Velocity of money is defined as (prices * transactions) / (money supply). Economists substitute GDP for (prices * transactions).

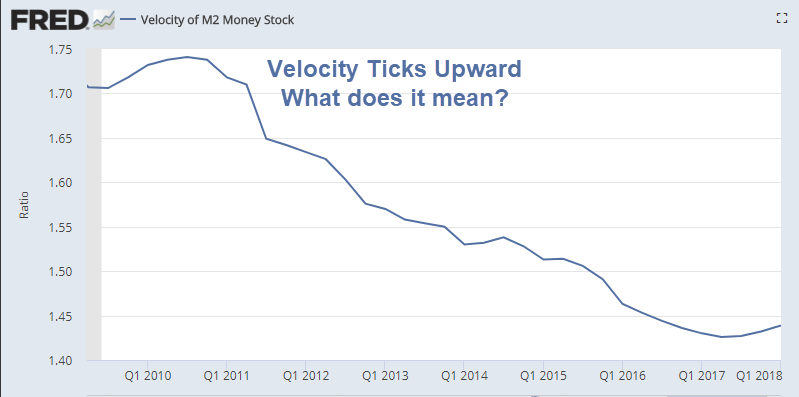

This tweet caught my eye today.

I suspect that opinion represents the majority view, but does it make any sense?

Let’s investigate with a series of charts.

Velocity of Money vs. CPI

Velocity of Money vs. CPI (Percent Change From Year Ago)

The above chart is particularly amusing. There are periods of correlation, inverse correlation, and periods of major random meanderings of velocity while the CPI does nothing at all.

Velocity vs GDP

Since 1998, the year-over-year trend in velocity has strongly correlated with the year-over-year trend in GDP. In the stagflationary 1970s Velocity and GDP were often inversely correlated.

Velocity “Magic”, Tax Receipts, and GDP

I have written about velocity several times previously. Please consider some snips from Velocity “Magic”, Tax Receipts, and GDP.

Velocity Magic

Austrian economist, Frank Shostak, took apart conventional wisdom years ago with his column Is Velocity Like Magic?

“The Mainstream View of Velocity

According to popular thinking, the idea of velocity is straightforward. It is held that over any interval of time, such as a year, a given amount of money can be used again and again to finance people’s purchases of goods and services. The money one person spends for goods and services at any given moment can be used later by the recipient of that money to purchase yet other goods and services.

For example, during a year, a particular $10 bill might have been used as following: a baker, John, pays the $10 to a tomato farmer, George. The tomato farmer uses the $10 bill to buy potatoes from Bob, who uses the $10 bill to buy sugar from Tom. The $10 here served in three transactions. This means that the $10 bill was used three times during the year; its velocity is therefore 3.

From this it is established that: Velocity = Value of transactions/supply of money. This expression can be summarized as: V = P(T/M) , where V stands for velocity, P stands for average prices, T stands for volume of transactions, and M stands for the supply of money.

This expression can be further rearranged by multiplying both sides of the equation by M. This in turn will give the famous equation of exchange: M(V) = P(T).

Many economists employ GDP instead of P(T), thereby concluding that: M(V) = GDP = P x (real GDP).

Most economists take the equation of exchange very seriously.

Velocity Does Not Have an Independent Existence

Contrary to mainstream economics, velocity does not have a “life of its own.” It is not an independent entity–it is always value of transactions P(T) divided into money M, i.e., P(T/M). On this Rothbard wrote: “But it is absurd to dignify any quantity with a place in an equation unless it can be defined independently of the other terms in the equation.” (Man, Economy, and State, p. 735)

Since V is P(T/M), it follows that the equation of exchange is reduced to M(PxT)/M = P(T), which is reduced to P(T) = P(T), and this is not a very interesting truism. It is like stating that $10=$10, and this tautology conveys no new knowledge of economic facts.

Boom and Bust

Shostak wrote that in 2002. A housing boom and a housing bust followed.

Also consider Shostak’s article “Money Velocity Myth”

We are now in an everything bubble. Another bust is guaranteed.

Velocity will not cause the next bust no matter what it does (although I do expect velocity will decline for the simple reason I expect massive amounts of further monetary stimulus).

