Let’s start with a discussion of how the short-end of the yield curve will act.

The following chart shows that when the yield on 3-month treasuries jumps above the Fed Funds rate, a rate hike is imminent.

CME futures suggest a 92% chance in December and just over 50% in March.

If the Fed does get in two rate hikes, what would the yield curve look like?

I suggest something like the following.

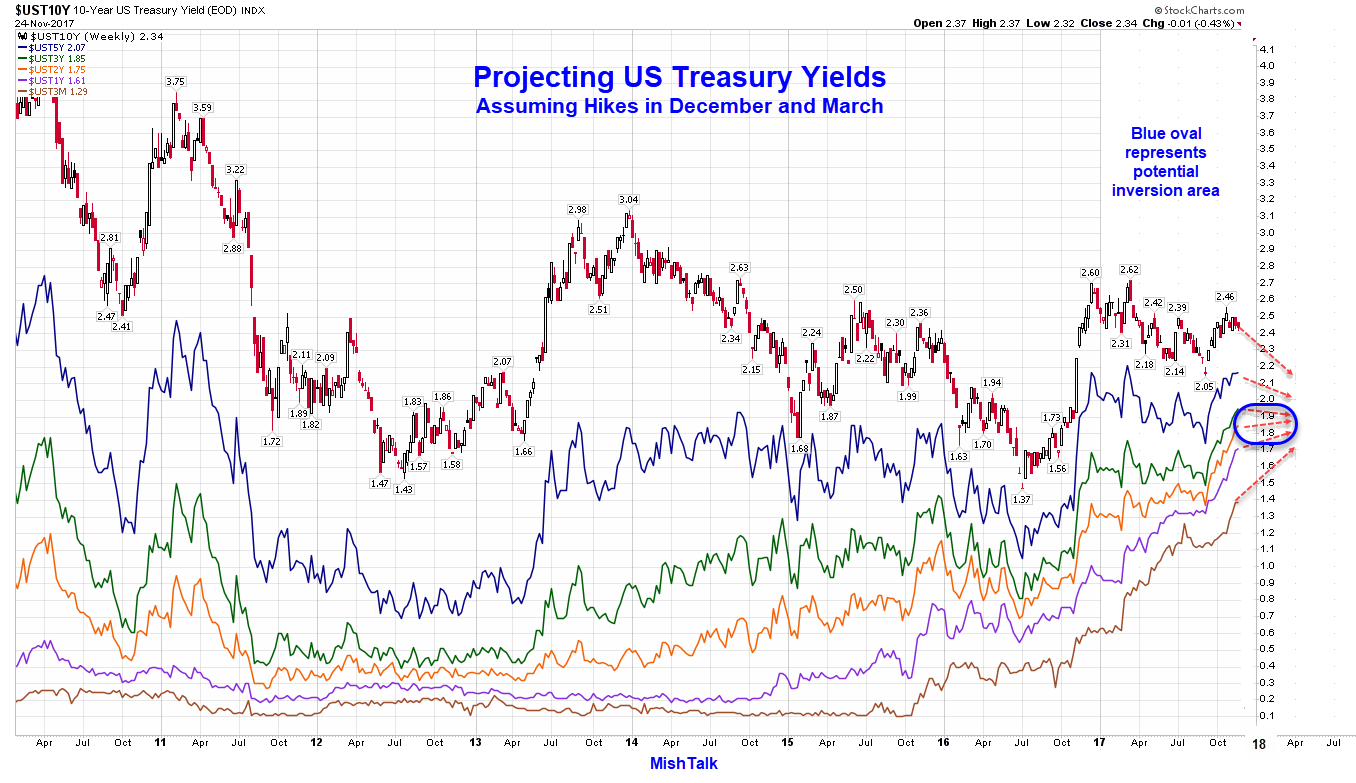

3-Month to 10-Year US Treasury Yield Projection

My base assumption is consumer price inflation is not about to jump significantly higher, and if not, there will be downward pressure on long-term yields.

The short-end of the curve is easier to predict. Add 50 basis points of hikes, then subtract about 5-10 basis points corresponding to the patterns in the first chart.

Inversion Chances

The blue oval represents an area in which we may see a yield curve inversion (longer-dated treasuries yield less than shorter-dated treasuries).

Should that occur, it will be a strong recession warning.

An inverted curve does not guarantee a recession, however, nor does lack of inversion mean a recession will not happen.

Regardless, we are very close to the end of this rate hike cycle.

Mike “Mish” Shedlock

The 2 yr and 10 yr treasury spread watch is definitely on. Will be definitely interesting watching the spread over the next few weeks as the quarter point raise in two weeks looks to be a go. Do inverted yield curves provide a good correlation of impending recessions? https://www.cnbc.com/2017/11/28/this-potential-signal-should-cause-investors-to-head-for-the-exits.html

I’ve been expecting them for darn near 3 years and it ain’t come yet.

2. sustained stock market decline

1. recession

Mish: I believe you’re misreading the chart. The Fed Funds implied probability of a December hike is 100%, broken down to about 92% chance of 25 bps, and 8% chance of 50 bps.

I think the FED is raising rates because they need room to lower them if things get bad.

Inverted yield curves are no longer a signal for impending recession. Historically, during uncertain times, the yield inverted because of increased demand for longer dated maturities. The rates for longer dated maturities went down. In this case, it will invert because the yield for shorter dated maturities will be forced up. The FED is forcing an invert, not the market.

Why would they stop hiking?

Easy:

1: recession

2: sustained stock market decline

I expect both

That means any meaningful decline in the 1st half of the next year and definitely in 2nd half. My reason for Bitcoin is black money, especially in politically unstable countries. Oh economically unstable countries.

Where is the demand for long-term treasuries going to come from when risk rises for govt defaults, trust is destroyed when the pedophilia bubble pops, and when gentlemen stop preferring bonds and opts for Bitcoin?

You continue to ignore the real reasons the Fed is hiking, which has nothing to do with the economy and everything to do with their reputation as a serial bubble blower and the pending pension crisis. Since the flows into stocks from the periphery will only be increasing and the govt pension problem only getting worse, why would they stop hiking?

So far the rate hikes have been done using RRPO, finanical repression. RRPO affects the broader market, not just a few charter banks. The first hike had 105B of RRPO, and now the terms are simply buried in the boilerplate at some astronomical figure per day, and potentially more than QE, which was 85B a month. The discount window is an old Fed tool, with RRPO the banker grabs you by the collar and says borrow. Without funding these rate hikes, interest rates would be much lower, which is another term for inverted yield curve. If the Fed lets off the gas, the vortex of falling rates (as you note the market has already priced in a rise) could suck us into a deflationary spiral. Of course if the banks simply stop borrowing there is no need to open the RRPO line. and basically everyone is happy.