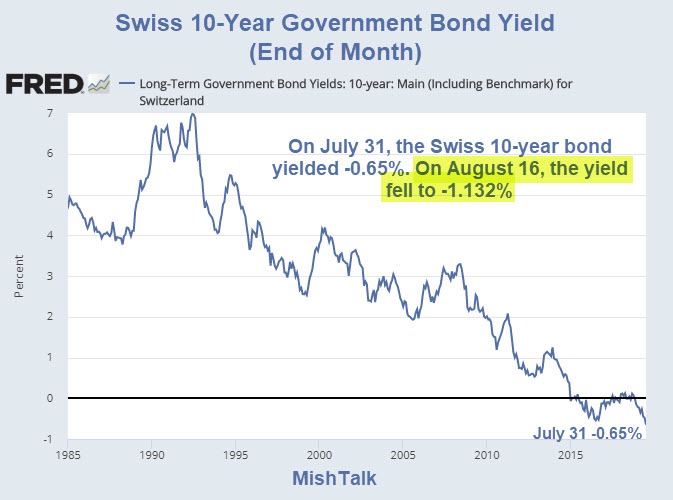

Swiss Bond Yield Calculation

Calculation from numbers I plugged into MoneyChimp.

Someone “investing” in Swiss government bonds rates will get back about 89 cents, ten years from now, for every dollar invested today.

Logically Impossible

This is logically impossible, yet, it’s happening.

There’s far worse.

Price of Austria 100-Year Government Bond

The 100-year bond trades at 200% of par. You get half your money back if you live long enough.

Madness? You bet.

17 Trillion in Negative Yield Bonds

Bloomberg discusses Ways to Profit From $17 Trillion of Negative-Yielding Debt

The article mentions three ways to play.

- Carry and Roll

- Currency Hedging

- Playing the slope of the curve in one currency vs another

My suggestion: Don’t.

The article did not mention risk. This is not “free money” as the article makes it appear.

The chart below shows one of the ways such schemes to pick up a few basis points can go hugely wrong in a hurry.

How Losses Can Build Quick

https://twitter.com/geoffreysbatt/status/1162328285734477824

As a technical point, the loss would be +37.8% not -37.8%. The return would be -37.8%.

In addition to yields blowing up, currency moves can also get out of hand and hedges aren’t perfect.

Some hedge funds are going to get burnt badly doing what the Bloomberg article suggests.

Currency Wars and Monetary Madness

17 trillion in negative-yield debt is proof of currency wars and monetary madness.

Globally, central banks want to cram more debt into a monetary system that is choking on debt.

Meaning of Zero

“Zero Has No Meaning” Says Greenspan: I Disagree, So Does Gold

Alan Greenspan is wrong. Zero is very meaningful with negative being even more meaningful.

Brick Wall

Negative yields mean central banks have hit a brick wall.

They cannot cram any more debt into the system. There is no tolerance for paying interest.

The evidence is overwhelming.

- More Currency Wars: Swiss Central Bank Poised to Cut Interest Rate to -1.0%

- Inverted Negative Yields in Germany and Negative Rate Mortgages.

- Fed Trapped in a Rate-Cutting Box: It’s the Debt Stupid

Mike “Mish” Shedlock

Picking up pennies in front of a steamroller.

Sorry – slightly off topic, but of interest. People who are into cryogenics are trying to determine how to invest their money for maybe centuries when they can be brought back to life. Current dollar bills may very well be invalid – so they are looking at other ways to invest.

There was an interesting podcast on this:

BTW, the Oddlots podcast is worth a listen beyond this episode.

The push for cashlessness makes sense now – every time you receive your salary, you will immediately start to lose it. Unless you spend it on stuff or go deeper in debt. Saving will be impossible.

A real possibility. Will guns and/or ammunition become a black market currency?

Btw, Bernanke was writing about this kind of stuff before he became the head of Fed Reserve.

This is a great idea. Combine positive inflation with negative interest, to achieve stunningly negative real returns. Talk about a booming stock market, though: Since the appropriate PE is 1/(interest rate), the PE can go to infinity. Any positive return on stocks is better than a negative return holding cash, after all. Real estate prices can similarly go to infinity, for the same reason.

All this brings to mind the famous quote attributed to Jefferson, (but which he never said): “If the American people ever allow private banks to control the issue of their money, first by inflation and then by deflation, the banks and corporations that will grow up around them, will deprive the people of their property until their children will wake up homeless on the continent their fathers conquered.”

While that quote is dead on, what with the massive inflation of the 70s and 80s, and now deflation, it is important to remember that “Famous dead people make excellent commentators on current events.” Ralph Keynes, 1992.