The cause of the next major decline will be the same as the cause of the last major decline: excess monetary and fiscal stimulus by the Fed, ECB, other central banks, and various government bodies.

Circulating Money

One irony in the velocity debate is that money does not even “circulate” as widely believed.

“Money can be in the process of transportation, it can travel in trains, ships, or planes from one place to another. But it is in this case, too, always subject to somebody’s control, is somebody’s property. “(Human Action, Mises p. 403)

Garbage In = Garbage Out

Starting with flawed measures of money and flawed measures of GDP, a good summation of velocity is “garbage in = garbage out”.

Velocity itself does not predict anything, nor cause anything! It’s not an independent variable.

What’s Coming?

Is Inflation Coming? Stagflation? Anything?

I assure you “something” is coming. I also assure you the current measure of velocity offers zero insights.

Fundamentally, when asset bubbles bust, periods of strong disinflation or deflation begin. Until then, there there may be another inflation scare just as we saw in 2000 and 2007.

Inflation Scare Now, Deflation Coming

It’s pretty clear we are in the midst of an inflation scare right now.

Given the amount of global financial leverage, I strongly suggest a deflationary bust is the most likely outcome looking ahead.

Deflation? Really?

Yes, really.

This topic is always a hair-raising event for inflationistas who really do not know how inflation works in the real world.

Definitions

- “Inflation is an increase in money supply and credit, with credit marked to market“.

- “Deflation is an decrease in money supply and credit, with credit marked to market“.

That is how the real world works in a fiat credit-based system.

In 2008, those with myopic views thought oil was going to $200, then $300. Instead, the price collapsed with the housing bust.

Austrian economists with a focus on money supply alone also missed the boat.

Those who understood the importance of bank credit that could not be paid back were the ones who got the picture correct.

For further discussion, please see Inflation Coming? How About Deflation?

Mike “Mish” Shedlock

first off this is M2 which is money market accounts not M1 which is real money which the Fed doesn’t recognize. second you look at a giant waterfall and notice some water splashing up at the bottom and you think the river has changed course? join the chorus of bond market pundits who are sure the bull market is over. not yet children.

I believe we already have modest stagflation, at least based on the Seattle area. Wages are stagnant and prices of most assets and goods have increased dramatically (especially housing).

Mish said “Until then, there there may be another inflation scare just as we saw in 2000 and 2007.” That has been my sentiment as well. These scares seem to come just before deflation ramps up. With debt levels so high, I do not see how most people can service their debt, let alone take on new debt. I do not see any driver for higher wages anytime soon.

Actually the velocity numbers for 2017 are completely wrong, because (unbeknownst to anyone) I had 100 trillion dollars buried in my garden. I didn’t do anything with it… So I guess the 2017 velocity is much lower suddenly. Oh and by the way that 100 trillion changed hands every day with my wife (unbeknownst to anyone) in 2016, so please correct the velocity of that year too, it was much higher!

@IICS There’s something intrinsically alarming about seeing monetary inflation slow down whilst spending speeds up. That’s a running-off-the-cliff situation.

Funny thing about inflation is, if most businesses expect it, they’ll schedule price hikes accordingly and it becomes a self fulfilling prophecy.

Then they find demand suddenly drops off. Then they panic.

How about train and not truck?

God, how many years have We been hearing that BS….one day they’ll be right. Just seems it never comes.

Look at the declining growth in M2. Velocity is rising because M2 is falling. If you pull back and look at the ratio against M2, it doesn’t look good for the inflation argument.

link to fred.stlouisfed.org

Miners barely moving

Btw, gold is tanking today.

i tend to agree with you that the velocity number is meaningless. It used to have minimal value, but now it has none. The reason is QEx. You can lead a horse to water, but you can’t make it drink. You can put money into the economy, but you can’t make it circulate. Massive amounts of money were pushed into the economy, but much of it isn’t circulating, and thus, the velocity has fallen, because when you average a growing pot of money that doesn’t circulate with the rest of the money, you get an ever lower velocity.

Note that this also explains the connection between velocity and economic growth. When the economy is growing, QE can be stopped, or even reversed, withdrawing money from the economy, and causing the computed velocity to rise (because there is less non-circulating money to average in).