expense for a structural issue that I can’t avoid. I am trying to decide if I want to go into forbearance or deferment and there is a major difference between the two though people use them interchangably as you have in your post. I am not wanting to do either really, but can see no way around it as my VA home loan is a zero down 100% mortgage. The only way I can borrow against equity for the repair is if I have equity which means the house would have to appraise for at least 20% more than I paid for it, and right now appraisals are touchy, not to mention the waiting list for appraisal is in places months out as many appraisers are taking a few months of paid vacay thanks to generous UI they qualify for under the Cares Act, most are independent self employed and qualify one time only for UI which normally they would not.

The sales data is thin, there is a lot of refi activity as people try to extract equity to get through tough times, but sales have taken a dive. Prices remain about where they were only because supply has evaporated faster than demand. There is about 4 months supply on the market which is little changed and considered tight. We actually hit a 3 month supply December 2019, which is really very tight. We are bounced back to 4 months as of this chart from the St. Louis Fed out Wednesday: https://fred.stlouisfed.org/series/HSFSUPUSM673N That page also shows a graph where Covid triggered an immediate drop in prices of existing homes, but which have already come back as government programs stalled the drop.

Forbearance is automatic for six months if your mortgage is federally backed via FHA, VA, or one of the GSE’s or credit unions, but the payback begins at the end of the forbearance period. And while lenders can’t begin foreclosure against you in that forbearance period they can and some do report you as being in default of your obligation to reporting agencies. Some will not, and some will even extend the forbearance by another six months.

Deferment is different, the CARES Act only requires automatic forbearance for six months basically no questions asked. Deferment is up to the lender. In effect what it does is take several payments and remove them from the present and tack them onto the end of the contract, in effect simply changing your payoff date. Lenders do not have to go this route and if yours does it is only because they know your alternative is automatic forbearance, or even just defaulting on the loan. But a lot of people are at 4% plus on their mortgages and with rates this low banks want to keep you at that higher rate. Not giving a deferment will in a lot of cases push people to refi at record low rates.

Also, damaging your credit may be pure fun for banksters, but it also leaves your repayment potential crippled. Many people will simply stop paying if their credit scores tank as happened in the GFC.

“Forbearance refers to an agreement made between you (the homeowner) and your lender in the event that you’re unable to pay your monthly mortgage amount for any reason. The lender freezes your payment requirements for a set amount of time. After this date, you would be required to continue your normal monthly mortgage payments, and pay back the balance owed, plus any interest or fees that accumulated during your grace period.”

Deferment: “Deferment is basically coming to an agreement with your creditor to freeze payments for a period of time. The money you don’t fork out during the payment holiday is then added to the end of your loan.

So let’s say you do a 90-day deferment on your mortgage, which is an option many lenders are offering right now. That means you won’t have to pay anything toward your mortgage for the next three months. But the life of your loan will extend by three months on the back end.

The favorable thing about deferment is that additional interest and fees don’t accrue during the payment holiday.”

So deferment is by far the best avenue if your bank will do it. If you are deep enough into your mortgage that you have equity to borrow against that can save your life and keep you from having to resort to either option. So really the people taking advantage of this are those that are early in their loans and do not have enough equity they can tap it. I think a lot of people jumped on forbearance when the Cares Act was passed without understanding that it will require them to make up all the payments, penalties, fees, and interest in the near future. The smart ones who could went with a cash out refi as interest rates are at a record low so they could kill two birds with one stone, get enough cash to get through Covid, and a lower interest rate to boot, along with about a 60 day period with no payments.

That is what accounts for the extreme rise in refi’s I believe.

let’s see what happens when the PPP covered period ends… that’s a few million loans intended for 8 weeks of employment for 10s of millions of people.

same for the other CARES Act sections that prohibited laying off employees, for a little while, in exchange for feeding from the trough.

The 8 weeks ended in mid-June. Congress extended that to 24 weeks, so companies that didn’t spend it in 8 weeks wouldn’t have to pay back the loan, but many companies have already used the PPP dollars. I know mine used it up by June 15th.

“Initial unemployment claims dipped slightly to 1,508,000.”

…

This report is for the week BLS conducts its survey for monthly jobs report.

Will June be as eye opening as May’s??

Given the environment is so outside of what the BLS models are built for I would just ignore it as garbage in/garbage out.

Continuing claims leveling off

Last week dropped 339K

This week only 62K

Sitting at 20,544,000

And that is with PPP still in force … as that fades??

PPP is at least partly out of force. The original rules said to use all the money in 8 weeks, which ran out a few weeks ago. Some companies didn’t, and faced the possibility of having to repay the “loan”, so Congress gave them a get out of jail free card, and gave them 24 weeks. Those companies are still using PPP, and will be for awhile. What percentage complied with the original rules? It’s hard to know, but some are done with PPP, some aren’t. The high new claims right now are no doubt coming from companies that have used up the PPP money.

Improving? The decelaration is slowing. 46 million initial claims. I have yet to read about improvements that aren’t largely statistical artefacts.