“The problem with quotes on the Internet is that it is hard to verify their authenticity.”

~ Abraham Lincoln

“Currency Wars and Monetary Madness”

Default by another name. None dare call it default.

“The 100-year bond trades at 200% of par. You get half your money back if you live long enough.”

Last time around, Roosevelt confiscated gold, then devalued the dollar.

With the buying power of inflation, assume 2%, that’s 20 cents

I like gold but is it really the safe asset we like to think it is? What are you going to do with your gold if the government makes its possession a capital offence? IRS managed to sent letters to cryptocurrency traders, imagine how easy it is for them to get a list of buyers from a bullion dealer. Then they buy it back from you at a price of their choosing or confiscate it if they want to. What are you going to do about it?

There is no investment that is government proof out there, absolutely nothing. Maybe the best investment is to work towards having good and responsible government.

Isn’t this just part of the “everything bubble” that the FED started? Listened to a podcast yesterday where David Stockman basically said this is all due to speculation and flippers, and that seems to be a valid explanation. If you have no intention of holding the bond to maturity you really don’t care about the yield, just that the greater sucker is looking to buy.

We all know central banks are the only buyers directly or indirectly of neg bonds…..they’re the biggest buyers of stocks,bonds,gold,silver,oil to prop it up.They have acre after acre of money trees (printing presses)and they’re planting cultivating new trees every day!

Soon they will have MMT: Magic Money Trees.

The logic of time preference applies to whether you would rather forego present consumption for future gains. This makes sense to ordinary people who work for a living and have unmet needs which they might postpone.

But most of the big money is handled by people for whom this calculus doesn’t apply. They either cannot consume the money (managers) or their consumption is only a marginal proportion of their income (“falling marginal propensity to consume”). Their only problem is how to turn their money into more money.

Since there seems to be only so much income to garner, the money can increase only by progressively stacking it up on top of a fixed “yield”, which is the same as saying the interest is falling. For every halving of the interest, you can double the debt supported by said yield, asymptotically (in the theoretical sense) approaching infinity as interest approaches zero; the income supporting this debt pyramid illusion can be leveraged even more by extending maturities out further and further (heh, do we have a millenial bond yet?).

A shock to the amount of income supporting this pyramid could mean all assets emerge beyond the event horizon unencumbered.

Mish, I’m curious as to your take on how negative yielding bonds will affect government revenue in the future, especially Europe.

All those investors buying that stuff won’t be paying on any gains, since there won’t be any….for a long time. Unless they sell today.

Banks are getting crucified

ECB policy accelerated problems with Deutsche bank and Italian banks

Hardly worth turning the crank on the money printing machine anymore, is it?

“As a technical point, the loss would be +37.8% not -37.8%. The return would be -37.8%.” I’m not sure what you are trying to say, but Geofrey Blatt is likely correct. If the interest rate went back to where it was 30 days ago, the value of your bond would drop from 200 to 125, a 37.8% loss.

He’s saying that losing a negative is a positive.

“The 100-year bond trades at 200% of par. You get half your money back if you live long enough.” That’s not at all what that means. The original bond had a rate of 2.1%, meaning in 100 years you would have about $8 for every original $1 invested. Now you need to pay $2 to get that $8 in the end. The bond would have to soar to 800 before the yield was negative.

Doesn’t this have a coupon, or am I mistaken?

You’re not very bright. Please comment on things you have a clue about.

Yes, my calculation came to $2.10 of interest for every dollar loaned by a person in 2018.

1.021^100 = 7.99. The math works out. Or pretty close. If the bond were 2 YO when purchased, you would only get 98 years of interest.

This assumes compounding of the interest, but if rates are negative throughout, this doesn’t work.

Or.. would you rather have gold?

Why gold? Wouldn’t you rather own a worthless piece of paper that, to rub salt into the wound, is taxed at 1% per year? C’mon where’s your patriotism?

Ask Ruth Baider Ginsburg.

As Keynes observed, in the long run…

When governent bonds go pets.com…

well, what will 89 cents buy in 10 years?

deflation has an upside.

and that current dollar? after taxes, it was worth 55 cents.

of course, in 10 years taxes might take most of that 89 cents.

Why would you ever be taxed on an 11c loss?

To encourage roll-over instead of redemption?

A question. I have no idea.

I’d rather bury a dollar in a jar in my back yard than buy a bond to give me 89 cents an entire decade from now.

Deflation is a fantasy — unless it’s your stock or property portfolio you’re talking about, in which case, yes. In addition, what the CHF is worth relative to the USD in 10yrs time is irrelevant. It’s what it’s worth relative to gold that matters.

Frankly, neither the CHF nor the USD will exist in 10yrs time